- UK retail sales surged in June, largely reversing coronavirus collapse.

- But they may overstate economic recovery, Capital Economics says.

- PMI surveys surge ahead of Eurozone rivals including German PMIs.

Image © Adobe Images

Achieve up to 3-5% more currency for your money transfers. Beat your bank's rate by using a specialist FX provider: find out how.

UK retail sales surged in June while IHS Markit PMI surveys suggested that manufacturing and services companies operating in the troubled UK economy pulled ahead of the Eurozone rivals in July, although economists have cautioned that the retail data likely overstates the broader economic recovery.

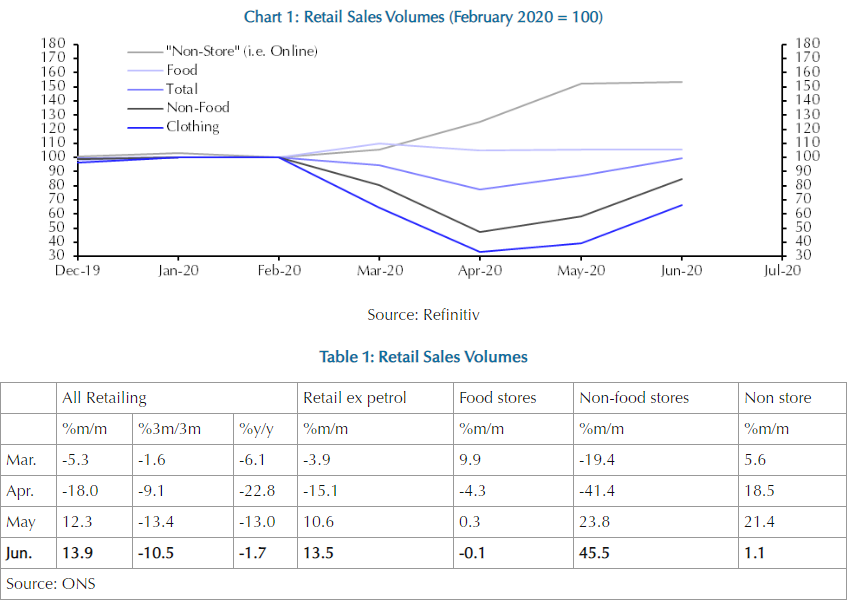

Retail sales rose 13.9% last month, building on a 12.3% gain from May and backfilling much of the -23.1% fall seen in March and April. Gains were led by food stores and non-store retailers like those who do business online, although non-food and fuel sales also saw strong increases.

Non-food sales rose by 45.5% from May levels last month, although sales in non-food stores were still -15% lower than in February, indicating that much discretionary expenditure has been online. Food sales have risen 54% since their trough and were 5.3% higher in June than they were in February.

This left June retail sales down by only -3.2% relative to same period one year ago and by -2.7% when compared with the level of sales volumes seen in February 2020, although economists have warned that this rebound likely overstates the recovery of the broader economy.

Above: UK retail sales statistics in chart and table form. Source: Capital Economics. Click for larger image.

"This is impressive given that in the UK non-essential retail stores had only been open for two of the four weeks of the survey in June," says Ruth Gregory at Capital Economics. "But the retail figures overplay the speed of recovery as they capture a substitution away from non-retail spending (i.e. restaurants to supermarkets, bricks & mortar to online). And the recovery in non-retail spending has been much more muted."

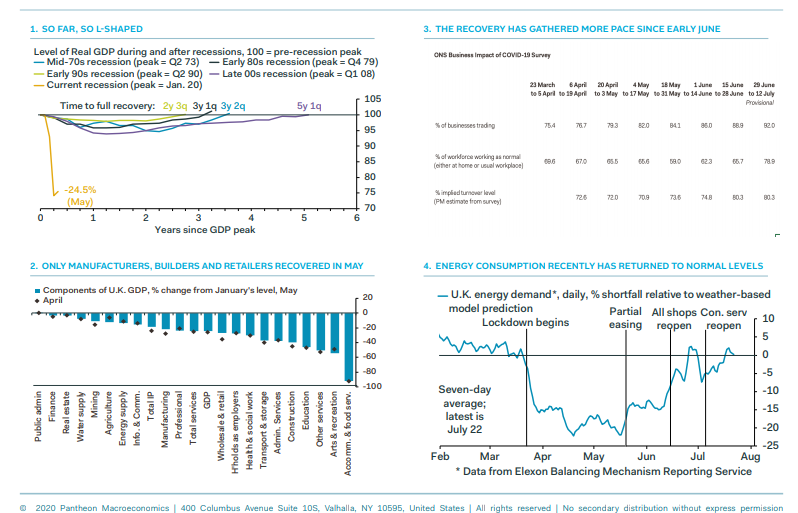

The economy contracted by -5.8% in March and by a further -20.3% in April as the nation entered 'lockdown,' while the May month brought only a meagre 1.8% rebound in GDP, leaving the broader economy deep under water for the year.

Retail sales are a meaningful part of the household spending that accounts for a majority share of the economic output so June's rebound could bode well for that month's GDP data, although the recovery has been slower in other parts of the economy and economists are worried that it could be tailing off.

"Households likely will continue to devote a larger fraction of their overall spending to purchasing goods in the second half of this year, due to the greater risk of catching Covid-19 when consuming most services. Nonetheless, households’ incomes will not recover to pre-virus levels, given that surveys suggest cumulative job losses will be greater than those during 2008-to-09," says Samuel Tombs, chief UK economist at Pantheon Macroeconomics.

Above: UK economic collapse and recovery thus far, in charts. Source: Pantheon Macroeconomics. Click for larger image.

The UK suffered the worst coronavirus outbreak in Europe with larger numbers of infections and deaths than all other continental countries while its services heavy economy has been expected to suffer a deeper and more protracted downturn than many counterparts.

Damage has been historic and recovery prospects remain uncertain but while June's retail sales data offer a glimmer of hope to economy-watchers, Friday's PMI surveys have openly contradicted the notion that the UK is lagging behind its European peers in the race out of the coronavirus trough.

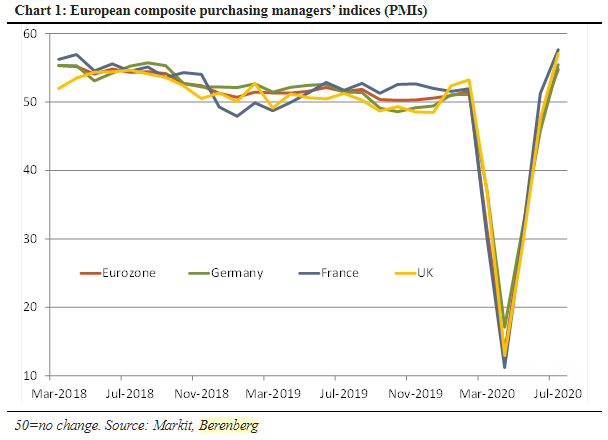

IHS Markit surveys suggested Friday that the services industry returned to growth in July while the recovery among manufacturers built further. The services PMI rose from 47.1 to 56.6 this month, surpassing the 50.0 level that denotes the difference between industry expansion and contraction. Meanwhile, the UK's manufacturing PMI rose from 50.1 to 53.6.

These leave both industries sitting on higher PMI indices than the Eurozone, while either besting or broadly matching those of France and Germany.

"Trade-oriented production barely grew in July across Europe according to the July PMI surveys. In Germany, output was apparently unchanged in July (50.0), although up from the weak 45.2 in June. In France, the manufacturing index edged slightly lower to 52.0 from 52.3 in June. The UK fared better," says Kallum Pickering, a senior economist at Berenberg. "The survey data suit our call for a tick-shaped recovery that involves a rapid, but partial, snap-back in economic activity as soon as economies re-open, followed by a slower sustained recovery thereafter that eventually reaches and exceeds the pre-COVID level of GDP some two to three years from now."

Above: PMI indices for major European economies. Source: Berenberg. Click for larger image.

Germany's services PMI rose from 47.3 to 56.7 while its manufacturing index rose from 45.2 to 52.0. The French manufacturing PMI fell from 52.3 to 52 in July, though its services index rallied from 50.7 to 57.8.

The Eurozone manufacturing PMI rose from 47.4 to 51.1 while the services PMI advanced from 48.3 to 55.1.

It's not clear if this dynamic will be confirmed by official data, much less what it would mean for Sterling, although it certainly contradicts the popular perception.

PMI surveys measure changes in industry activity by asking respondents to rate conditions for employment, production, new orders, prices, deliveries and inventories. A number above the 50.0 level indicates industry expansion while a number below is consistent with contraction. The survey results often correlate with official measures of output, although they can often be wide of the mark too.

"Many firms who respond to Markit’s survey do not simply report whether output is higher or lower than in the previous month. Instead, some businesses just provide a vague sense of whether output is above or below recent norms, and this proportion likely varies over time. This makes the PMI particularly hard to interpret after a huge fall in the level of output," says Pantheon's Tombs.