Image © Adobe Stock

The British Pound went higher in the wake of the Bank of England's decision to raise interest rates again and communicate that further, and potentially larger, rate hikes were coming.

Sterling initially fell against the Euro and Dollar as the news broke and it was revealed the Monetary Policy Committee voted 6-3 for a 25 basis point hike that took Bank Rate to 1.25%.

The falls represent disappointment in a large portion of the market that was expecting a more foreceful 50bp move in light of surging UK inflation and the 75bp move by the Federal Reseve overnight.

But it soon jumped as markets digested the details of the Bank's statement and came to the conclusion this was in fact a 'hawkish' policy update by a central bank that has changed course.

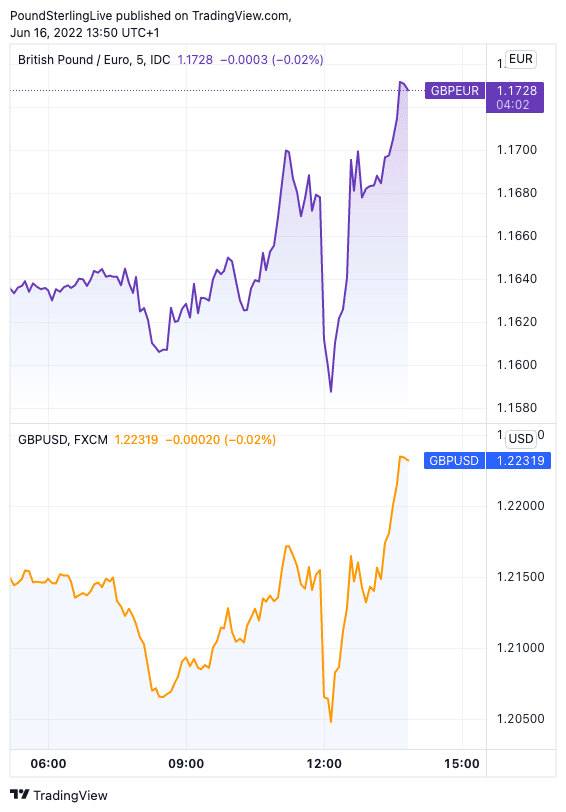

The Pound to Euro exchange rate was down nearly half a percent in the wake of the decision to quote at 1.1589 before pushing up two-thirds of a percent to 1.1724 by the time of this article's update.

The Pound to Dollar exchange rate was down 0.80% at 1.2086 before recovering to 1.2230.

The Bank's statement revealed it is by no means yet ready to quit the hiking cycle, warning it was prepared to act more forcefully in the future if inflation was deemed to be more persistent.

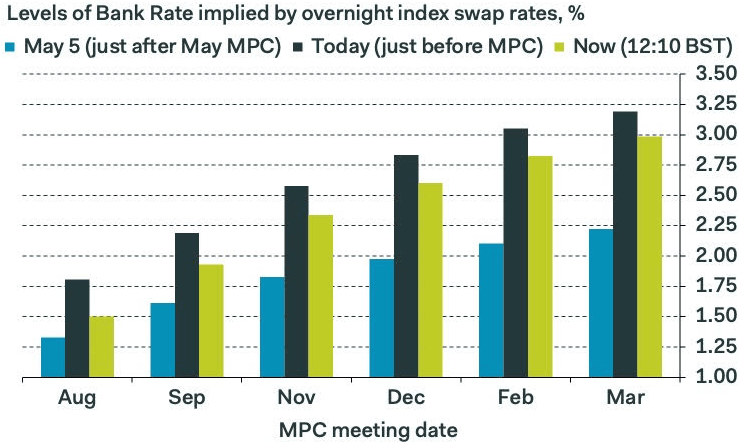

The market promptly began to raise expectations for Bank Rate, which is reflected in the year-ahead OIS curve:

Image courtesy of @samueltombs

The above is in effect the money market's discount for future rates and shows investors initially priced in lower rates a year ahead, only to then reverse the decision and price in higher rates.

This reflects the market's initial disappointment with the scale of the hike and then a subsequent digesting of the contents of the statement that lead to the conclusion more hikes are coming.

The money market's move is meanwhile reflected in the Pound's reaction against the Euro and Dollar:

Above: GBP/EUR (top) and GBP/USD (bottom) in the wake of the BoE rate hike.

"The Committee will be particularly alert to indications of more persistent inflationary pressures, and will if necessary act forcefully in response," read the statement, alluding to a desire to drop guidance and instead react to incoming data.

The Bank dropped the cautious tone evident in previous MPC statements, notably that further "gradual" hikes might be needed. Instead, data would take a guiding role.

"The scale, pace and timing of any further increases in Bank Rate will reflect the Committee’s assessment of the economic outlook and inflationary pressures," said the Bank.

Samuel Tombs, Chief UK Economist at Pantheon Macroeconomics, says this change in tone hints the Monetary Policy Committee (MPC) lacks the unity required to confidently offer guidance on the outlook for interest rates.

As such they will place heavy emphasis on the direction of travel in UK data.

"This suggests that the evolution of wage growth and medium-term inflation expectations, which so far have risen only trivially in response to the surge in CPI inflation over the last six months, will remain key to their decisions," says Tombs.

The Bank also said it was mindful of the Pound's ongoing decline against the Dollar, a nod to the inflationary pressures posed by a falling Pound to Dollar exchange rate which this week fell below 1.20.

The Bank risks becoming stuck in the slow lane when it comes to raising interest rates: last night the Federal Reserve hiked 75 basis points and this morning the Swiss National Bank, which hasn't hiked in years, went 50 bp.

Being left behind could mean the Pound struggles against the currencies of more agressive central banks, most notably the Fed, and in a world struggling under the weight of surging energy costs such an outcome would only serve to press imported inflation higher.

But the change in tone in the statement suggests the Bank is open to more forceful hikes and a higher 'terminal' rate than they might have been prepared to deliver just last month.

This explains the move higher in interest rate expectations and the Pound.

"We think the Bank of England is putting too much weight on the softening economy and not enough on surging inflation. It did hint it may yet raise rates faster. But either way, we think the Bank will have to raise rates to a peak of 3.00%. That’s a little lower than the peak of 3.50% now priced into the markets, but higher than the peak of 2.00% expected by most analysts," says Paul Dales, Chief UK Economist at Capital Economics.

Pantheon Macroeconomics acknowledges the Bank cannot fall too far behind the Federal Reserve in order to defend the GBP/USD exchange rate and keep a lid on imported inflationary pressures.

They have therefore raised their Bank Rate forecast by 25 basis points and now look for an additional 25bp rate hike after the further 25bp increase they expect in August.

This would leave Bank Rate peaking at 1.75% in this cycle.

Image courtesy of Pantheon Macroeconomics.

"While the Bank has further increased rates, it has done so with considerably less gusto than the Fed which last night announced a 75bps hike – making the Bank’s 25bps increase look rather lacklustre in comparison," says Hinesh Patel, portfolio manager at Quilter Investors.

The Bank of England remains concerned that UK economic growth will slow sharply over coming months, confirming this to be a central bank concerned as much with economic growth as it is with inflation.

But their sole stated mandate is to keep a lid on inflation, which suggests the Bank could have been more agressive. Indeed the Bank said inflation could now top 11% later in the year as it delivered its latest assessment.

"As was widely expected, today the Bank chose to maintain its course at 25bps, marking the fifth consecutive rate rise since the BoE first began its campaign against inflation, but signalled a larger move may be on the horizon. We expect this will be needed to try and stabilise UK sterling at the very least given the larger hikes in the US," says Patel.

Zeeshan Syed, economic expert from the University of Salford Business School, said much more may be needed from the Bank in future.

"BoE rate is still among the lowest in its history; other than during the post-financial crisis period, the current rate only existed during the second world war. Raising the rate is the only way forward, as the ex-governor, Mervyn King, notes that BoE's inaction has already paved the way for fiscal mismanagement," says Syed.

He adds the increase of 25bp may not be enough as much of the current inflation the UK is witnessing is due to consumption; "people are consuming, spending, and borrowing as if there is no tomorrow. That is causing an upward inflation spiral".

Syed says data suggests that out of 9.5% of inflation, 5.5% is contributed by goods and services consumption.

"The threat is that the trend may balloon as EY predicts that consumer borrowing will increase to 7.9% this year, a five-year high," he adds. "In this context, BoE is duty-bound to curtail this buy now pay later culture and inhibit the widespread and un-accounted for consumption. The more the bank increases the rate beyond expectations (above 0.50bp), the more quickly this irrational exuberance will end, and fiscal sanity will prevail."