- GBP/EUR & GBP/CHF can go further says Goldmans

- GBP/USD under near term pressure

- But USD to still fall in 2021 says UBS

Image © Adobe Images

- Market rates at publication: GBP/EUR: 1.1613 | GBP/USD: 1.3814

- Bank transfer rates: 1.1388 | 1.3527

- Specialist transfer rates: 1.1532 | 1.3717

- More about bank-beating exchange rates, here

- Set an exchange rate alert, here

The British Pound is tipped to maintain a trend of appreciation against then Euro and Swiss franc, according to Goldman Sachs.

The Wall Street investment bank tells clients at the start of the new week that they remain buyers of Sterling on the view that the UK economy is well poised for an economic rebound over coming weeks and months, with the March budget announcement proving supportive of this view.

UK Chancellor Rishi Sunak last week unveiled the UK government's spending and taxation plans and surprised economists by providing more generous near-term support packages.

"The UK economy is well-positioned for the coming recovery," says Zach Pandl, economist at Goldman Sachs. "The support program laid out by the government surprised consensus expectations to the upside, and included a number of economic incentives aimed at medium-term investment."

The Pound-to-Euro exchange rate last week rallied back above 1.16 in the wake of the budget announcement and the pair is at 1.1612 at the start of the new week.

The Pound-to-Dollar exchange rate has however come under near-term pressure as a broad-based rally in the U.S. Dollar continues to dominate foreign exchange market action. The pair is at 1.3822 at the start of the new week. (Read: Budget 2021 a 'Win Win' for Pound Sterling, Advances v Euro and Dollar).

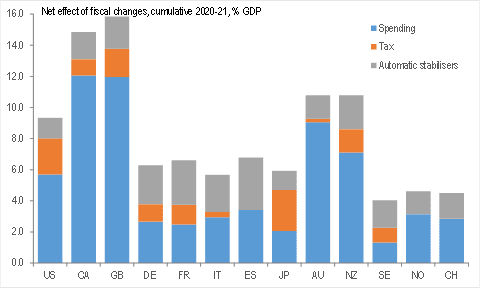

Sunak announced a net giveaway for the short-term that will see an additional £65BN in spending, grants and tax breaks made available, meaning the total additional spending and benefits made available during the crisis stands at £352BN.

For Adam Cole, Chief Currency Strategist at RBC Capital Markets, this is a significant development as it makes the UK the biggest easer amongst the world's advanced economies.

"UK Budget delivered another extraordinary dose of near-term fiscal easing. Net changes in 2020-21 are worth over 2.5% of GDP and future fiscal tightening only starts in 2023 and is moderate in the early years," says Cole.

Above: UK and Canada have eased by most, European countries by least, image by RBC Capital.

Most economists we follow say that providing generous support to economies during the covid crisis is likely to reduce any long-term scarring and allow for a more robust rebound.

For currencies, generous fiscal support in the near-term is therefore a supportive impulse.

Goldman Sachs analysis shows the additional spending announced by the government comes after substantial fiscal support in 2020 already contributed to UK households accumulating "excess savings" of nearly 10% of their pre-pandemic annual spending.

They say this puts the UK just behind the U.S. "and quite a bit more than in the Euro area".

"Solid household and business balance sheets should soon translate into robust growth, as the UK’s strategy of prioritising getting more people vaccinated with a single dose appears to be paying dividends. We are therefore keeping open the short EUR/GBP component of our long GBP/CHF cross trade," says Pandl.

Goldman Sachs tell clients the main risk to this trade is a further broad tightening of financial conditions globally.

{wbamp-hide start}{wbamp-hide end}{wbamp-show start}{wbamp-show end}

Global markets have struggled under the weight of rising sovereign bond yields of late, in particular the rise of longer-dated bond yields.

This has tightened the cost of finance in the global economy and investors are concerned the development will stifle the global economic recovery, before it has even had a chance to get started.

As a result stock markets have lost value since late February, as have those currencies that are positively aligned with market sentiment.

The biggest winner of 2020 - the Australian Dollar - has been particularly hard-hit given the positive correlation between the currency and global market sentiment.

Pound Sterling has also however shown a strong correlation with global market sentiment, particularly against the Dollar.

Therefore, should global bond yields continue to rise and stock markets struggle, the GBP/USD exchange rate will likely remain under pressure.

"Rising US yields have added to equity market volatility and supported the US dollar. The Federal Reserve remains dovish, but chair Jerome Powell chose not to push back verbally against higher yields providing a further short-term boost to the greenback," says Mark Haefele, Chief Investment Officer Global Wealth Management, UBS AG.

However, foreign exchange strategists at UBS say on Monday they are not expecting the Dollar to appreciate substantially.

"Currencies move in cycles, and political, economic, and historical trends point to further medium-term USD weakness," says Haefele.

The analyst says fiscal and monetary stimulus are bad for the U.S. Dollar while the Eurozone’s relative performance looks set to improve.

In addition, the U.S. Dollar has historically weakened when longer-term yields rise says Haefele. "So the USD has more room to fall this year, with the pickup in the cyclical recovery likely to boost pro-risk and commodity-linked currencies."