In one scenario envisaged by the Bank of England - where the global debt bubble pops - the British Pound could fall 27%.

The Bank of England does not issue foreign exchange forecasts; but this doesn't mean they don't forecast the Pound.

The stress tests of U.K. banks carried out by the Bank of England give insights into their forecasts for the British Pound under various economic scenarios pertaining to the nature of Brexit in March 2019.

Assumptions on the Pound's future value are revealed in the Bank's latest Financial Stability Report - issued on November 28, 2017 - the result of which proved good news for the UK financial sector as all the country's major banks look set to remain viable under even the worst-case Brexit scenario.

A disorderly Brexit - where the UK exits the EU without a deal in place - would see all lenders keep their heads above water and avoid collapse, or the need for a bail-out.

What makes for a disorderly Brexit are assumptions on economic growth, employment, interest rartes and the exchange rate.

It is the exchange rate that we at Pound Sterling Live would be inclined to focus on.

In the Bank's Financial Stability Report it is revealed that, "in the stress scenario, there is a sudden reduction in investor appetite for U.K. assets and the Sterling exchange rate falls to its lowest ever level against the Dollar."

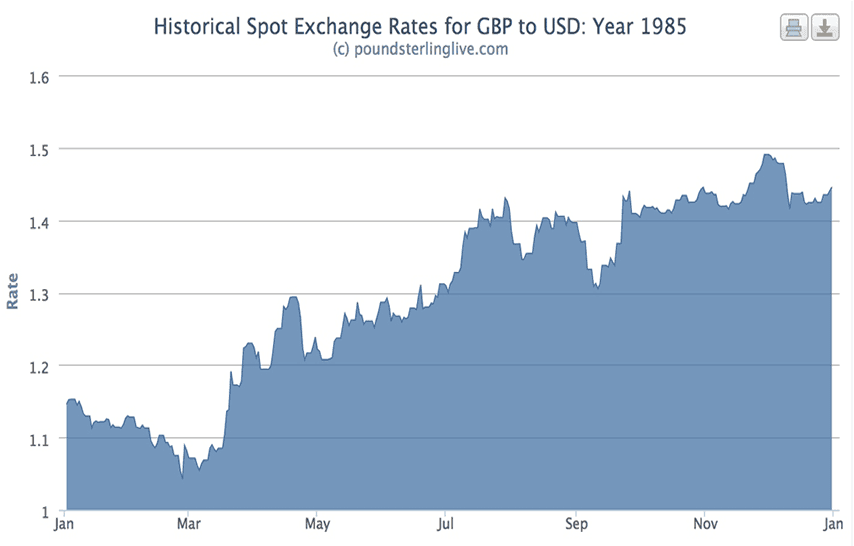

Data shows that the lowest ever Pound-to-Dollar exchange rate was reached at 1.0420 on February 26, 1985.

Our data is supplied by the Bank of England and therefore gives us a hint that this is close to their forecast scenario.

A GBP/USD exchange rate at 1.0420 implies a Pound-to-Euro exchange rate of 0.87 assuming today's EUR/USD exchange rate of 1.1887; so parity would easily be broken.

Yet what the Euro's reaction to the EU referendum of June 2016 shows is that it too is responsive to Brexit-orientated negativity, therefore we would assume a lower EUR/USD exchange rate in the event as the European Central Bank would look to extend its asset purchase programme and delays its first interest rate rise in years.

Even if the EUR/USD were to retreat back to 1.10, that still gives us a GBP/EUR exchange rate at 0.94 if GBP/USD falls to all-time lows. And let's say the EUR/USD climbs to 1.25 - where many analysts believe the pair's current fair-value is right now - we could see the GBP/EUR going down to 0.83.

Of course the details surrounding the true figures adopted by the Bank are not made available as per their policy not to issue exchange rate forecasts, but we do get a sense of what could go wrong.

27% Fall in the Value of the Pound

The Bank believes risks to the UK economy and the Pound extend beyond Brexit - part of their stress testing scenarios accounted for a massive deterioration in global economic performance as the global debt bubble bursts.

"High levels of debt can result in larger downside economic risks in foreign economies. If they materialise, these risks can spill over to the United Kingdom through trade and financial linkages," notes the Bank.

The risk environment was reflected in the 2017 stress-test scenario.

The annual cyclical scenario for the 2017 stress test captured a wide range of domestic and global risks. In particular, the test incorporated:

"A severe consumer credit impairment rate of 20% over the first three years of the stress, as unemployment and interest rates increase sharply. The resulting losses across the banking system of £30 billion (of which £21 billion are incurred by the major banks in the stress test) are £10 billion higher than in the 2016 stress test.

"A sudden increase in the return investors demand for holding sterling assets and a 27% fall in the Sterling exchange rate index."

The Sterling exchange rate index is at 77.63 at current effective exchange rate measures, thus we could see it fall to 56.67 under this scenario - easily an all-time low.

In short, if the global economy is hit by a debt-induced economic slump, the Pound is at risk of deep falls.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.

Losing the 'Kindness of Strangers': The Mechanism to a Sterling Slump

While the Bank doesn't issue exact exchange rate forecast targets, we do know the Bank of England's thinking when it comes to the mechanisms that would trigger a sharp fall in the value of the British Pound.

The Bank notes, the United Kingdom may be vulnerable to a reduction in foreign investor appetite for UK assets as the country has a large external balance sheet and current account deficit.

A current account deficit means the UK imports more than it exports, while the inflows of earnings realised on assets owned by U.K. nationals outside of the country are lower than they once were.

A current account deficit ultimately means that domestic investment is greater than saving, and must be financed by capital from overseas; the U.K. current account has been persistently in deficit since 1999.

This leaves the U.K. dependent on foreign investment inflows to keep the value of the Pound propped up.

Bank of England Governor Mark Carney has famously said of the situation that the UK remains dependent on the "kindness of strangers"; the country requires about £100BN annually to finance its current account deficit and this would be jeopardised by a loss of confidence in the U.K.

The Bank notes recent capital inflows, which have focused on direct investment and long-term securities, appear less vulnerable to reversals than during the run-up to the financial crisis.

"However, the United Kingdom is vulnerable to a reduction in foreign investor appetite for U.K. assets. If that occurred, credit conditions would be expected to tighten, domestic demand would weaken and the Sterling exchange rate would depreciate," reads the Financial Stability Report.

Overseas investors must remain willing to continue holding UK assets if Sterling is to remain elevated.

The Bank notes sharp falls in foreign investor appetite for UK assets could lead to falls in UK asset prices and a tightening in domestic credit conditions.

This could be triggered, for example, by perceptions of weaker or more uncertain UK long-term growth prospects.

"Such a disruption could also drive further Sterling depreciation, potentially triggering a build-up in inflationary pressures, and lead to a downward adjustment in domestic demand. This could worsen the trade-off between growth and inflation," says the Bank.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.

But, Brexit Outlook Improves and Pound Looks to Strong Year-End

The worst-case scenario envisaged in the Bank's modelling might however be avoided, if the latest developments on the Brexit front yield a stable exit from the E.U.

The Telegraph reports U.K and E.U. negotiators have confirmed that an agreement-in-principle has now been reached, opening the door to a potential breakthrough in the talks this December.

Further talks confirm another meeting of the U.K. cabinet has approved proposals to pay the E.U. anywhere between EUR45-55bn after Brexit due to long-term liabilities; confirmation of Government unity on the matter.

Of course both sides of the Brexit commentariat in the U.K. are scathing in their assessment of the developments with Remainers saying this is further proof of the unneccessary cost of Brexit (this money was going to be paid anyway!) and Brexiteers saying the bill is too much (this group are not content on simply having a Brexit, they want a confrontational Brexit!).

Whatever the chattering classes say, the verdict from the market is positive as the breakthrough - which still requires all the remaining 27 E.U. states to agree to - will finally allow talks to move on to the issue of trade and the future relationship which should finally allow businesses some clarity.

"If made official, this would be a major achievement for Prime Minister May but for the time being its nothing more than hope. Although Ireland's political troubles and their border issue could remain a problem, the Brexit bill agreement should be enough to unlock the talks," says Kathy Lien, Director at BK Asset Management.

This clarity should feedback into a stronger Pound.

“We are still taking as our base-case a view that the UK finds a way to promise sufficient clarity on the financial settlement to allow for a positive surprise, which is the key to our relatively bullish GBP forecasts,” says Shahab Jalinoos, a foreign exchange strategist at Credit Suisse.