The New Zealand Dollar continues to recover in the mid-week session but longer-term is at risk of falling in value by up to 10%.

The NZ dollar continues to move higher as the October recovery remains intact. The lates bout of NZD appreciation comes after the RBNZ has communicated it is nervous about cutting interest rates further.

In a speech on the 14th of October Governor Wheeler said further rate cuts must be constrained by the fact that there is little evidence that reducing rates further will boost growth and further rate cuts risk pouring more fuel on an already blazing housing market.

The risks of a further interest rate cut are therefore greatly reduced and, in our view, this is a big positive for the New Zealand currency's outlook.

The British pound to New Zealand dollar exchange rate (GBPNZD) remains caught in the September / October downtrend; the pair has fallen from the 2.45's in September to the present levels around the 2.30's.

However, while the risks for a further interest rate cut at the RBNZ have receded analysts at BNZ are still pricing in one more interest rate cut ahead - a move that could catch markets by surprise and therefore poses a significant risk to the NZD's current rally.

Latest Pound / New Zealand Dollar Exchange Rates

| Live: 2.3509▲ + 0.1%12 Month Best:2.3553 |

*Your Bank's Retail Rate

| 2.271 - 2.2804 |

**Independent Specialist | 2.318 - 2.3274 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Gains Could Extend for Now

Despite the jitters seen at the time of writing it is worth pointing out that the pound to New Zealand dollar exchange rate remains in a technical downtrend and momentum indicators continue to advocate for further declines.

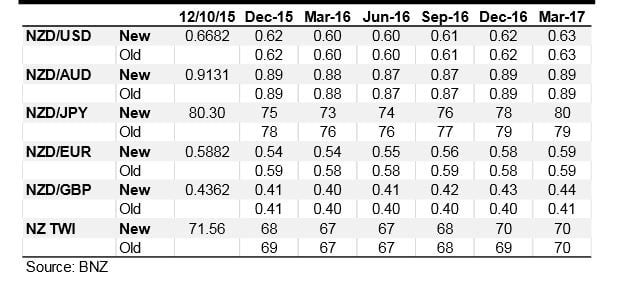

A new exchange rate forecast briefing from Bank of New Zealand (BNZ) has meanwhile confirmed the prospect for further gains in the NZD are possible:

"This NZD rally could persist, in the near-term at least, thanks to the continued exit of short positions against other risky assets.

"For example, Asian currencies could well extend their recent retracement rally against the USD, especially if China decides to fix the CNY stronger in coming days. Part of the Asian FX weakness had its roots in expectation of a weaker CNY into year-end, a prospect that has markedly dimmed over the past fortnight."

Strategists say they would not be surprised to see a break of 0.67 in NZDUSD, if the buoyant risk appetite persists.

Forecasting New Zealand Dollar Declines Longer-Term

Concerning the longer-term outlook the prospect of a reversal in fortunes for the New Zealand dollar is likely warn analysts at BNZ.

BNZ's Raiko Shareef says he sees 10% downside ahead:

"We spend little time herein agonising about the RBNZ’s near-term path. We still forecast another 25bp cut by year-end, slightly favouring the October meeting.

"Our economic forecasts, both in GDP and employment terms, are markedly less optimistic than the RBNZ’s. The prospect of a drought counters some of the positive vibes brought about by the dairy price recovery.

"The uninspiring economic outlook, combined with a higher volatility world, leaves us comfortably forecasting a 10% depreciation in NZD in six months from today’s levels, to 0.60 by March 2016."

BNZ advise they have pared back their forecast pace of USD appreciation against major currencies.

"But we have left our NZD and AUD forecasts unchanged, wary of spikes in market volatility that would see these risk-sensitive currencies correct sharply," says Shareef.

The AUD's recent recovery has come alongside a smart recovery in Asian EM currencies and a generally softer US dollar this far in October.

"We continue to forecast 70 cents for year-end, partly in anticipation of renewed market volatility out of the 17 Dec FOMC - whatever the outcome," says a note from BNZ's sister bank ANZ.

GBP/NZD Now Oversold

Analysis of the 1 day pound / New Zealand dollar charts confirms the GBP/NZD is now oversold and presumably due a period of consolidation or recovery.

The Relative Strength Index (RSI) is reading at 24.3 - anything under 30 suggests an instrument is oversold. There will be those in the market who are looking to capitalise on a comeback by the British pound.

However, we do must be aware that timing the recovery in the RSI back above 30 is notoriously hard and we would therefore hesitate to call the recovery. Watch the UK data calendar which gets livelier from Tuesday the 12th for fundamental cues to a GBP/NZD rally.

The Commodity Price Decline is Not Yet Over

For the New Zealand, Australian and Canadian dollars the movement of commodity prices remain central to their outlooks.

In short, should the downtrend in commodity prices resume you can expect the end of the rallies on the dollar complex.

Copper and oil prices have rebounded and numerous senior industry figures talked of the worst now being over.

"We agree that the downside price risks are receding as supply restructuring is gathering pace, but the bottoming out process is likely to last for a while yet," say Barclays in their Commodity Weekly brief to clients.

If past patterns are any guide, Barclays argue, there is unlikely to be a sustainable improvement in the prices of either commodities until global GDP starts to improve and there is little sign of that yet.

The key ingredient that is missing this time round is any significant recovery in the global economy to boost demand it is argued.

During the financial crisis the price recovery was supported by average global GDP growth from the second quarter of 2009 onward of 4%, 5.3%, 5.1% and 6%.

"Restocking all the way through the oil and copper distribution chain magnified the underlying demand improvement and resulted is sustained periods of very strong demand growth," says analyst Kevin Norrish at Barclays.

Likewise the recovery from the Asian financial crisis took place on the back of a spurt of above-trend global growth, averaging over 4.5% from early 1999 into 2000. Global growth also averaged over 4.5% for a considerable time as commodity prices begun a sustainable recovery from their 1980s lows.

"Thus while we do not expect any further significant declines in oil or copper prices the prospect of the type of rebound that has characterised previous recoveries looks slim. The bottom is probably in, but it is likely to prove a long one," says Norrish.