- A big week looms for GBP

- Bank of England to hike on Thursday

- Kwarteng to announce mini budget Friday

- Analysts resolutely bearish on GBP's prospects

Above: Chancellor Kwasi Kwarteng is the Pound's focus on Friday. Image: Gov.uk.

The Pound is set to fall further say analysts, although there is a faint prospect the currency finds redemption towards the end of the coming week when a Bank of England rate hike and the 'mini budget' are delivered.

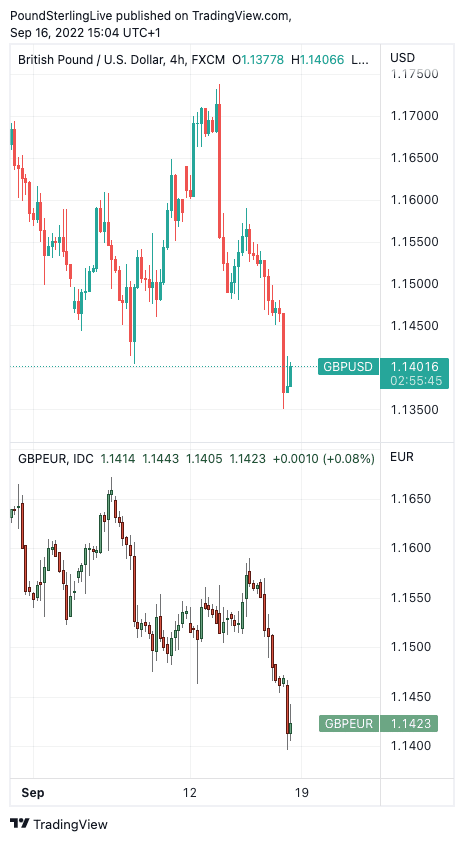

The monetary and fiscal double-header comes after the British Pound slid to its lowest level since 1985 against the Dollar on Friday, while plumbing lows not seen since February 2021 against the Euro.

The Pound's 2022 losses accelerated following the release of disappointing UK retail sales data that left economists warning the economy is already in recession. Retail sales fell 1.6% in the month to August, defying expectations for a shallower -0.5%.

The Pound to Euro exchange rate (GBP/EUR) fell to a low of 1.1399 and the Pound to Dollar exchange rate (GBP/USD) fell to a low of 1.1351.

"The UK pound was slammed to fresh 37-year lows against the greenback after worrisome news on the British consumer moved the economy a big step closer to recession," says Joe Manimbo, Senior Analyst at Convera, formerly Western Union Business Solutions.

"The dismal showing suggested the Bank of England on Sept 22 would raise rates less aggressively than the Fed, potentially opting for a 50 basis point increase to 2.25%," he adds.

Such a decision by the Bank would heap further pain on the Pound, given market expectations are for a 75 basis point hike. A 75bp hike is meanwhile expected from the Fed on Thursday.

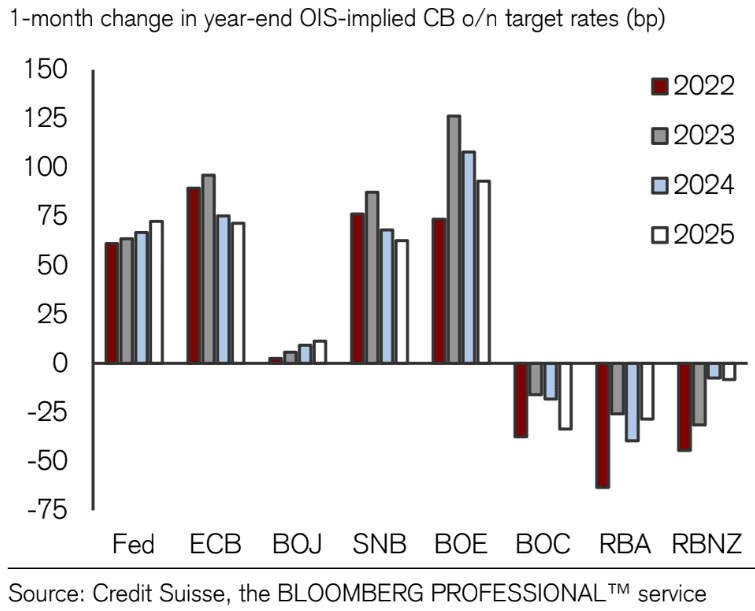

Above: In the past month the market has rapidly raised its expectation of how much further the Bank of England must hike.

The Bank of England has consistently under-delivered against market expectations in the current hiking cycle, allowing the Pound to lose value.

"The elevated fear is that the BOE will again deliver a dovish 50bp hike rather than displaying the inflation fighting mettle being displayed by the Fed, ECB and SNB," says Jonathan Pierce, Credit Suisse's institutional dealing desk.

That central banks that previously held negative interest rates (SNB and ECB) are considered more hawkish than the Bank of England is all readers need to know as to how the UK's central bank has positioned itself.

"Next week's BOE meeting is growing in importance and if they deliver the wrong message GBP will be in significant trouble," says Pierce.

"We expect the Bank of England to hike 50bp on Thursday," says Robert Wood, UK Economist at Bank of America.

"The government's utility price cap cuts peak inflation 450bp, in our view. A lower and earlier prospective inflation peak cuts the risk that the BoE raises the pace again by hiking 75bp in September, in our view," he adds.

Shahab Jalinoos, Head of FX Strategy at Credit Suisse, says the Bank must go with a 100bp if it is to restore credibility and challenge the negative narrative on Sterling.

He says such a move would increase the yield paid on UK assets, thereby attracting the required foreign investor capital required to fund the country's chronic current account deficit.

Above: Four-hour chart showing Sept. performance for GBP/USD (top) and GBP/EUR (bottom). To stay on top of the market set your own free FX rate alert, here.

With deficits in mind, the next major event for the Pound in the coming week is Chancellor Kwasi Kwarteng's mini budget, due Friday.

The Chancellor is expected to present a slimmed-down set of updated forecasts from the Office for Budget Responsibility drawn up in response to the already announced energy bill guarantee.

The effective cap on energy bills will be funded by government borrowing and the final cost will ultimately depend on how gas prices behave over coming months.

Nevertheless, the expectation is the UK government will need to issue more debt than previously anticipated to fund the additional spending, meaning it will most likely have to pay higher debt servicing costs.

"A combination of higher UK yields and lower GBP is not good. Overlay this with renewed focus on the UK current account deficit and it is clear that investors are viewing GBP through the lens of some of its traditional medium-term anchors. We would argue that GBP is effectively the clearest manifestation of a currency where fundamentals matter more than cyclical considerations," says BofA's Wood.