The euro exchange rate complex has started the new year in robust fashion but forces should ultimately take EURUSD to parity says a new report.

Forecasts from Skandinaviska Enskilda Banken (S.E.B) - the Swedish Financial Group - confirm a delay to when parity in the euro to dollar conversion will be reached in 2016.

In a note to clients analysts say that while the euro is still forecast to decline in 2016 the rate of decline will be slower.

The suggestion comes at a time when we are witnessing the euro to dollar conversion trade within a well-defined sideways range ensuring any attempts at USD strength are ultimately contained.

Analysts note that improving Eurozone economic fundamentals coupled with stagnant US bond yields are allowing the euro to remain better supported.

Recent data releases provided confirmation of the ongoing cyclical recovery in the euro area. Real GDP had continued to grow in the third quarter, while other incoming information, including the latest survey evidence available up to November 2015, remained consistent with a continued moderate economic recovery.

And most importantly the governing members at the European Central Bank believe the policy measures they have put in place are working:

“The recovery, although modest but still with growth rates above potential, remained intact,” read the account of the last meeting held by the Governing Council at the ECB which markets have read as a suggestion that no euro-negative actions will be taken for some time yet.

Latest Pound/Euro Exchange Rates

| Live: 1.174▲ + 0.08%12 Month Best:1.1752 |

*Your Bank's Retail Rate

| 1.1341 - 1.1388 |

**Independent Specialist | 1.1576 - 1.1623 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Euro Benefits from the 2016 Market Sell-Off

Another key reasons why the euro exchange rate complex could do well over coming weeks relates to the nerves dominating global financial markets.

2016 has gotten off to a poor start for share holders who are exposed to the jitters emanating from China.

One would think the US dollar - the global reserve currency and perceived safe haven - would be best placed to take advantage of such negative market conditions.

Not necessarily says Richard Falkenhall at S.E.B:

“Historically we have become used to seeing the dollar benefit from falling risk appetite. However, as we highlighted following the period of increased financial stress when China devalued the yuan last August, the dollar no longer serves as the natural safe haven currency during periods of rising uncertainty. Instead the euro and the Japanese yen appear to benefit from increased stress in global financial markets.”

S.E.B observe that recently the euro has gained against the dollar (and pound sterling for that matter) when stress in financial markets increases.

“If the uncertainty surrounding Chinese growth and the present negative equity market development continue going forward, it could clearly reinforce the negative dollar trend in line with historical experience following Fed liftoffs, albeit for a different reason,” says Falkenhall.

As research from RBS notes, there is good reason to expect the Chinese theme to continue in 2016. In fact, we could well be at the beginning of the Chinese Yuan devaluation cycle as it is argued the currency is overvalued to the tune of 20%.

What we are seeing here is another reason to be more positive regarding the euro’s chances in 2016.

US Dollar Strength Delayed

The other side of the EURUSD equation matters too - can the US dollar find upside and push the EURUSD lower?

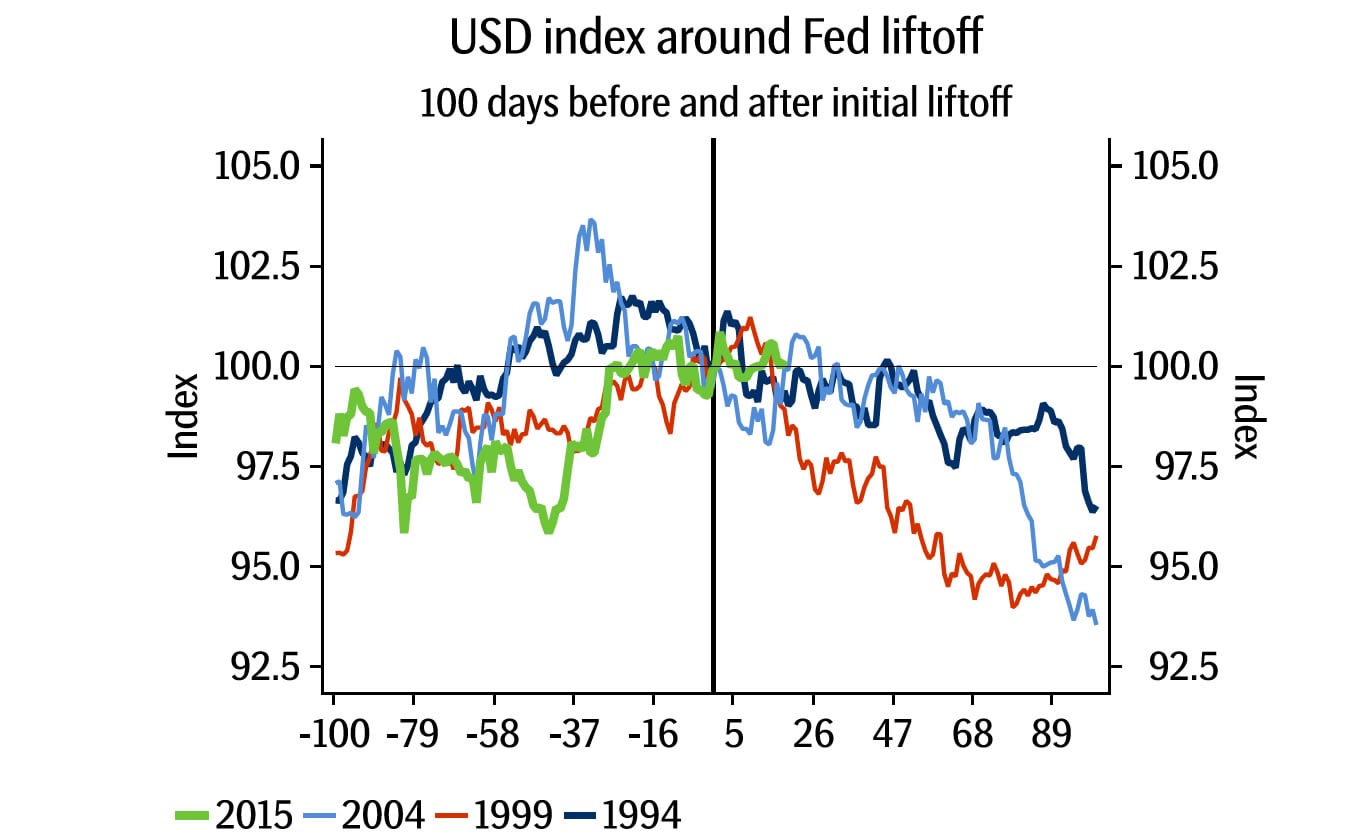

History shows that the US dollar rises and then tends to fall after the US Federal starts raising rates.

So far history has repeated itself - the US dollar appreciated slightly against the euro - and across the board for that matter - since the decision to raise rates in December.

“Although there are reasons suggesting the post-liftoff dollar reaction could be different this time, which are also supported by its trading performance since the rate decision in December, downside risks to the near-term dollar outlook still persist,” says Falkenhall.

If history is to repeat itself then we could be witnessing peak-dollar.

Parity Ahead, S.E.B Still Constructive on the US Dollar in 2016

Nevertheless, the global theme at S.E.B remains pro-USD.

“We are still constructive on the outlook for the dollar although we maintain a cautious near-term view due to financial market uncertainty. While we expect the Fed to proceed very cautiously to tighten monetary policy this year, its approach will remain the complete opposite tothat taken by the ECB.

Enter that familiar theme of monetary divergence - the bottom line, all being equal - is that the ECB continues to grow the amount of money it supplies to the Eurozone economy while the US Federal Reserve is looking to cut the supply.

Importantly S.E.B believe the pace of divergence will continue to increase, “which should be dollar supportive.”

Previously S.E.B forecast the euro to dollar rate to reach parity by mid-2016. “We still expect parity to be achieved but later when the EUR/USD bottoms at 1.00 by the end of Q3 this year.”

So those hoping for sub—1.0 may be disappointed if S.E.B are on the money.