Image © Adobe Stock

Great expectations: the two successive 75 basis point hikes the markets are expecting from the Bank of England paves the way to an epic disappointment for the British Pound.

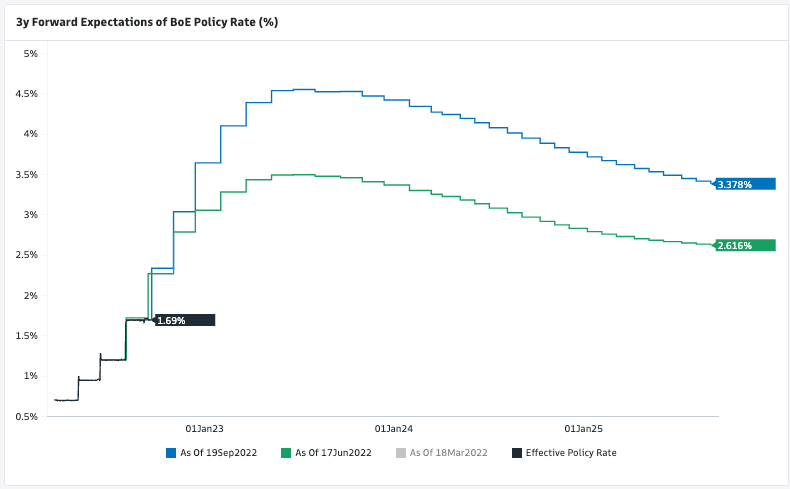

Money markets are now priced for 200 basis points of hikes over the next three decisions, implying the Bank will need to raise rates by 75bp points at two of those meetings.

This is more than is asked by any other developed market central bank.

Markets imply a 60% chance of a 75bp increase on Thursday, which would be its largest rate hike since 1989's 100bp move.

The pressure on the Bank to hike by such increments comes as other central banks raise rates at a clip: we have already seen the ECB raise rates by 75bp this month while the Riksbank raised rates 100bp on Tuesday and the Fed is expected to go 75bp on Wednesday.

The Bank of England must therefore at least match market expectations if it is to defend Sterling's current valuations: this is applicable not just against the Dollar but also the likes of the Euro and a host of other currencies.

"We expect the Bank of England to raise its policy rate 50 basis points to 2.25% at next week's monetary policy announcement, and follow up thereafter with a 50 basis point rate increase in November and a 25 basis point increase in December," says Nick Bennenbroek, International Economist at Wells Fargo Securities.

Such an undershoot at September's policy meeting would be outright bearish for the Pound, those looking to protect their international payments budget could consider locking in current rates or setting an order protect payment budgets.

"With Bank of England tightening set to lag the Fed and fall short of market expectations, we expect renewed downside in the pound," says Bennenbroek.

Above: Market implied expectations for Bank Rate. Image courtesy of Goldman Sachs.

This is an era in which economies favour appreciating currencies in order to minimise the impact of imported inflation: with the Dollar so strong, the cost of energy and commodity imports for non-producing countries are particularly eye-watering.

Central banks that are not seen to be hawkish enough in such a competitive environment understandably risk further devaluations and elevated-for-longer inflation.

Therefore keeping GBP/USD supported would understandably be a policy consideration for the Bank of England at upcoming meetings.

The Pound has suffered over the course of 2022 as the Bank has proven itself a reluctant hiker, often moving by increments below what the market was expecting.

And when it does meet market expectations - as was the case in August - it has a knack of issuing such sombre guidance regarding the outlook the market sells the Pound anyway.

"The GBP remains on the back foot," says analyst Valentin Marinov at Crédit Agricole. "Among the reasons for the decoupling between the FX and rates markets seems to be FX investors' scepticism that the MPC would be able to deliver on the hawkish market expectations."

The Pound to Euro exchange rate has fallen 4.0% in 2022 and is currently quoted at 1.1412, the Pound to Dollar exchange rate is down 15.50% at 1.1417.

"There has been an almost non-stop, albeit very measured, sell-off in the Pound since August 11, with a brief pause for a shake-out of the dollar bulls' positions. In turn, this momentum looks to be part of a downward wave since March," says Alex Kuptsikevich, senior market analyst at FxPro.

Last week saw the Pound fall to its lowest level since 1985 against the Dollar and lowest level since February 2021 against the Euro amidst fears of a Bank of England disappointment, ongoing demand for the dollar amidst gloomy market conditions and expectations for a marked UK economic slowdown.

The Bank of England is meanwhile expected to offer further details on its plans to sell the bonds it purchased under its quantitative easing programme back to the market, which would potentially raise the cost of government borrowing.

(Increased supply of bonds = higher yields paid on these and other bonds).

But, the government is to massively raise its borrowing requirements over coming months as the new government of Liz Truss seeks the funds to freeze household energy bills.

This means the Bank could be selling bonds just as the government is issuing greater quantities of bonds, thereby potentially creating funding stresses.

There is therefore potential for the Bank to delay its bond sell-off plans as it would not be keen to destabilise the market.

"Because the government plans have upset the gilt markets, the latest developments could further complicate the BoE’s own QT plans. Indeed, any evidence next week that the BoE may delay its gilt

sales plans could keep the UK real yields very negative to the detriment of the GBP," says Marinov.

The government's debt position will be more fully understood by Friday when the Chancellor Kwasi Kwarteng issues a 'mini budget', detailing the cost of the energy price cap and further measures to be taken on taxes and spending intentions.

"The ‘mini Budget’ label should be treated as a classic British understatement. Pandemic era-scaled fiscal intervention looks set to be confirmed," says Ross Walker, Chief UK Economist at NatWest Markets.

"A counter-intuitive start for a self-professed small-State government, but a largely unavoidable one given the severity and likely persistence of the energy shock," he adds.

NatWest says investors will be confronted by a tripling of net supply of government bonds in the face of an underlying deterioration in the public finances.

They forecast UK 10-year bond yields to climb to decade highs of 4.0% by early 2023 as a result of the increased supply.

The trajectory of UK borrowing appears to be another concern for international investors and helps explain why the Pound has found virtually no support from rising bond yields.

"We continue to expect Gilt yields to fall back and sterling to grind lower against the US dollar," says Jonathan Petersen, Senior Markets Economist at Capital Economics.

"Meanwhile, the global economic backdrop remains weak, particularly in other European countries and China. This, in turn, is likely to prove a headwind for cyclically sensitive economies like the UK," he adds.

Capital Economics' UK markets forecasts remain consistent with an outlook of slowing economic growth at home and weak appetite for risk in the context of a broad-based slowdown abroad.

They project that the UK 10-year bond yield will end this year at 2.5% amid increased demand for 'safe' assets.

In the absence of large shifts in yields between the U.S. and UK, they think the sensitivity of sterling (and other “high-beta” currencies) to shifts in risk sentiment will push down the GBP/USD exchange rate: their end-2022 forecast is 1.10.

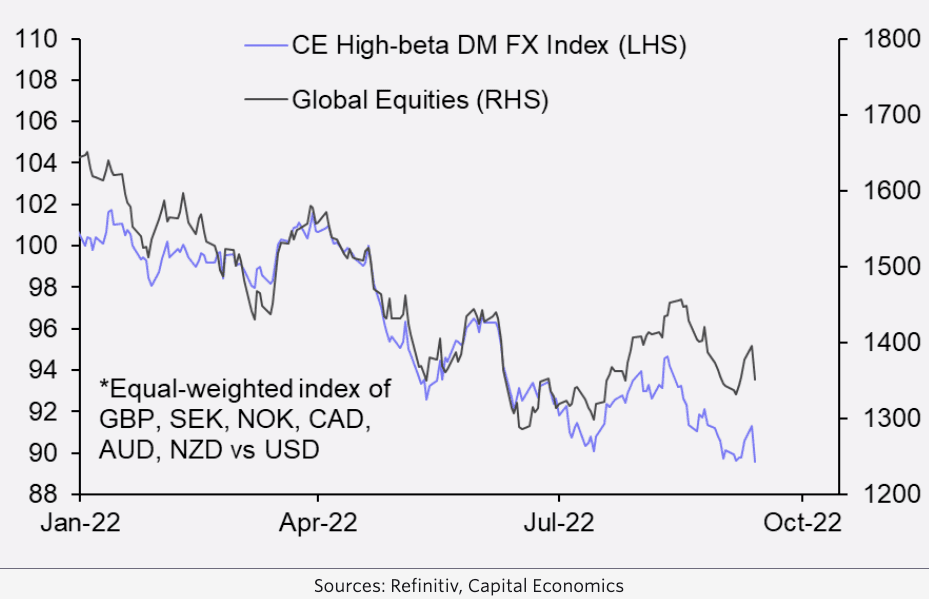

Above: GBP and peers track the ongoing decline in stock markets.