- Market rates at publication: GBP/EUR: 1.1578 | GBP/USD: 1.3930

- Bank transfer rates: 1.1354 | 1.3640

- Specialist transfer rates: 1.1490 | 1.3830

- More about bank-beating exchange rates, here

- Set an exchange rate alert, here

The British Pound went higher against the world's major currencies following the announcement of the UK government's spending and tax plans on Wednesday, with economists saying the measures are likely to boost the economic recovery.

UK Chancellor Rishi Sunak announced a net giveaway for the short-term that will see an additional £65BN in spending, grants and tax breaks made available, meaning the total additional spending and benefits made available during the crisis stands at £352BN.

Sterling was broadly firmer following the developments, with many economists saying the decisions were relatively well balanced given the circumstances the economy finds itself in.

For Adam Cole, Chief Currency Strategist at RBC Capital Markets, this is a significant development as it makes the UK the biggest easer amongst the world's advanced economies.

"Yesterday's UK Budget delivered another extraordinary dose of near-term fiscal easing. Net changes in 2020-21 are worth over 2.5% of GDP and future fiscal tightening only starts in 2023 and is moderate in the early years," says Cole.

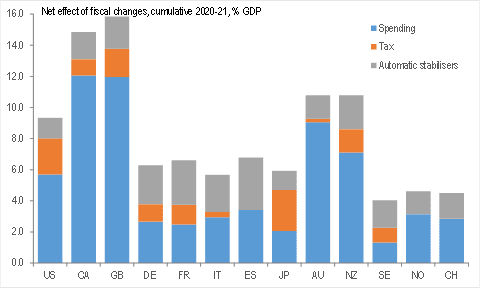

Above: UK and Canada have eased by most, European countries by least, image by RBC Capital.

"On our estimates, the UK has now delivered more fiscal easing than any other G10 country. Yesterday’s mix of tax cuts and spending increases take our estimate of total stimulus through 2020 and 2021 to 14% of GDP," says Cole.

RBC Capital note Canada is not far behind the UK (13% of GDP), followed by Australia and NZ (both around 9%).

"The US is falling behind the Commonwealth countries, but this will change when we know how to allocate the latest stimulus package. Similarly, allocation of the ERF will partly close the gap for European countries, but won’t change Europe’s status as a fiscal laggard in its COVID response," says Cole.

For foreign exchange markets, this easing is significant in that it suggests the economy will be able to recover in a strong fashion once restrictions are lifted.

A stronger economy relative to those economies that are potentially lagging meanwhile bestows an element of outperformance on the Pound.

"So far, FX markets have focused on the positive cyclical impact of more easing in the UK and the Budget has added to the support from the UK’s relative success in rolling out COVID vaccines," says Cole.

The boost to spending announced by the Chancellor means the UK's borrowing needs will be higher than previously expected, and the UK's independent Office for Budget Responsibility (OBR) forecast the 2021/22 budget deficit will be at £234BN, against the November forecast of £164.2BN, this is a 2021/22 deficit of 10.3% of GDP vs. the November forecast for 7.4% of GDP.

OBR forecasts show 2022/23 budget deficit of 4.5% of GDP, against the November forecast 4.4% of GDP.

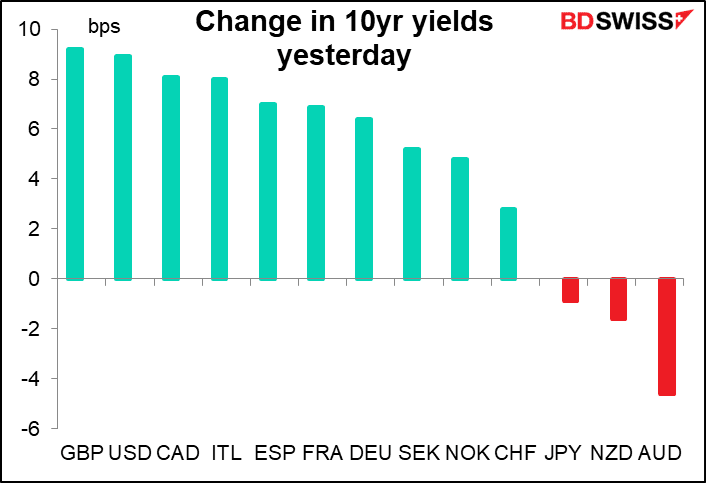

As a result of the increased borrowing projections bond markets ask for a higher return for holding UK debt, leading to higher UK bond yields.

"Yields in most of the major bond markets were higher yesterday, led by Britain after Chancellor Sunak announced an expansionary budget," says Marshall Gittler, Head of Investment Research at BDSwiss Holding Ltd.

"The increase in borrowing pushed up gilts yields and supported the pound," says Gittler.

"Nonetheless, I think cable’s inability to regain the 1.40 level after this better-than-expected news is worrisome. If this can’t push it back above 1.40, what will? The economic indicators are still surprising on the upside, but less and less," he adds.

Francesco Pesole, foreign exchange strategist at ING Bank says yesterday’s UK budget was seen to strike the right balance and support the spring recovery.

"Gilts sold off on the larger than expected supply plans, yet we think the re-assessment of UK growth prospects can support GBP," says Pesole.

The short-term nature of the boost might be positive, but the longer-term implications are hazier.

"Longer-term, however, sharp rises in borrowing forecasts need to be seen in the context of the UK’s already large imbalances and relative scarcity of domestic private savings. Whilst we won’t fight the positive short-term impact, longer-term the further blowout in borrowing is at best ambiguous," says Cole.

{wbamp-hide start}{wbamp-hide end}{wbamp-show start}{wbamp-show end}