- GBP recovers

- After BoE hikes 25 bp

- And hints at bigger rises ahead

- But some say GBP weakness to return

Image © Bank of England

Increased expectations for a 50 basis point rate hike in August is said by some currency analysts to be one reason why Pound Sterling went higher against the Euro and Dollar in the wake of the Bank of England's June policy update.

The Bank raised interest rates by 25 bp which initially disappointed investors who sold the Pound. But the statement issued by the Bank represented something of a change in approach and was deemed by some corners of the market to be more 'hawkish' and therefore supportive of the Pound.

The Bank dropped guidance that some further gradual rate hikes were needed in the future, saying now that it would respond forcefully if inflation continued to surprise to the upside.

Specifically, the Bank deleted the phrase used at previous meetings that "some degree of further tightening may still be appropriate", replacing it with "the Committee will be particularly alert to indications of more persistent inflationary pressures, and will if necessary act forcefully in response."

This convinced the market to price in more interest rate hikes by the Bank in the future, while also raising expectations for a 50 bp hike in August. "Expectations for higher rates in the future are supportive of the Pound," says a note from international banking services provider Astra Trust.

"You could read that as the MPC shifting from saying that rates will probably rise further to that it now depends on the data. But our take is that it’s more about the MPC becoming more sure that rates will rise further, as well as acknowledging that they may need to rise to a higher level than it previously thought and perhaps in 50bps, rather than 25bps, steps too," says Paul Dales, Chief UK Economist at Capital Economics.

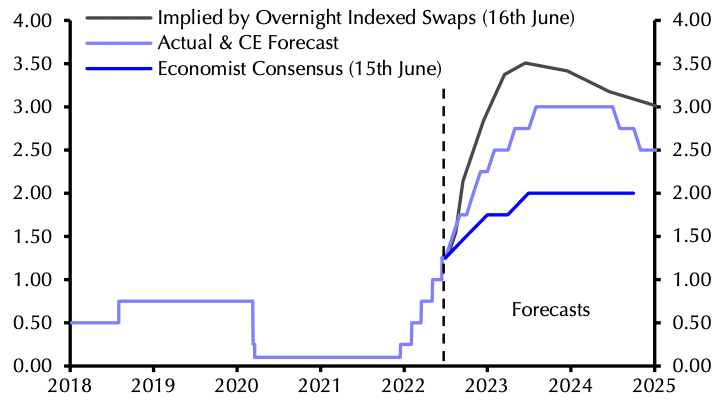

Above: Bank Rate forecasts, showing market implied and economist consensus expectations against those of Capital Economics. Image courtesy of Capital Economics.

Ahead of the decision it was Morgan Stanley's FX strategist in London Wanting Low who was 'on the money' with this call:

"For GBP, specifically, we think the best outcome ... would be a 25bp hike, with clear guidance that the BoE remains data-dependent and stands ready to act if necessary."

"This could either be by an indication of increasing the size of the hike should inflation surprise further to the upside or slowing the pace of hikes should growth roll over and the labour market slacken further," said Low."

He adds the Bank is right to leave the door open to bigger rate hikes while waiting for new forecasts in August, saying it "makes the most sense and would be GBP-positive".

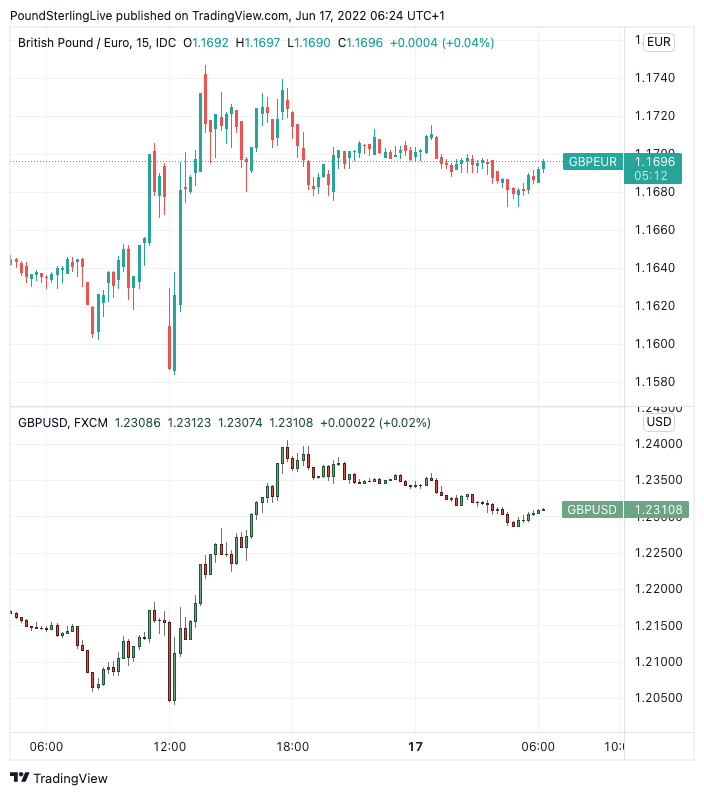

The Pound to Euro exchange rate dropped to as low as 1.1588 in the minutes following the announcement before rising to a high of 1.1747 and subsequently levelling off to quote at 1.1689 at the time of writing. (Set your FX rate alert here).

The Pound to Dollar exchange rate dropped to 1.2040 before peaking at 1.24 and then levelling off to current levels around 1.23.

Some economists were looking for the Bank of England to hike rates by 50 bp in order to be seen to be getting a grip on the inflation narrative.

Such expectations were only exacerbated by the Federal Reserve's decision hours previously to hike by 75 bp.

Others meanwhile argued a Bank of England hike larger than 25 bp would be the correct reaction to the Fed as it would keep a lid on the yield divergence between the U.S. and UK, thereby defending the Pound-Dollar exchange rate.

Protecting the value of Sterling against the Dollar matters in a world where energy is the prime driver of inflationary pressures given commodity markets are priced in dollars.

"It’s pretty clear that the hawks are nervous about the 8% fall in the pound versus the dollar we've seen so far this quarter. Big picture, this is unlikely to change the inflation story dramatically, but the hawks know this is one of the few things the Bank can influence in an environment of rising dollar input prices," says James Smith, Developed Markets Economist at ING Bank.

Above: How GBP reacted to the BoE decision against EUR (top) and USD (bottom).

Morgan Stanley's Low says the market could have perceived a 50bp hike at the June meeting as an over-reaction to other central banks delivering more, which could have exacerbate UK growth concerns.

"Growth expectations remain a key driver of GBP and falling growth expectations would be GBP-negative," says Low.

ING's Smith says ultimately the Bank of England resisted the temptation to follow the Fed and other global central banks into a more aggressive phase of tightening.

"While the hawks failed to win over the rest of the committee, they have succeeded in securing a noticeably more hawkish policy statement," says Smith.

"It speaks of UK core inflation being higher than in the US and Europe, and more importantly signals that it will act forcefully if cost pressures become more persistent," he adds.

ING says a 50bp move is still entirely possible in August.

Above: Money market pricing showing where investors expect UK interest rates to be a year ahead. The data shows a dip and then a rally as the Bank's statement was digested. The move was in turn reflected in GBP/EUR and GBP/USD. Image courtesy of @samueltombs

Paul Dales, Chief UK Economist at Capital Economics, says the Bank of England remains too timid in its approach to monetary policy and will inevitably have to speed up the pace at which it hikes.

"By raising interest rates by 25bps (basis points) today, from 1.00% to 1.25%, rather than by 50bps or the 75bps the Fed announced last night, we think the Bank of England is putting too much weight on the softening economy and not enough on surging inflation," says Dales.

Capital Economics think the Bank will have to raise rates to 3.00%.

While the Bank of England might have ultimately supported the Pound on June 16 the outlook for the UK currency remains challenging.

Jeremy Stretch at CIBC Capital Markets says he remains bearish on Sterling irrespective of the Bank of England.

"The prospect of a weakening macro backdrop, as discretionary spending is being pressured by falling real earnings, continues to point towards the UK entering a recessionary scenario earlier than most other markets, we would expect Q2 and Q3 GDP quarterly GDP to be negative," says Stretch.

"Under such circumstances, we do not anticipate that the BoE will be able to meet implied rate expectations... we remain mindful of Sterling trending back towards 1.2030/40 as the macro backdrop remains challenging" he adds.

CIBC Capital Markets also say Sterling remains inversely risk correlated - i.e. when stock markets fall, so too does the Pound - leaving it at risk in the current equity bear market.

Once the market has repositioned in the wake of the Bank of England update it could be global market conditions that exert their grip on the currency once more.