- BoE hikes 50bp

- GBP in "sell the fact" response

- Higher wages predicted

- Higher prices charged by firms expected

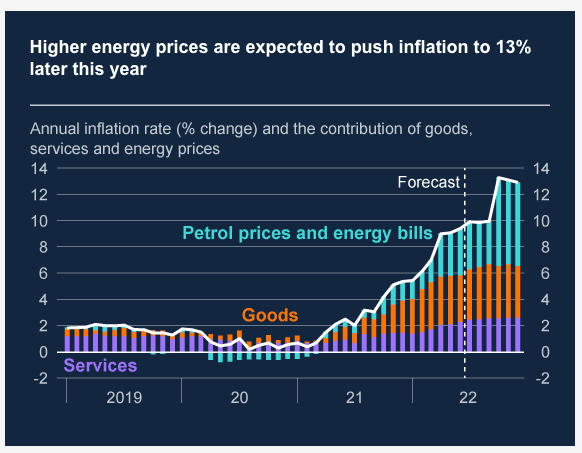

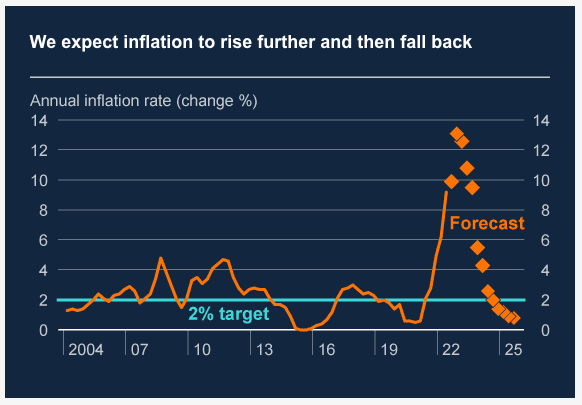

- Upgraded inflation forecasts

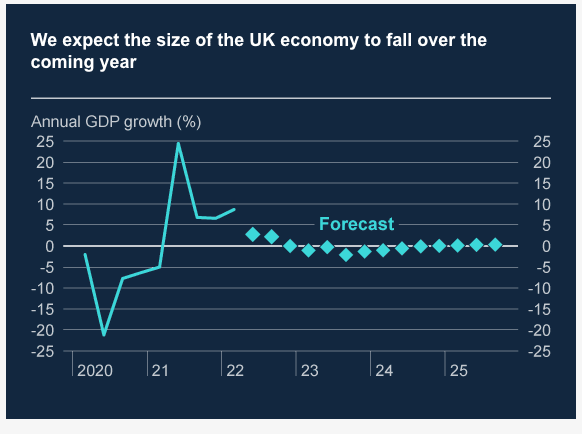

- Forecasts show no more economic growth likely

Above: Bank of England Governor Andrew Bailey speaks to the press following the rate decision.

The British Pound's fell sharply in response to an outsized 50 basis point interest rate rise by the Bank of England, a reaction that was largely in line with the predictions made by a number of analysts we follow.

However, predictions for an economic recession to take hold by the end of the year and last until 2024 made for a downbeat affair and will have contributed to the selling.

"The Bank of England has hiked rates by 50 basis-points while also now forecasting a recession lasting for five quarters," says James Smith, Developed Markets Economist at ING Bank.

Yet, there was a decidedly hawkish slant to the August policy decision and update which could underpin the Pound: just one member of the Bank's Monetary Policy Committee voted against the 50bp hike, instead opting for a smaller 25bp hike.

The Bank also restated its committment to "act forecefully" on inflation.

Altogether, the message from the Bank was consistent with the prospect of another potential 50bp hike in September, which should however keep Sterling supported. "Another 50bp hike in September seems plausible," says Smith.

Although the Pound initially declined in response to the announcement, volatility over coming hours is highly likely as the market navigates the incoming information and arrives at a final conclusion.

"The labour market remains tight, and domestic cost and price pressures are elevated. There is a risk that a longer period of externally generated price inflation will lead to more enduring domestic price and wage pressures," said the Bank in a statement.

Crucially, it maintained the statement first introduced in June that it "will if necessary act forcefully in response" to elevated inflation.

That line alone was responsible for the upgrading in the market's expectations for a 50bp hike today.

That the line remains in the August statement suggests further 50bp moves are likely, particularly given the Bank now forecasts inflation to peak at 13% in late 2022.

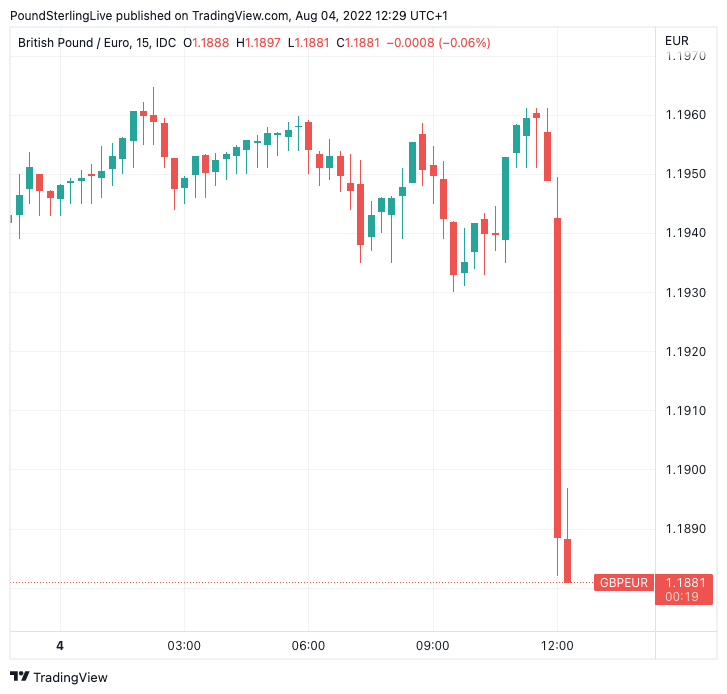

Above: GBP/EUR at 15 minute intervals.

In the Monetary Policy Report (MPR) the Bank's economists note inflationary pressures in the United Kingdom and the rest of Europe have intensified significantly since the May MPR and the MPC’s previous meeting held in June.

CPI inflation is now forecast to rise more than was forecast in the May Monetary Policy Report (MPR), from 9.4% in June to just over 13% in 2022 in the fourth quarter of 2022.

Inflation is expected to remain at very elevated levels throughout much of 2023, before falling to the 2% target two years ahead.

The United Kingdom is now projected by the Bank's economists to enter recession from the fourth quarter of this year.

This projection could have contributed to the Pound's initial decline following the decision.

"There were no surprises in the size of the rate hike, nor the voting pattern, yet the BoE’s narrative of further forceful tightening even as the economy heads into recession is a tricky one for growth-sensitive sterling," says Chris Turner, Global Head of Markets and Regional Head of Research for UK & CEE at ING Bank.

The Pound to Euro exchange rate is down half a percent in the half hour following the release at 1.1893, taking bank account euro quotes to ~1.1655 and quotes offered by payment specialists to ~1.1857.

The Pound to Dollar exchange rate is lower by 0.20% at 1.2115, meaning bank account rates for dollar payments are approximately at 1.1873 and those at payment specialists at ~1.2079.

The below chart from the Bank is quite remarkable in that it implies the UK economy will not grow again, at least for the next 3-4 years:

Despite the soft reaction by Sterling the narrative remains broadly supportive of the currency in that the Bank is concerned second-round inflationary pressures are building, which suggests the rate hike cycle is not about to slowdown.

"Firms generally report that they expect to increase their selling prices markedly, reflecting the sharp rises in their costs," said the Bank.

It added:

"The labour market has remained tight, with the unemployment rate at 3.8% in the three months to May and vacancies at historically high levels. As a result, and consistent with the latest Agents’ survey, underlying nominal wage growth is expected to be higher than in the May Report over the first half of the forecast period."

The Pound fell following the Bank's May MPR when it said its projections suggested inflation would fall quickly back to 2.0% over coming months, if the market's expected path of interest rate hikes were followed.

The market saw this as a dovish 'push back' by the Bank against market expectations for numerous further rate hikes, in turn prompting Sterling weakness over subsequent weeks.

But the Bank looks keen to avoid a repeat of this, saying "the Committee is currently putting less weight on the implications of any single set of conditioning assumptions and projections."

"All options are on the table" for future Bank of England meetings, Governor Andrew Bailey said in a press conference following the decision, adding there are "no ifs or buts" about the goal of reducing inflation to 2%."

Money markets nevertheless now expect the Bank to be in a position to cut interest rates in 2023 as inflation passes its peak and growth slows sharply.

The acceleration in interest rates today could therefore mean the rate at which the Bank cuts rates in the future could be quite steep, particularly given forecasts for a fall in inflation and growth.

For Sterling, this could be a headwind according to some strategists.

"The Bank of England has chosen to go down the aggressive rate hike path. But that also means rates will come down quite quickly once inflation comes down. Betting on sharp BoE rate cuts down the line is the scenario not priced into markets," says Viraj Patel, Macro Strategist at Vanda Research.

"What goes up must come down," he adds.