- EUR/USD is recovering but it won't last suggest analysts at Nordea

- Dollar to benefit amidst strengthening domestic inflation

- Stronger Dollar likely on Trump fiscal policy

© Andrey Popov, Adobe Stock

The Euro has strengthened by 0.3% versus the Dollar at the start of the new week having traded back towards 1.1987 on the interbank market, having achieved a 2018 low at 1.1822 in the previous week.

The single currency's recovery is partly due to Dollar bulls having the wind taken out of their sales by lower-than-expected US inflation data which showed a 2.3% rise compared to a year ago, versus the 2.4% expected.

Lower inflation makes it less likely the US Federal Reserve (Fed) will put up interest rates as quickly as the market was expecting and this is negative for the Dollar because higher interest rates - or the expectation of higher interest rates - tends to strengthen the Dollar by attracting greater inflows of foreign capital drawn by the promise of higher returns.

Since the disappointing inflation release, however, things have looked a lot less rosy for the Dollar and some analysts are even hailing this as a sign that the Dollar uptrend has reached an end.

Taking a contrarian standpoint are strategists at Scandanavia's Nordea Markets who still think EUR/USD will go lower, and are keeping their bearish bets against the Euro open.

They continue to see the potential for the exchange rate to fall to an initial target at 1.1850, if not all the way down to parity eventually.

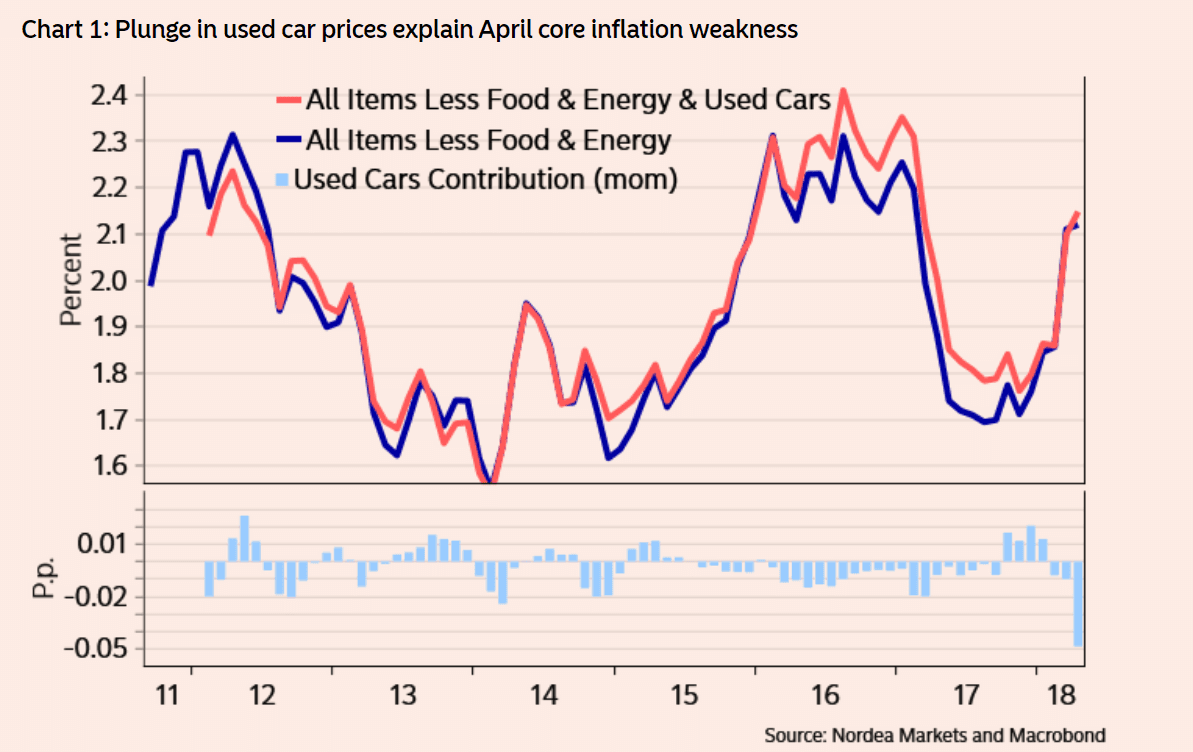

Their continued faith in the Dollar is due to a belief that the April's poor core CPI figure was not indicative of lower inflation to come, and also that inflation in the Eurozone will slow down more than in the US, hitting the Euro relatively more than the US Dollar.

"We still judge that the inflation spread between the US and the Euro area is bound to widen more over the next months. This is one of the reasons why we stick to our short EUR/USD," says Martin Enlund, chief analyst at Nordea Markets.

Enlund dismisses the slowdown in US inflation data in April as a one-off, putting it down to a mis-perception based on the surge in prices due to the hurricane-effect last year. Since then prices have looked worse than they really are because they have been "mean-reverting" from a spike high.

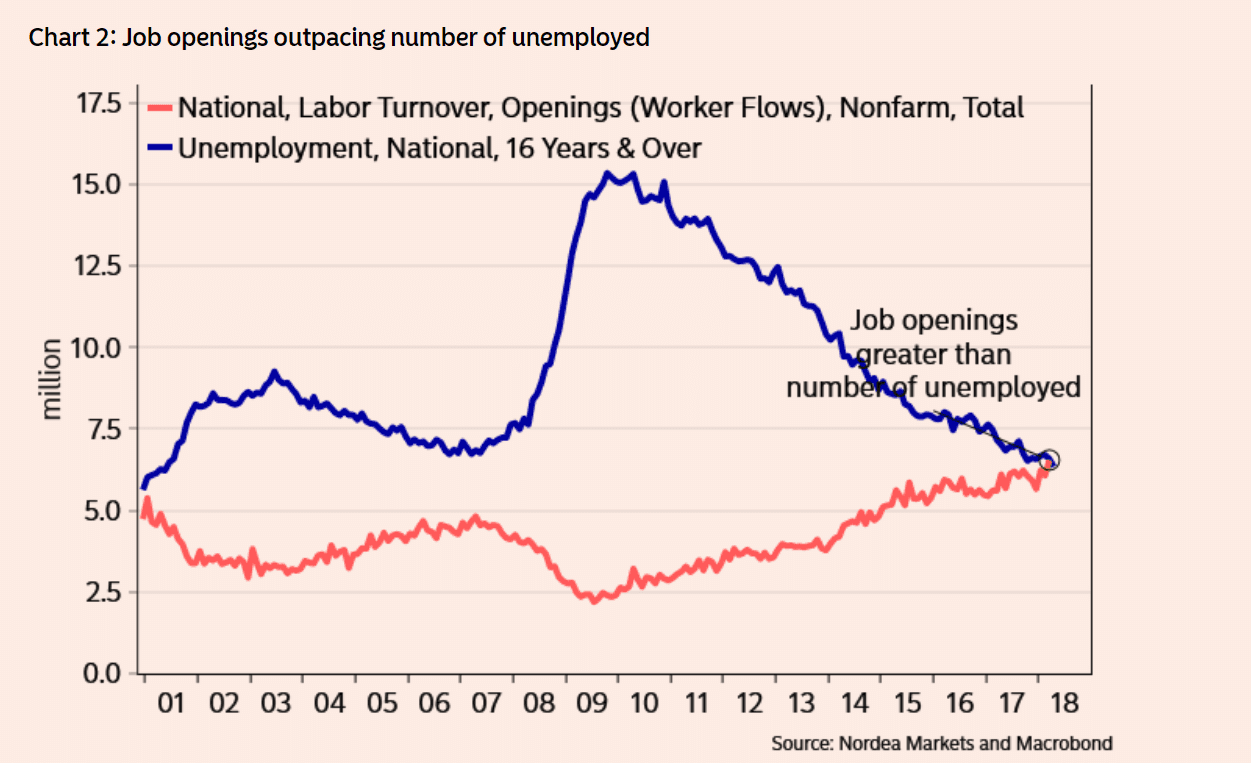

If anything, US inflation is more likely to rise than fall in coming months due to a combination of rising petrol prices and an improving labour market.

"The number of job openings is now outstripping the number of people unemployed. This is a critical juncture for the Fed," says Enlund.

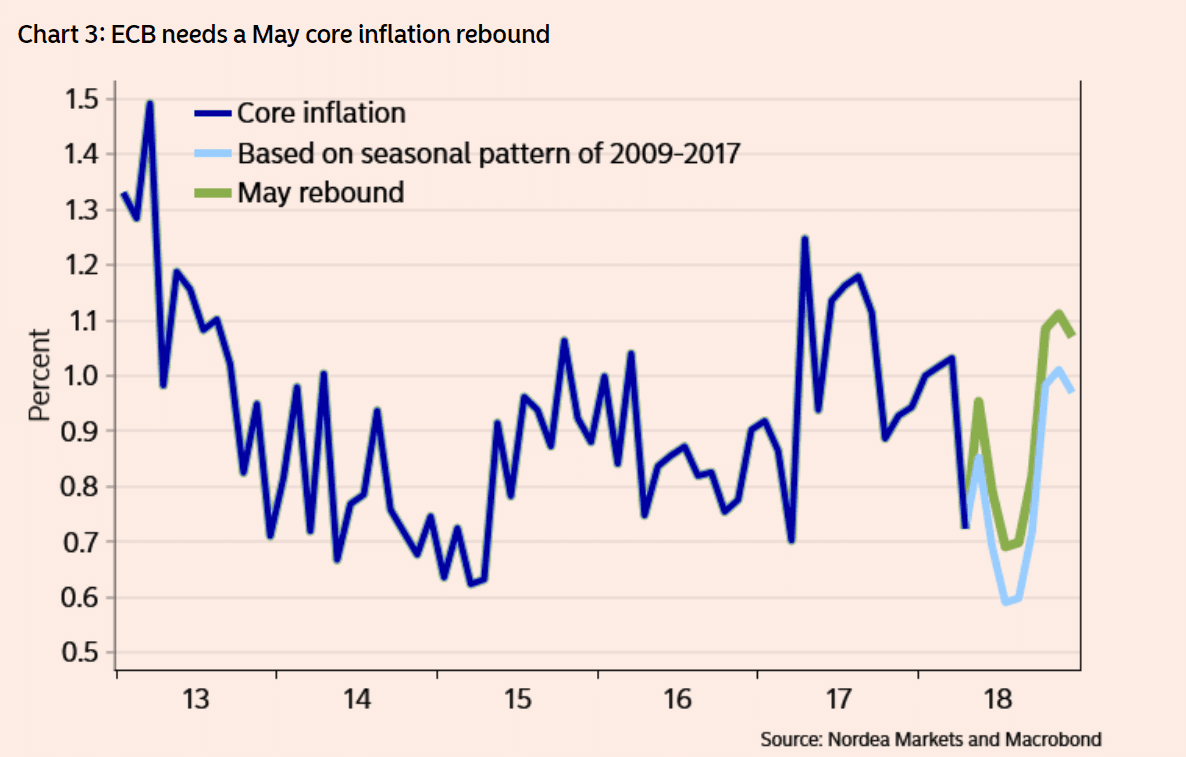

The European Central Bank (ECB) and economists remain quite optimistic about the level of inflation in the Eurozone expected in May but based on seasonality in prior years, inflation in Europe is actually more likely to slow down than rise.

"If the May number only reproduces the usual pattern of 2009-2017, then ECB will need to cut its core inflation forecast again," says Enlund.

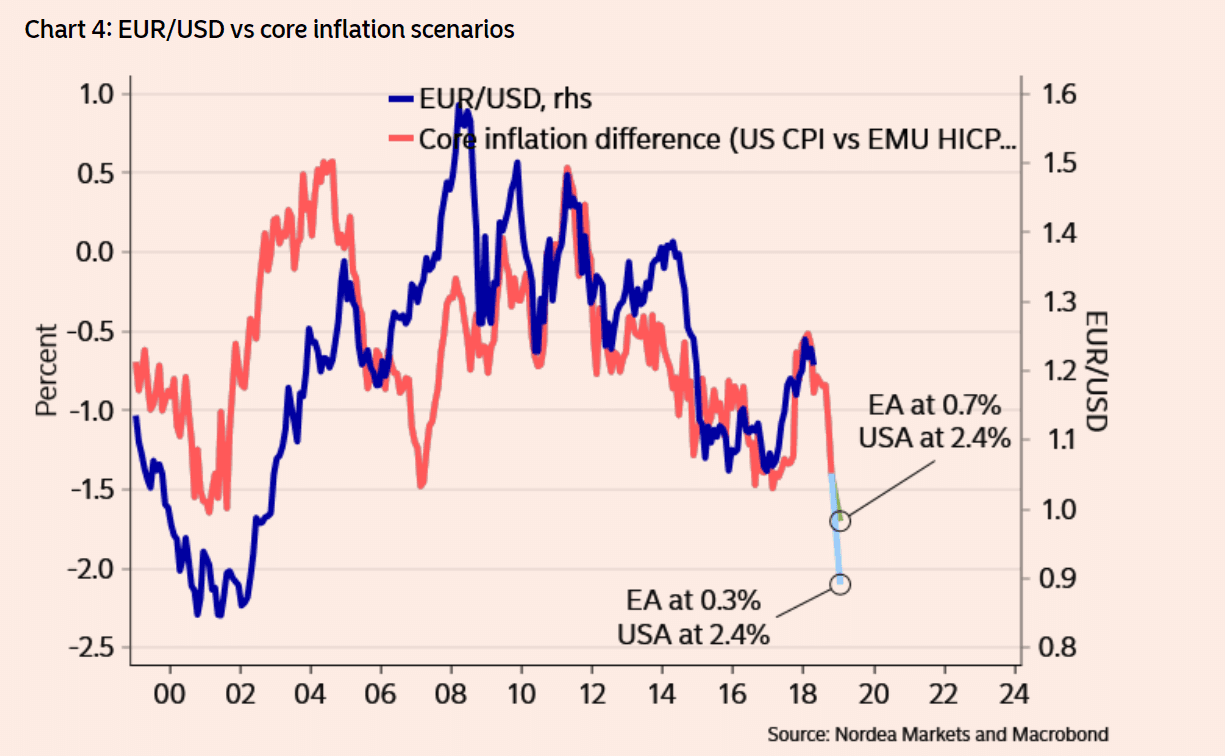

The difference or 'spread' between US and Eurozone core inflation is actually quite a good indicator of where the EUR/USD exchange rate is likely to go and Nordea's Enlund expects it to widen to record levels later in the year.

Our reading of the above model suggests that EUR/USD could actually fall to parity, or even lower, should inflation dynamics and the currency market extend their correlations.

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.

Fiscal Policy Another Potential Driver of Dollar Strength

It had been feared the Trump administration might put the Fed under pressure to adopt a weaker Dollar policy in order to oil the wheels of its export-orientated 'America First' agenda.

One way of achieving such an outcome might be to pressure the Fed to slow down its programme of interest rate hikes, however, according to Enlund, this does not appear to be the case, since a recent 'hawkish' speech by Fed chairman Powell and the appointment of the marginally hawkish new member Clarida to as vice chairman evidence the contrary.

"The hawkish rhetoric in Fed Chair Powell's speech on global capital flows, as well as the nomination of Clarida to the FOMC, puts two final nails in this coffin, however," says Enlund.

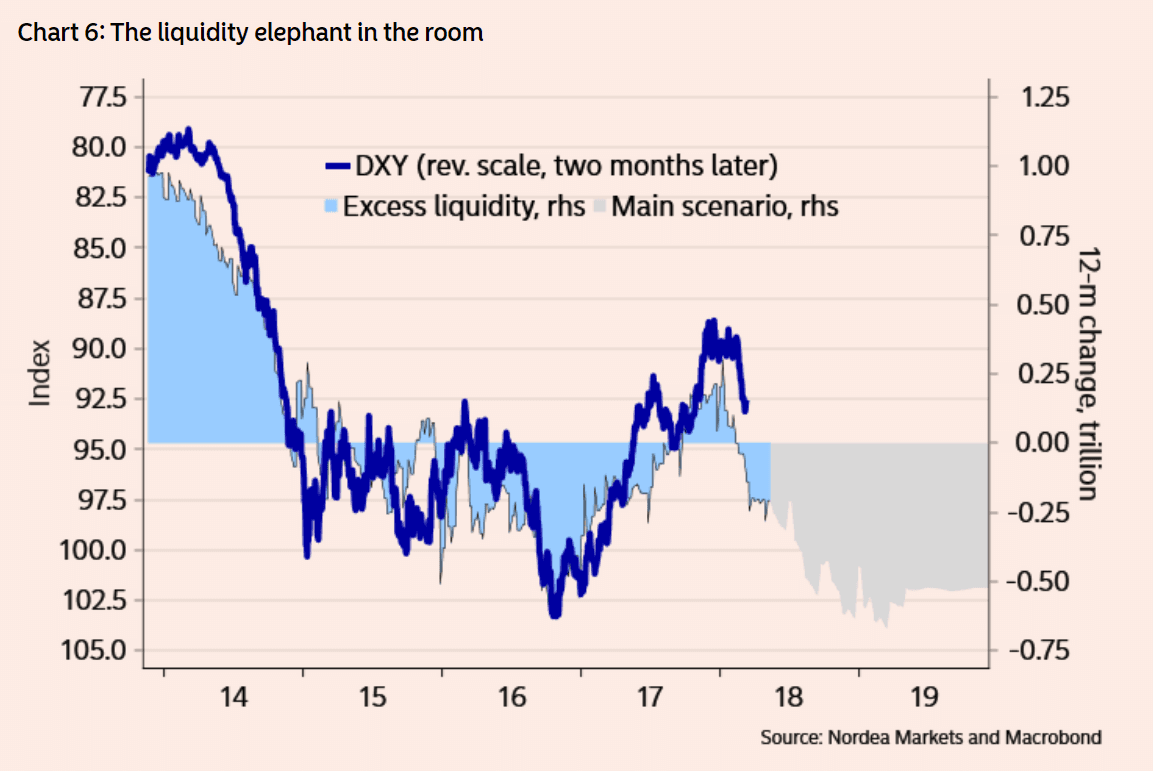

USD could also continue rising due to Dollar scarcity as the US Treasury has to hoover up excess Dollar liquidity to maintain its capital buffer (which it keeps at 300bn for emergencies). The maintenance of the buffer has become increasingly difficult recently after government tax cuts reduced the Treasury's revenue, and this has exacerbated USD shortages.

As can be seen from the chart below the level of excess Dollar liquidity is highly correlated with the value of the Dollar Index (the Dollar versus a trade-weighted basket of currency counterparts).

Yet the whole story is not USD-positive, and there are some factors previously supportive of the Dollar which have since been fading.

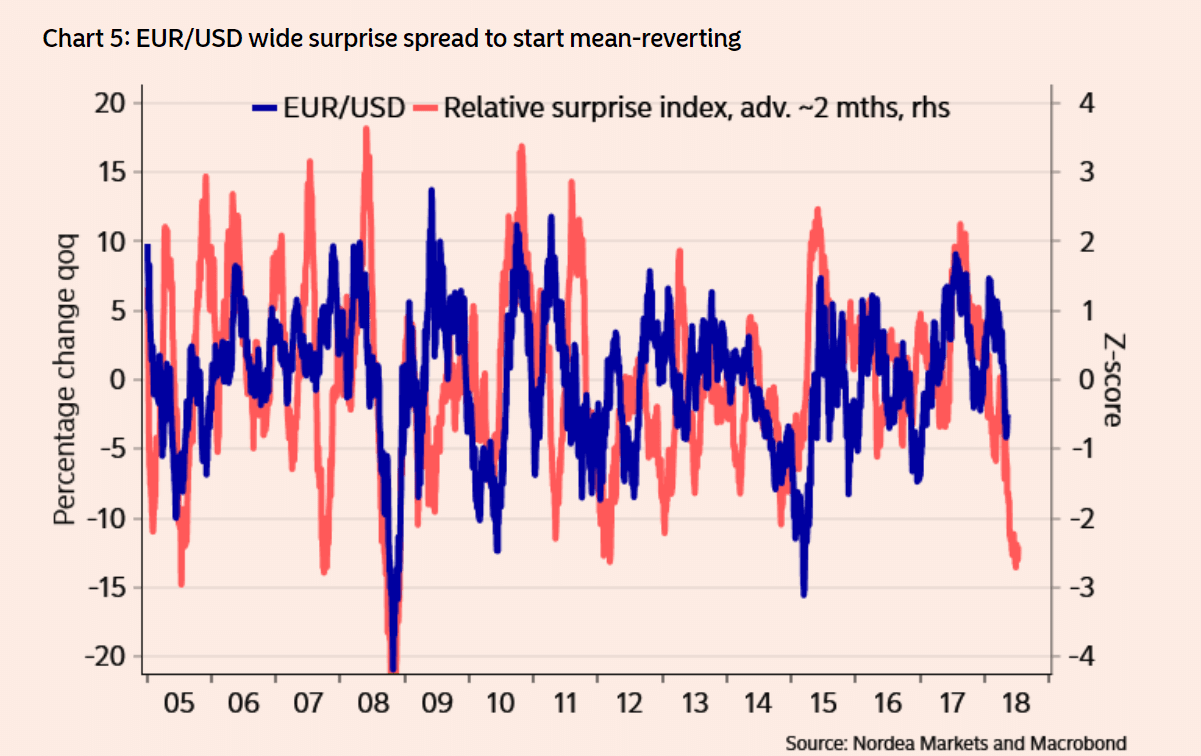

The difference between data surprises in the Eurozone and the US, for example, has reached an over-stretched extreme which recommends a 'reversion to mean' favouring an improvement of Eurozone data over US data, which would be positive for EUR/USD.

"Some dollar positives should, however, be fading. The difference between EA data and US data hasn't been this wide since early 2012, and a rebound in the EA surprise index might moderate the upside in the dollar," adds Enlund.

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.