The NZ Dollar trades softer following the RBNZ policy event but some strategists will see weakness as an open invitation to load up on fresh bets for further appreciation.

Expect yet more strength in the New Zealand Dollar argue analysts at Westpac’s institutional banking arm.

The call comes as New Zealand’s currency continues to be one of the best performing currency's in G10.

Indeed, the Pound to New Zealand Dollar was this week seen testing the 1.77 floor again.

There is notable support for GBP/NZD at this level, so from a technical perspective, a break below here will be difficult to achieve.

Nevertheless, the message on NZD from Westpac's in-house G10 FX model is clear - the currency is biased higher.

“The G10 FX model makes an aggressive bet on kiwi for the week ahead, the portfolio running with a 31% NZD long, the most aggressive NZD long held by the model in more than a decade,” says Richard Franulovich at Westpac.

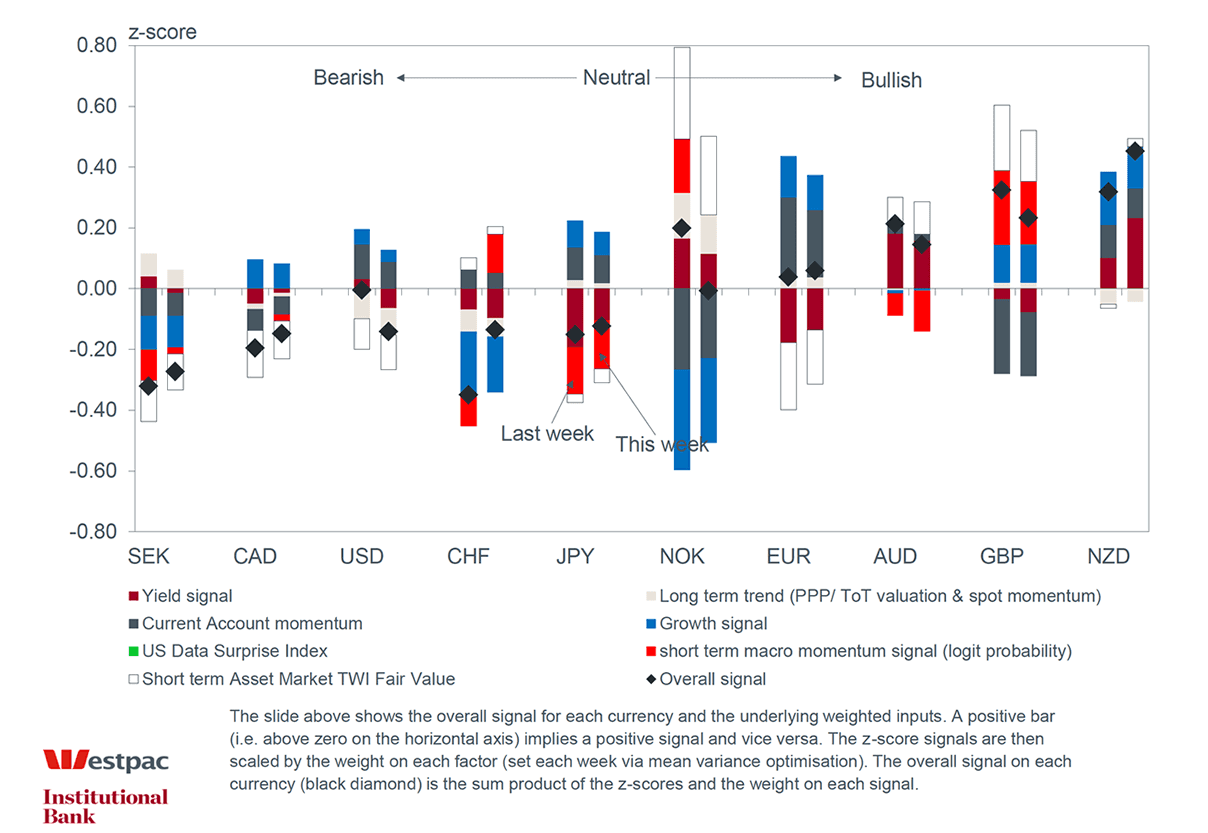

The Westpac G10 FX model is a multi-factor approach to systematically trading the G10 currencies.

The forecast model identifies the relative attractiveness of the G10 currencies based on 9 dynamically weighted macro-economic factors.

The 9 factors are based on a combination of; 1) modifications to the "standard FX model" (i.e. carry, trend and value); and 2) various signals sourced from Westpac's suite of FX indicators.

Latest Pound / New Zealand Dollar Exchange Rates

| Live: 2.3521▼ -0.03%12 Month Best:2.3553 |

*Your Bank's Retail Rate

| 2.2721 - 2.2815 |

**Independent Specialist | 2.3192 - 2.3286 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Why so Positive on the NZ Dollar then?

According to Franulovich the NZD is the standout bet in the G10 model mostly because of the country’s impressive economic growth profile.

Last week it was reported that annual growth in New Zealand stands at over 3%.

Yield and valuation signals for the NZD are also in play, see blue, marone and white bars for NZD:

NZ’s positive growth story is hardly newsworthy though it is notable that NZ has jumped back to the top slot according to our growth signal in recent weeks.

“NZ’s attractive yields are hardly newsworthy either, though our NZ yield signal has nevertheless continued to firm, the higher beta NZ fixed income market underperforming during the bigger global decline in fixed income markets recently,” says Franulovich.

NZD’s short term valuation signal has also improved, the currency mostly consolidating in the last month while dairy prices and yield support has continued to firm.

Standard Charterd Warn NZD's Supportive Drivers are Waning

However, not all analysts are backing the Kiwi blindly.

The NZD has benefitted lately from high local bond yields, a surge in dairy prices, upside surprises to New Zealand data and a weak USD.

"We see most of these factors waning, limiting further NZD gains. Moreover, the unusually low volatility over the summer months may be coming to an end," says a strategy note from Standard Chartered.

Remember the Thursday 22nd RBNZ policy meeting. Some analysts suspect Governor Wheeler and his team may cut interest rates again.

This would be a surprise and we would expect some weakness in the NZD to transpire if this were the case.

Indeed, although the latest dairy auction revealed yet another price gain, prices were up by 1.7%, the retreat in volumes sold, down 4.5% proved to arrest pre-auction NZD gains.

In the wake of the volume shortfall, (the market assumed another gain) we witnessed NZD sliding lower against a number of major competitors.

RBNZ: Concerned About Strong Exchange Rate

The NZD trades softer on Thursday the 22nd September following the RBNZ meeting in which no change to the country's OCR was announced.

However we get the sense that that RBNZ is getting increasingly agitated over the sky-high valuation of the NZD.

In the accompanying statement the RBNZ reflected:

"Weak global conditions and low interest rates relative to New Zealand are placing upward pressure on the New Zealand dollar exchange rate. The trade-weighted exchange rate is higher than assumed in the August Statement."

As such, some action directly targetting the value of the currency could be warranted:

"The high exchange rate continues to place pressure on the export and import-competing sectors and, together with low global inflation, is causing negative inflation in the tradables sector. A decline in the exchange rate is needed."

Presumably a cut to the interest rate would be one route of achieving such an aim, however with interest rates at 2.0% New Zealand remains head and shoulders above other nations and will continue to attract investor capital seeking out higher yields.

Therefore it will take more than just one 25 basis point rate cut to soften the NZD.

The RBNZ would therefore have to look at avenues to achieve devaluation, but of course it would then risk breaking the deal set at the G20 meeting in Shanghai that countries will not seek to devalue their currencies.