The election of a new government with views antithetical to a strong currency has depressed the New Zealand Dollar, but the risks are overdone says a leading New Zealand bank.

The New Zealand Dollar is likely to rise despite analysts' negative views, says Jason Wong, an Auckland-based foreign exchange analyst with BNZ.

Since the election in October, the New Zealand Dollar has weakened by over 4.5% (versus a basket of the most traded currencies) due to growth concerns associated with the policies of the parties in the new coalition government.

The Pound-to-New Zealand Dollar exchange rate has risen 2.75% in the past month as a result of this politically-inspired Kiwi weakness while the US Dollar has advanced 2.25% and the Euro 1.66%.

Out of the 32 most traded global currencies, ony two have fallen more than the NZD - the Turkish Lira and the Mexican Peso.

The main policy areas weighing on the Kiwi are those relating to foreign investment, trade and immigration and those relating to the Reserve Bank of New Zealand (RBNZ).

The policies of the new government have a populist, nationalist feel, in line with the current global trend, and therefore seek to reposition New Zealand's interests first (sound familiar?).

Proposals to limit foreign investment in New Zealand property and to cut immigration dramatically - by at least 55% or more - are all suggesting to markets that New Zealand's economic growth rates are likely to slow.

If enacted the policies would reduce demand for the Kiwi and impact negatively on growth by lowering immigration which is seen as a source of increased demand - both of which would weaken the Kiwi.

Full Employment Reform at the Reserve Bank

The reforms proposed by the new government for the RBNZ are also likely to weigh on the Kiwi, they argue.

The RBNZ sets the base interest rate on which all other banks base their interest rates.

How does this impact on the currency?

Currencies generally follow interest rates up and down because higher interest rates attract money from abroad due to the promise of higher returns, which in turn increases demand for the currency.

The new government is proposing the Reserve bank reforms its mandate to include the promotion of 'full employment', but in order to do this, the RBNZ will probably keep interest rates low, to make borrowing cheaper and encourage businesses to expand and create jobs.

Lower interest rates will in turn pressure the Kiwi lower.

But, the Kiwi Might be Too Weak

Whilst the new government's policies have pushed the NZ Dollar down, Wong thinks fears are overdone and the Kiwi has weakened far enough - too far even.

"Our working assumption remains that the NZD over-reacted to domestic political change and this force will fade over time, particularly as more details on policy are released and the market gets more comfortable with the new government," says Wong in a note to clients.

Wong sees no evidence yet that the government will be as anti-Kiwi as markets have feared.

In relation to curbs on foreign ownership and investment, he notes that the only policy to have been tabled so far is to prohibit foreign ownership of existing New Zealand homes, which only accounts for 3.0% of the market.

It is true that Winston Peters, the head of the New Zealand First party, gave a strongly anti-capitalist speech when forming the government but BNZ's Wong dismisses this, saying:

"The night he chose Labour to form a government, Deputy PM Peter’s speech talked of fighting capitalism. That’s scary sounding at face value, but for all the talk about a significant change in economic direction the reality is that we’ll likely see only a minor shift, in our view."

Is the Price is Right?

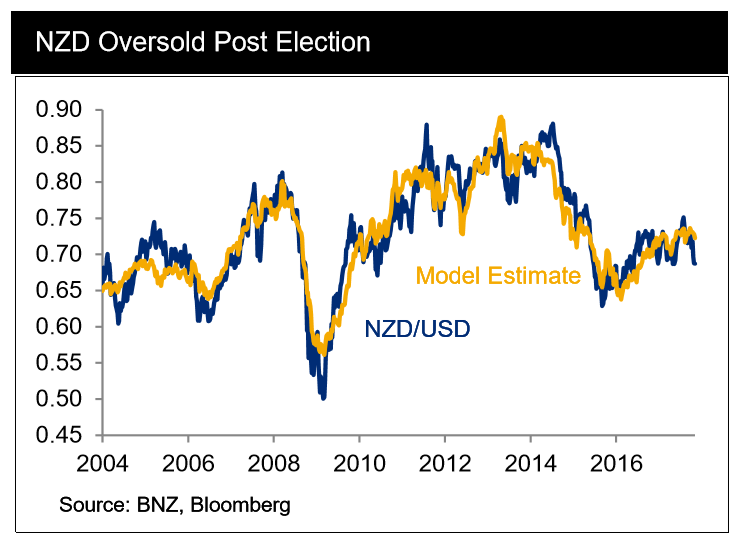

Currency analysts sometimes use what is called 'fair value models' to estimate what the 'true' value of a currency is using economic fundamentals, and often this differs from the actual market value.

When this happens the assumption is that the two will move closer together over time as valuations become more accurate.

In the case of the New Zealand Dollar BNZ's Wong notes how the current market value of NZD/USD at 0.6923 is well below his model's fair value estimate of 0.72-0.73.

This suggests two things - a) that the actual market value is too low, which for NZD/USD means an overly weak NZD; and b) that the market value will rise in the future to close the gap, which for NZD/USD implies a strengthening of the Kiwi.

"A fading of the NZ political risk premium supports a closing of the valuation gap over the near-term and a broadly based recovery on most crosses," says Wong.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.

Next Week's RBNZ Meeting

The RBNZ rate meeting next Thursday (November 9) could very well provide the moment when the Kiwi starts its recovery.

This is because, on balance, Wong thinks the central bank will raise its inflation forecasts, which, in turn, will lead to heightened expectations it will raise interest rates to medicate against the higher inflation.

"Next week's RBNZ MPS should be NZD-supportive as the Bank lifts its inflation forecasts. The Bank might not yet be willing to admit a tightening bias, but the direction of change in view should be clear."

The bank is currently as neutral as Switzerland in its own expectations concerning whether or not to raise interest rates, but Wong sees it slowly shifting to a more hawkish stance - hawkish meaning in favour of higher rates.

There are many inflationary pressures which are likely to impact on the outlook.

The weaker currency is one factor since it pushes up the prices of imports; higher global commodity prices is another factor, the higher than expected Q3 CPI result (a 0.3%) a further indicator, a leap in the minimum wage and Labour's generous spending plans, also further drivers.

"The overwhelming weight of evidence since the RBNZ’s August MPS points to higher inflationary pressure," says Wong.

Against this, the RBNZ will have to consider what sort of "growth pothole" the new government's policies will create in the short-term.

But since it is Wong's view that political risks are overdone, he actually expects RBNZ to revise up their growth forecasts, and, "bring forward the projected first rate hike for the cycle (previously late-2019)."

This is likely to push up the New Zealand Dollar.

"It’s early days, but the NZ Trade Weighted Index (TWI) appears to have found a floor over the past week, perhaps suggesting that selling pressure seen post-election is drawing to a close.," concludes Wong, who is in no hurry to alter his previous forecast, despite the election result.

"Putting it all together, we have no great urge to change our NZD projections, which have the currency anchored around USD 0.69-0.70 through the next 12 months," says the analyst.