- GBP's all-time lows a side effect of PBoC defence of RMB

- Recent JPY interventions & poor GBP liquidity in Asia key

- But losses merely precursors to stabilisation for GBP et al

- PBoC & Fed policy divergence the main driver of volatility

- Important political event in China key to short-term outlook

- May result in stabilisation or recovery for many currencies

- Potentially very bearish for U.S. Dollar pairs in short-term

Image © Adobe Images

Pound Sterling's recent fall to record lows may appear linked to government policy but a wealth of information has since suggested strongly that it was really just a table turned or a glass broken in a scrap between the market and a big hitter of a heavyweight puncher called the Peoples' Bank of China (PBoC).

Sterling's falls have impacted public conversation about government policy so readers should understand what appears to be the effect of interest rate divergence between the Federal Reserve (Fed) and PBoC, and the impact this has on currencies in the managed-floating Renminbi system including Sterling.

For readers who prefer not to engage in longer reads, the most important point here is that the Pound is an international currency and sometimes Sterling exchange rates will do things that have little or nothing at all to do with developments taking place in the United Kingdom itself.

For those who do like long reads, there is something of a dissertation below setting out how speculative bets against China's currency very likely interacted with inadequate Sterling liquidity in Asia trading hours in order to drive last Sunday or Monday's fall to all-time lows in some British exchange rates.

"Walking onto the New York trading floor this Wednesday morning, and the questions were already flying thick and fast. USDCNY has broken out to 7.25. The Chinese currency has now lost 15% against the USD since the start of Q2 – a massive move," says Ajay Rajadhyaksha, head of macro research at Barclays.

Above: Dollar-Renminbi rate (USD/CNH) shown at daily intervals alongside USD/GBP (orange), USD/EUR and USD/JPY. Note the very close relationship between USD/CNH and USD/GBP. Click image for closer inspection.

Above: Dollar-Renminbi rate (USD/CNH) shown at daily intervals alongside USD/GBP (orange), USD/EUR and USD/JPY. Note the very close relationship between USD/CNH and USD/GBP. Click image for closer inspection.

"Sure, other prominent currencies such as the EUR and the GBP have performed even worse, but not by much. Moreover, the pace of CNY weakness is accelerating," Rajadhyaksha wrote in a note last Wednesday co-authored with London and Singapore-based colleagues.

The above from Barclays is relevant because Sterling's recent fall to historic lows against the Dollar and other currencies took place in last Monday's Asia trading session, which corresponds with the overnight hours of the Sunday in the UK and is a period in which the Pound does not usually trade all that much.

It is also highly relevant that last Monday's trading volumes in Sterling were three times their normal levels and came close to matching turnover in the much larger Chinese Renminbi, while daily trading remained far above its typical levels throughout the entirety of the week.

"USD-CNY broke 7.20 to reach levels last seen in early 2008. The fixings have been rising much faster in recent days, even as reports emerge about counter-cyclical measures," writes Paul Mackel, global head of FX research at HSBC, in a Wednesday research briefing.

"This level has been keenly followed by the FX market because it was a level that held during the period of heightened US-China trade tensions in 2018-19. Many market participants probably thought that spot would take longer to hit this level and that there would be more friction around it," he added.

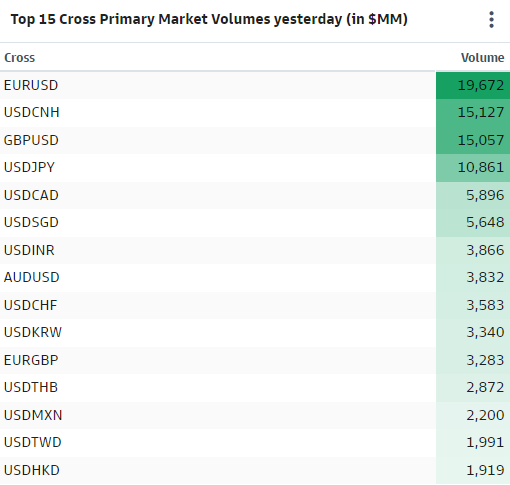

Above: FX spot turnover on EBS and RUT trading platforms from Monday, 26 September. Source: Goldman Sachs Marquee.

Readers should also note at this point that trading in the Pound surpassed that of the Japanese Yen through all of last week and likely due to direct intervention in the currency market from Tokyo to stem the Yen's losses during the prior week, losses that had become a concern for the government of Japan.

In addition, it is most relevant that by Wednesday of last week China's Renminbi had become the second most traded currency in the market after the U.S. Dollar, a spot that is typically taken up by the Euro, which would then normally be followed by the Renminbi, Japanese Yen and Sterling.

Readers will not necessarily be able to connect the dots outlined above but the author can and what follows is an attempt to help others do the same.

"While policymakers are clearly pulling out a range of administrative measures (and stealth intervention) to slow the pace of RMB depreciation, we are not convinced the PBoC prefers a particularly strong currency," writes Stephen Gallo, European head of FX strategy at BMO Capital Markets.

"The recent depreciation of various G10 currencies to new cycle lows further underscores our view," Gallo wrote in a Friday market commentary.

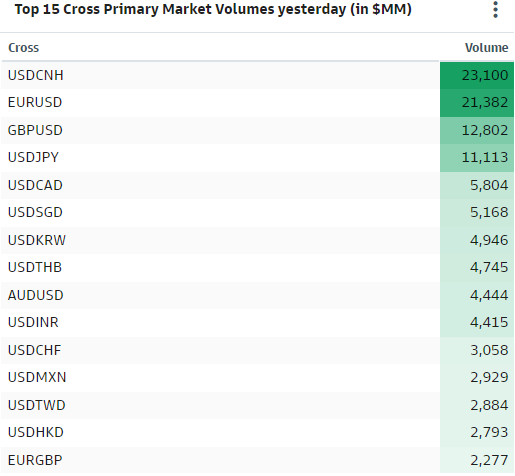

Above: Wednesday, 28 September. Source: Goldman Sachs Marquee.

The term "stealth intervention" may or may not be the best description for the market response to Chancellor Kwasi Kwarteng's budget, which saw Sterling rally for a time before being sold heavily against most currencies, though the concept is presented here as food for readers' thoughts nonetheless.

Most importantly, however, there was nothing stealthy about Sterling's fall in last Monday's Asia session - when the Pound actually reached record lows - and it is most noteworthy that Sterling stabilised during European trading that day before later going on to end the week higher in relation to many other currencies.

"China is getting more serious on the yuan. Here is a quick graphic of their slowly escalating commentary [the next graph below]," says Brent Donnelly, CEO of Spectra Markets and a veteran currency trader with time spent at hedge funds as well as global banks including Lehman Brothers and HSBC.

"With the China Party Congress on October 16, and the newly upped urgency from SAFE and the PBoC, it’s time to take profit on USDCNH longs. Rebuy in the 7.00 area," Donnelly said in Friday's AM/FX (anybody can sign up here).

Recent price action followed a lengthy depreciation of the Renminbi and came just weeks out from a highly important political event in the Chinese calendar that has without doubt catalysed PBoC actions that could prove quite supportive of Sterling and somewhat bearish for the Dollar during the weeks ahead.

Above: USD/CNH and PBoC actions since early August. Click image for closer inspection. Source: Spectra Markets.

Above: USD/CNH and PBoC actions since early August. Click image for closer inspection. Source: Spectra Markets.

"The scale of their firepower is credible, as the aggregate net foreign asset position of local banks reported by the PBoC turned notably more positive in 2021," BMO's Gallo said of this MUST-READ report from Reuters.

"But the rate of increase had already started to turn lower in Q2. It is therefore quite possible that state banks have been intervening on PBoC's behalf by selling foreign currency for some time," Gallo added.

At this point it becomes relevant that Reuters cited four sources last Thursday when reporting that the PBoC had instructed state-owned banks in China to prepare to sell U.S. Dollars offshore in order to place a floor under the Renminbi.

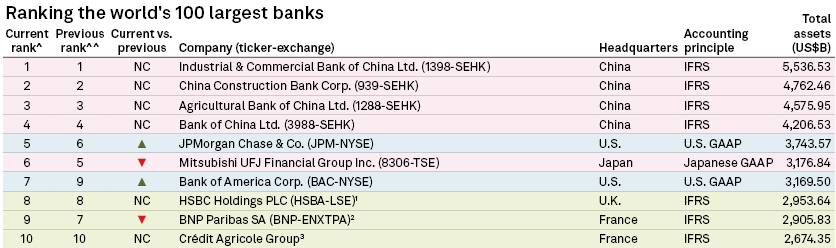

Such reports have to be taken seriously because China dominates the upper echelon of the international league table when banks are listed according to the size of their balance sheets while the PBoC itself wields the world's largest chest of FX reserves that were valued at a little over $3 trillion in August.

However, the trading volume figures outlined previously in this article are strong indications that this report emerged at least a few days after a very determined currency intervention began, while all of this makes it necessary for readers to understand at least a bit about the managed-floating Renminbi system.

Source: The World's 100 Largest Banks, S&P Global Market Intelligence.

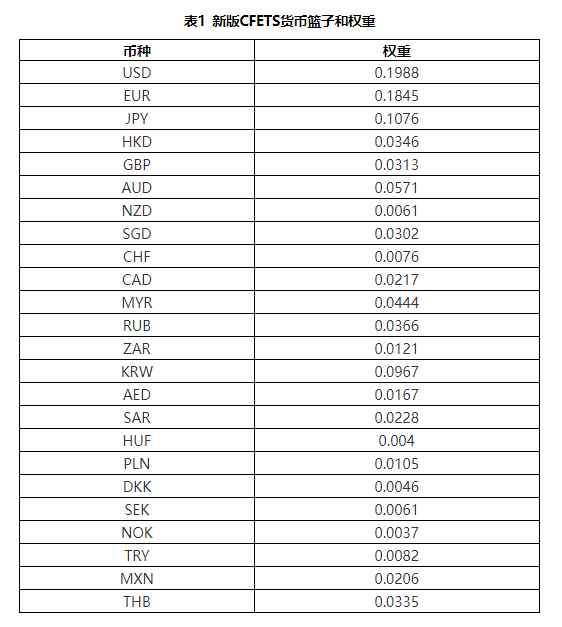

The managed-floating exchange rate system operated by the PBoC directly links Pound Sterling and all other currencies within the China Foreign Exchange Trade System (CFETS) index pictured below, to a Chinese Renminbi that has been under immense pressure from the U.S. Dollar during recent months.

The stated objective of the managed-float system is to keep the Renminbi "basically stable" against others in the CFETS index, which is important because if the Renminbi is falling sharply then this system requires that other currencies within the CFETS index must also fall to at least some extent.

"FX reserves have dropped by $200bn this year. Little wonder that investors are wary when the currency depreciates sharply. But, while the growth developments in China remain deeply worrying, we still believe concerns of a systemic crisis are overstated," Barclays' Rajadhyaksha said on Wednesday.

"This is simply investors leaving Chinese equity and bond markets, attracted by the highest US interest rates in many decades. It is not domestic savers losing confidence and fleeing the local economy, and is a far cry from the hundreds of billions of dollars of outflows that the country saw in 2015-16," he added.

The most important thing at this point is that the PBoC has recently cut its interest rates while providing other stimulus to the local economy and at a time when the Federal Reserve is lifting U.S. interest rates sharply in order to bring down high inflation rates that do not currently exist to the same extent in China.

Above: China Foreign Exchange Trade System (CFETS) Index.

Fed policy has resulted in widespread strength across U.S. Dollar exchange rates while this and PBoC policy has put huge pressure on the Renminbi, although all of these policy and price developments also had significant effects on other currencies due to the managed-floating exchange rate system.

This is because the managed-floating exchange rate system has a very, very, very, very clever way of converting the market's bets against the Chinese currency into even larger or simply more effective wagers against a whole bunch of other currencies including Pound Sterling.

It's not clear if this a design feature of the system or simply a coincidence but it is certainly a reality or byproduct of the system, and one that can also work in reverse, as the author thinks it is now likely to during the weeks leading up to the aforementioned political event that is of high significance in China.

"Chinese Golden Week is around the corner. We expect that authorities will try to squash any further disorderly moves going into this period and the October National People’s Congress," Barclays' Rajadhyaksha said last week.

"It is too soon to worry about systemic risk emanating from China. But if the CNY is truly on a path to further currency depreciation, which now seems very likely, it is more bad news for the rest of the world," he added.

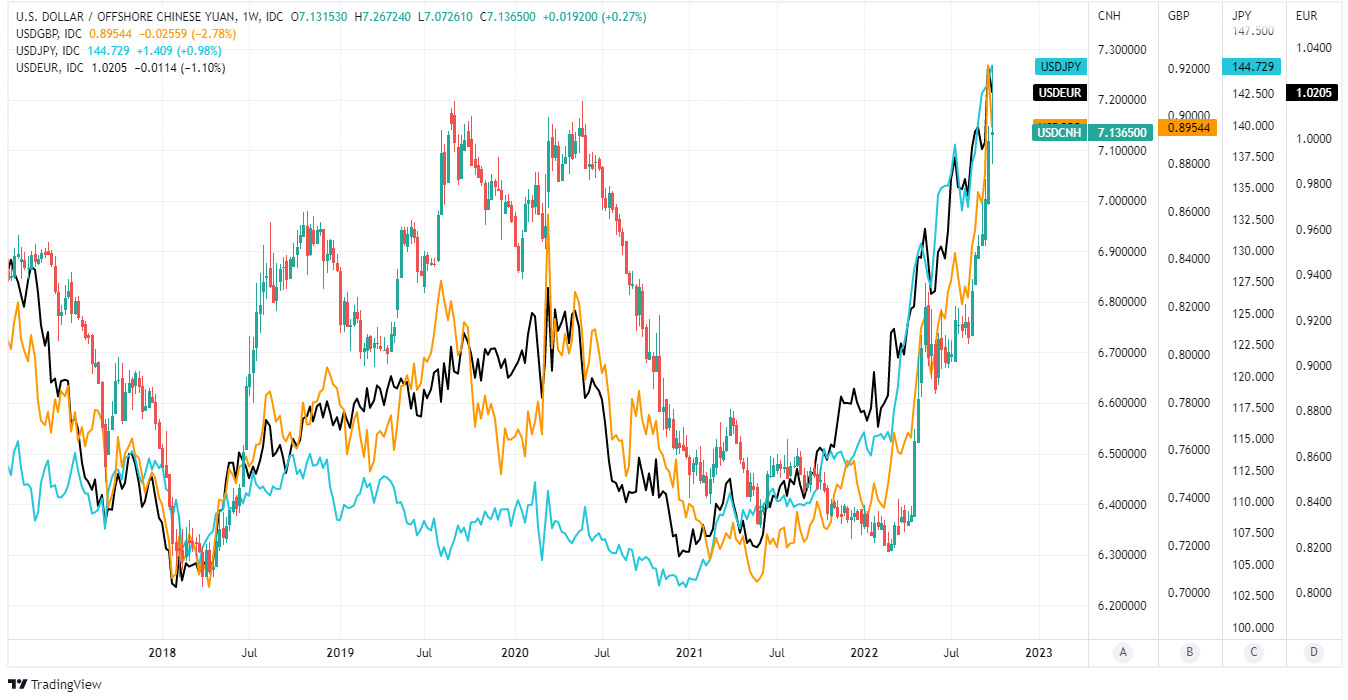

Above: Dollar-Renminbi rate (USD/CNH) shown at weekly intervals alongside USD/GBP (orange), USD/EUR and USD/JPY. Note the very close relationship between USD/CNH and USD/GBP. Click image for closer inspection.

Above: Dollar-Renminbi rate (USD/CNH) shown at weekly intervals alongside USD/GBP (orange), USD/EUR and USD/JPY. Note the very close relationship between USD/CNH and USD/GBP. Click image for closer inspection.

To an extent disorderly moves have already been squashed with Sterling ending last week higher against many currencies and the U.S. Dollar Index lower.

If the author is right about any of this then it's likely that many U.S. Dollar exchange rates will struggle in the weeks ahead while the Renminbi, Sterling and a whole bunch of other currencies will stabilise into mid-October.

However, and was pointed out by Barclays, what might be likely to happen after that is another matter entirely and much likely depends on both Fed as well as PBoC monetary policies, which are pulling in opposite directions and are in some ways holding lots of other currencies and economies as hostages.

"During yet another tumultuous week in financial markets, the dollar has dropped back over the past couple of days after intervention by the BoE (in the gilt market) and the PBOC (in the renminbi) provided a degree of relief across equity, bond, and currency markets. The greenback’s rally looks increasingly stretched and we think there is scope for further consolidation," says Jonas Goltermann, a senior markets economist at Capital Economics.

"But with Fed officials continuing to bang their hawkish drum, the key underlying driver of the dollar’s strength remains intact and the risk of a continued self-reinforcing dollar melt-up is high. At this point, significantly weaker US data (or an accident in US financial markets akin to this week’s Gilt meltdown) look like the only things which might change the FOMC’s mind," Goltermann and colleagues wrote in a Friday review of last week's developments in the markets.

{kind=link}