Image © European Union 2018 - European Parliament, Reproduced Under CC Licensing.

- EUR aided in risk-on rally by quarells over ECB bond buying.

- Internal opposition to fresh QE said to be dividing ECB staff.

- Doubts over effectiveness lead to opposition inside the ECB.

- Market spies a central bank that's all but out of ammunition.

- Policy impotence may drive limited EUR gains into year-end.

- Ongoing events at U.S. Fed may strengthen ECB rebels' case.

The Euro was aided higher Thursday by reports of internal opposition to the recent European Central Bank (ECB) decision to resume its quantitative easing program, although an increasingly apparent policy impotence could lift the single currency even further into year-end, according to Monex Europe forecasts.

Dollar weakness and risk-chasing were the order of the day in the Thursday session but Europe's single currency was aided in part of its upward turn by the minutes of September's ECB policy meeting and an FT report revealing quarells in the corridors of the Frankfurt-based institution.

The ECB said last month it will buy €20 bn of corporate and government bonds per month from November 01, as part of an effort to stimulate growth in what is currently being billed as a soft patch for the economy. ECB officials need faster Eurozone growth if they are to meet the long-elusive inflation target of "close to but below 2%" and, with most of its interest rates at or below zero already, the bank had little choice in September but to resort to fresh 'money printing' and to reiterate pleas for governments to do more.

"The euro has been trading higher today as the US dollar broadly depreciates in a risk-on environment," says Simon Harvey, an analyst at Monex. "ECB meeting minutes didn’t add much from what was already given in the press conference, but debates over the restart of QE and purchase limits has pushed bund yields marginally lower and prompted a minor clawback in EURUSD."

Above: Euro-to-Dollar rate shown at hourly intervals.

Members of the ECB's monetary policy committee, which is separate to the Governing Council that makes policy decisions, advised outgoing ECB President Mario Draghi against restarting the program that's already seen it buy a substantial part of the European bond market in the years since January 2015, according to the FT. The committee cited doubts over the effectiveness of the prior program for its recommendation, although staff behind the advice have no binding sway over decisions of the bank.

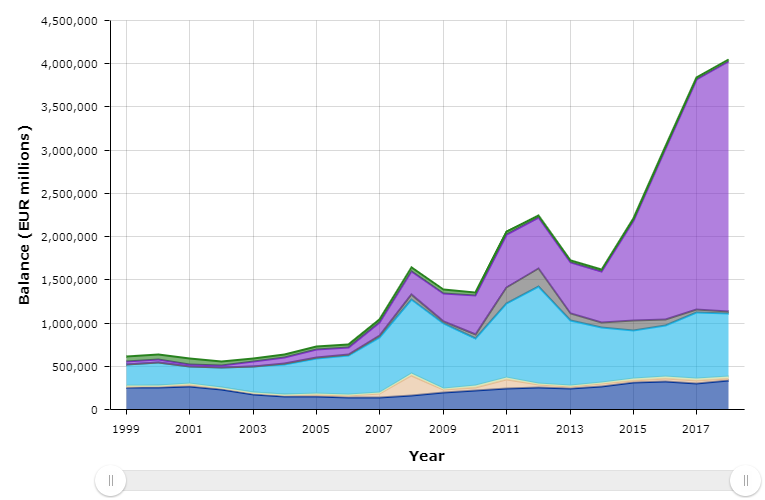

The ECB spent €2.6 trillion buying European bonds in the three years to the end of December 2018 in the hope of reviving a flatlining Eurozone inflation pulse but core CPI, which is generally seen as the more accurate and relevant measure of price pressures, was just 1% in October 2019. That's just 40 basis points above the 0.6% that prevailed when the original QE program was announced in January 2015 and is barely half of what the ECB needs it to be.

"Comments made by Draghi regarding the need for fiscal policy back on the 12th September were more telling than the FT article on opposition within the ECB. Taken together though, the European Central Bank is definitely running out of ammunition to tackle falling inflation and growth levels, any more substantial easing packages will only heighten the negative side effects," Harvey told Pound Sterling Live on Thursday.

Above: ECB balance sheet assets. Purple shaded area represents QE bond holdings. Source: ECB.

September's decision was controversial because the ECB is believed to be close to, if not already at, the so-called reversal rate where further cuts and additional efforts to compress bond yields simply do more harm than good. This is unfortunate for the bank because its monetary policy relies on using reductions in borrowing costs to stimulate increased investment, faster growth and attainment of the inflation target.

Research shows that once the reversal rate is reached, bank lenders and investors simply begin to hoard more cash rather than lend more cash to the real economy. This eventually results in even lesser lending for productive purposes, risking slower economic growth and even lower inflation. Put differently, the ECB has all but run out of ammunition, which is bad for the economy but might have a positive impact on the Euro-to-Dollar rate. Although Monex says any impact is likely to be small.

"Many claim that a floor under rates would cause a floor under the euro in terms of relative rates due to the Fed embarking on a cutting cycle too – the marginal effect in our opinion will be limited and we forecast EURUSD to reach 1.12 by the end of the year for this reason," Harvey says.

Above: Euro-to-Dollar rate shown at daily intervals.

The FT has described the monetary policy committee as fighting a "rearguard action" designed to have incoming ECB chief Christine Lagarde cancel the bond buying program once she takes up her post on November 01. If that's an accurate characterisation and there is any hint in the coming months that they might be succesful, then the Euro could conceivably see more uptake from investors as European bond yields would be likely to rise.

It remains to be seen if the committee will succeed in its action to end the program, which has not been given an end date by the ECB, although they might be aided in their arguments by recent and ongoing developments in the U.S. financial system. Fiscal and monetary 'hawks' in Germany and other European countries have always asserted that quantitative easing amounts to the financing of governments and in a roundabout way, events at the Federal Reserve might just prove them right to some extent in the near future.

If the Federal Reserve is forced to admit at any point in the months ahead, that it will never truly be able to take back the money that was indirectly loaned to the U.S. government through the Fed's own multi-trillion Dollar post-crisis QE program then claims of 'monetisation' and the same old cries about financing of governments could see more influential voices from some parts of Europe begin to throw their weight behind the ECB monetary policy committee.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement