Image © Adobe Images

The euro’s surge against the dollar last week was driven less by shifting macro fundamentals and more by an options-led liquidity dislocation that briefly turned market mechanics against participants.

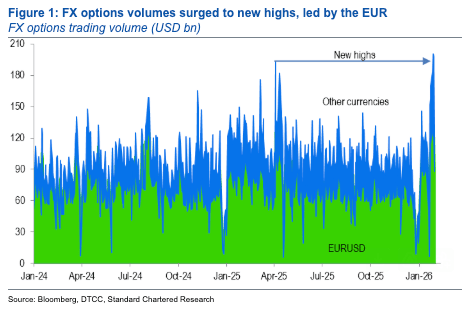

According to Standard Chartered, the selloff in the dollar extended well beyond spot trading and was amplified by positioning in the derivatives market as EUR/USD accelerated through key technical levels.

“Last week’s dollar sell-off was not just a spot story; it was an options-led dislocation that briefly turned liquidity against the market, in our view,” says Bader Al Sarraf, Research Analyst at Standard Chartered.

His research points to the break above widely watched topside levels, most notably around 1.20, as the catalyst that forced a rapid unwind of barrier-linked option structures.

"As EUR-USD accelerated through widely watched topside levels - most notably around 1.20 - we think a large stock of barrier-linked structures were forced to unwind,” says Al Sarraf.

The resulting adjustment was visible in volatility and turnover, with one-month implied volatility jumping by around three volatility points in a single day, while total EUR/USD options turnover rose by roughly 55%.

“1M EUR-USD implied volatility jumped around 3 vols over a day, while total EUR-USD options turnover rose by roughly 55% - we think this reflected both forced repositioning and defensive demand," he explains. "This is despite the underlying macro narratives remaining largely unchanged."

Image courtesy of Standard Chartered.

Consensus projections for the next four quarters, compiled from leading investment banks.

Access the full forecast →

The research finds that while EUR/USD was range-bound between 1.15 and 1.18, a range of options structures had been established to monetise carry in a low-volatility environment.

But once spot moved decisively higher, those structures were triggered, leaving dealers over-hedged and forcing them to chase the market higher.

“Dealers, who had hedged those structures via topside options, were likely left over-hedged, forcing them to chase spot and buy back hedges at progressively worse levels," says Al Sarraf.

He says the scramble to rebalance positions became self-reinforcing, contributing to the sharp spike in front-end volatility.

“As the dust settled, the options market began to normalise, but it did not fully reset,” he adds. "Fresh supply likely emerged at higher topside strikes as markets re-entered barrier structures further out, helping to cap skew and pull implied vol off its extremes."