© European Central Bank

- EUR treads water amid Draghi's final ECB press conference.

- Draghi tipped to depart on plea to governments for stimulus.

- Amid divisions in Frankfurt over rates and quantitative easing.

- Departs with Germany likely in recession, Eurozone on rocks.

- Federal Reserve rate decision on Oct 30 key to EUR outlook.

The Euro was buoyant Thursday amid Mario Draghi's final press conference on behalf of the European Central Bank (ECB), which comes amid divisions in Frankfurt over recent decisions and as rate setters grapple with an ongoing economic slowdown, but the downside is tipped to prevail in the weeks ahead.

Europe's three main interest rates were left unchanged in October, with the deposit rate held at its new low of -0.50% while rates on 'main refinancing operations' and the 'marginal lending' facility remained unchanged at 0% and 0.25% respectively. The ECB also confirmed it will push ahead with the reopening of its quantitative easing program from November 01, which will see it buy €20 bn of bonds per month for an open-ended period of time.

Mario Draghi, who exits the ECB this month and will be replaced by former International Monetary Fund boss Christine Lagarde, said the Eurozone has been cheered by the recent ebbing of 'no deal' Brexit risk but noted that the UK's pending EU exit, as well as international trade tensions, remain a risk to the outlook. Nonetheless, Draghi also claimed to have achieved the bank's September objectives.

"Draghi has been the most closely watched person in global finance, to the extent that traders speculate about ECB policy based on what colour of tie he wears," says Florian Hense at Berenberg. "Although the Dragh-era is set to end, the era of low rates and the ECB acting as the Eurozone’s financial backstop continues. During his presidency the ECB has transformed itself in a major way. Previously unconventional policy measures have become part of the ECB’s standard toolkit. This is Draghi’s legacy."

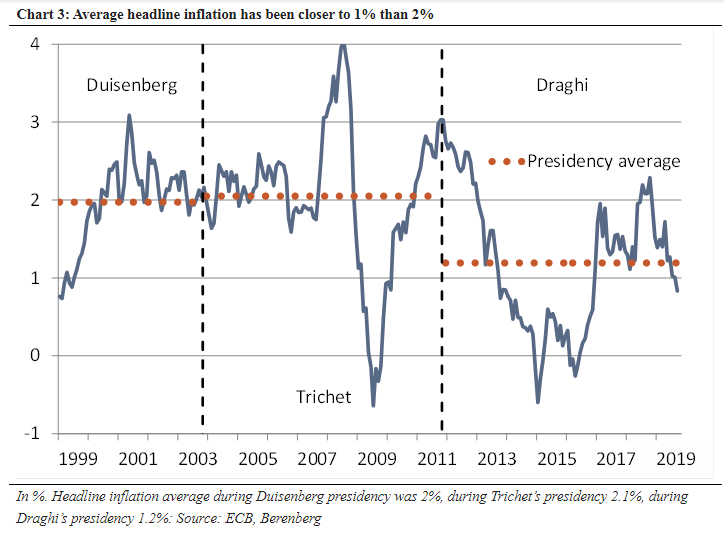

Above: Eurozone consumer price index inflation rates under former and current ECB regimes. Source: Berenberg.

The outgoing policy chief said in September the bank wants to "anchor" expectations for interest rates in the future at or below present levels until such time as the inflation outlook becomes consistent with an eventual attainment of the target. That has largely been achieved because pricing in the overnight-index-swap market implies the ECB's main refinancing rate will fall and remain below the current level until at least the second half of 2021, although inflation expectations have since fallen further.

September's decisions have been credited with causing an almost unprecedented level of division in the corridors of the ECB given the limited benefit that was obtained from the prior program, which saw the bank's balance sheet swell to €2.6 trillion in the three years to the end of 2018, and the unknown costs of the program. German policymakers have long opposed QE although opposition to it has recently broadened out to other countries too.

"For many, especially those in the financial services industry, the first half of Mario’s term was a big success. However, the second half of his tenure will most likely be remembered as a string of failed attempts to reflate the Eurozone," says Artur Baluszynski, head of research at Henderson Rowe. "There are many external deflationary forces outside of the ECB’s control. The sooner the EZ’s political elite, especially in Germany, accept this fact, the better chance there is for a real recovery for the bloc."

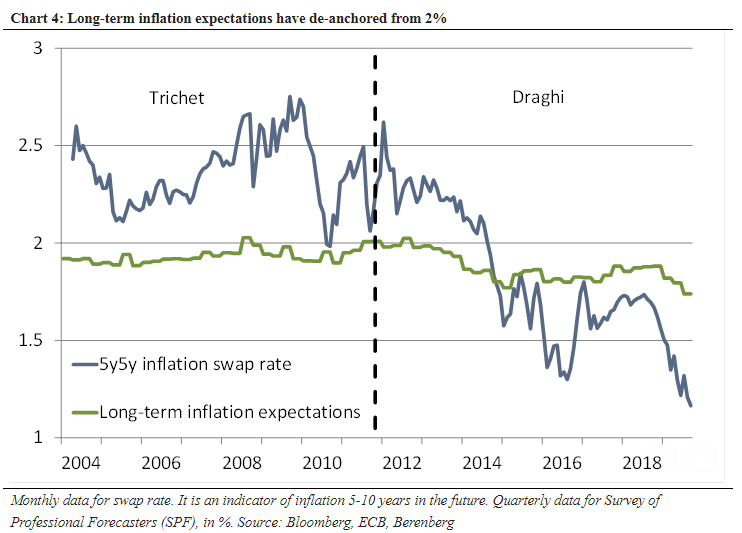

Above: Eurozone consumer price index inflation expectations under former and current ECB regimes. Source: Berenberg.

"Inflation expectations matter. Effectively, forward-looking central banks target expected rather than actual inflation. Monetary policy acts with a lag," says Berenberg's Hense. "Baring an upside surprise in inflation and irrespective of a more growth-friendly fiscal policy, bridging the gap between actual inflation and the ECB’s target will require further monetary easing or a more flexible interpretation of the inflation target."

The ECB needs faster growth if it's to meet its long-elusive inflation target of "close to but below 2%" but core CPI, which is generally seen as the more accurate and relevant measure of price pressures, was just 1% in October 2019. That's just 40 basis points above the 0.6% that prevailed when the original QE program was announced in January 2015.

However, and with most of its rates at or below zero already, the ECB is now widely seen as being out of monetary ammunition it can fight a mounting Eurozone economic downturn with. The bank resorted last month to pleading with governments to do more to lift their economies, and attempted again Thursday to coax politicians into loosening their purse strings.

"The French PMIs surprised to the upside, sending EURUSD up to 1.1160, but the German and Eurozone PMIs came in slightly below expectations and EURUSD reversed the whole move back down to 1.1130," says Stefan Muller, a spot FX trader at UBS. "The desk maintain a bullish bias as long as the short-term uptrend, coming in at 1.1075, remains intact. The first levels to watch on the topside are 1.1175 and 1.1204."

Above: Euro-to-Dollar rate shown at 15-minute intervals.

"The central bank intends to keep the pedal to the metal until the point at which it is satisfied that core inflation has stabilised at around 2%. This won’t happen anytime soon, indicating a structurally loose monetary policy setting in the Eurozone. We, and most other ECB watchers and investors, have adjusted our forecasts accordingly," says Claus Vistesen, chief Eurozone economist at Pantheon Macroeconomics.

The ECB is widely believed to be close to, if not already at, the so-called reversal rate where further cuts and additional efforts to compress bond yields simply do more harm than good. This is unfortunate for the bank because its monetary policy relies on using reductions in borrowing costs to stimulate increased investment, faster growth and attainment of the inflation target.

Research shows that once the reversal rate is reached, bank lenders and investors simply begin to hoard more cash rather than lend more cash to the real economy. This eventually results in even lesser lending for productive purposes, risking slower growth and even lower inflation. Some staff are said to be fighting a "rearguard action" designed to have incoming ECB chief Christine Lagarde cancel the program once she takes up her post on November 01.

“Europe’s main engine is confirming signs of slowing, German employment has declined for the first time since 2013, this leads us to think that pressure will build for the German Government to start using fiscal stimulus. Overall, markets are not pricing any further easing measures for the time being which translates in EUR trading in tight ranges of late,” says Olivier Konzeoue at Saxo Bank.

Above: Euro-to-Dollar rate shown at 4-hour intervals.

Eurozone GDP growth is forecast by the European Commission to come in at just 1.2% for 2019, below what the ECB's calls 'potential growth'. This means the economy is not growing fast enough to generate any inflation pressures at all, while the outlook for growth in the European and broader global economies is very much contingent upon whether or not a "phase one" deal suspending hostilities between the U.S. and China actually gets inked in November and what the White House decides on EU car tariffs.

German growth fell by 0.1% in the second quarter, the second contraction inside of a year, although two consecutive declines are required for an economy to be considered to be in recession. Data covering the third quarter will reveal whether a recession has hit at 08:00 on Tuesday, 14 November. The government is now said to be expecting GDP growth of just 0.5% for 2019, down significantly from the 1.5% seen in 2018 and the 2.2% seen in 2017.

The German IHS Markit manufacturing PMI appeared to stabilise in October when it rose from 41.7 to 41.9, taking up from a 10-year low, but the services sector PMI missed market expectations. The services PMI fell from 51.4 to 51.2 in October and is further encouraging speculation that the downturn in the factors sector could now be spilling over into the rest of the economy. Draghi referenced this latter risk as a concern for the ECB this Thursday.

"Although broadly unchanged from the previous month, euro area October PMIs show early signs of contagion from manufacturing weakness in services soft data. Our PMI based GDP tracker is now slightly below 0.1% q/q, indicating the region may flirt with stagnation in Q4 below our baseline of 0.2% q/q GDP growth," says Ludovico Sapio, an economist at Barclays.

Above: Euro-to-Dollar rate shown at daily intervals.

TD Securities tips the Federal Reserve (Fed) decision due on October 30 as being more key to the outlook for the Euro-to-Dollar rate than Thursday's ECB shindig, and the terrain of the current relative interest rate landscape still favours the Dollar, according to the Toronto-headquartered investment bank.

U.S. economic data has continued to incite further wagers by the market that the Fed will cut its interest rate again at the end of October, making for a third consecutive rate cut, and a move on the 30th is now fully priced into the market with more cuts eyed for 2020 too. However, economists are not quite as sure as the market that the Fed will be willing to indulge those wagers and TD is also sceptical of the idea the Fed would be willing to deliver them.

"The point here is that there is some speculation that the Fed could even stand pat, and if realized, that would undoubtedly leave USD risks skewed topside going into the meeting. We do not think the Fed is willing to disrupt financial markets at this point, but it is animate the risks around going into the meeting, which are skewed topside for the USD," Issa says.

Pricing in the overnight-index-swap market implies a Fed Funds rate of 1.74% for October 30, which is just more than a 25 basis point cut below the current 2% level of the benchmark, but a still-under-construction Bloomberg consensus suggests only around half of analysts and economists anticipate a cut this month. Some say the Fed will wait until December before cutting again and TD is tipping a correction higher as most likely for the Dollar in the weeks ahead, accompanied by a turn lower for the Euro.

"While we do not think that Powell will be quick to completely close the door to support the economy with more cuts, we think it is far more likely they he (and the Committee) opt to wait and see how the data unfolds after delivering 75bps of cuts and trade talks have pivoted towards a more positive footing. This could serve as the basis for a tactical turnaround in the USD," Issa says.

Above: Euro-to-Dollar rate shown at weekly intervals.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of a specialist foreign exchange specialist. A payments provider can deliver you an exchange rate closer to the real market rate than your bank would, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement