A note institutional currency analyst says Pound Sterling's good run against the Euro is ultimately likely to go into reverse.

This week has seen the Pound-to-Euro exchange rate make an impressive 0.90% advance to 1.1342 amidst a broad environment of Sterling outperformance.

However, amidst the positive price action in the exchange rate, we have reported that there remain some currency professionals who remain sceptical as to how sustainable Sterling's advance against its cross-channel partner might be.

We can report today that the Pound will struggle to appreciate against a resurgent Euro during the year ahead, according to Commonwealth Bank of Australia, and may not be able to avoid a return to last year’s lows at some time or another as the Brexit negotiations roll on.

The warning from CBA comes a day after we reported two major investment banks - UBS and JP Morgan - were of the view that Sterling would ultimately return to the 2017 lows located around 1.08 at some point in 2018.

Broadly speaking, strategists at CBA see Sterling trading within a tight range against the Euro during 2018, although the lower end of this range suggests a return toward earlier lows is likely in the months ahead.

“We anticipate EUR/GBP will trade in a tight range over the coming year, reflecting broad EUR outperformance,” says Richard Grace, chief currency strategist at Commonwealth Bank of Australia.

The British currency has performed strongly in early January as traders responded to a number of soft brexit cues, including reports that Spain and the Netherlands are keen to keep the UK as close to the European Union as possible.

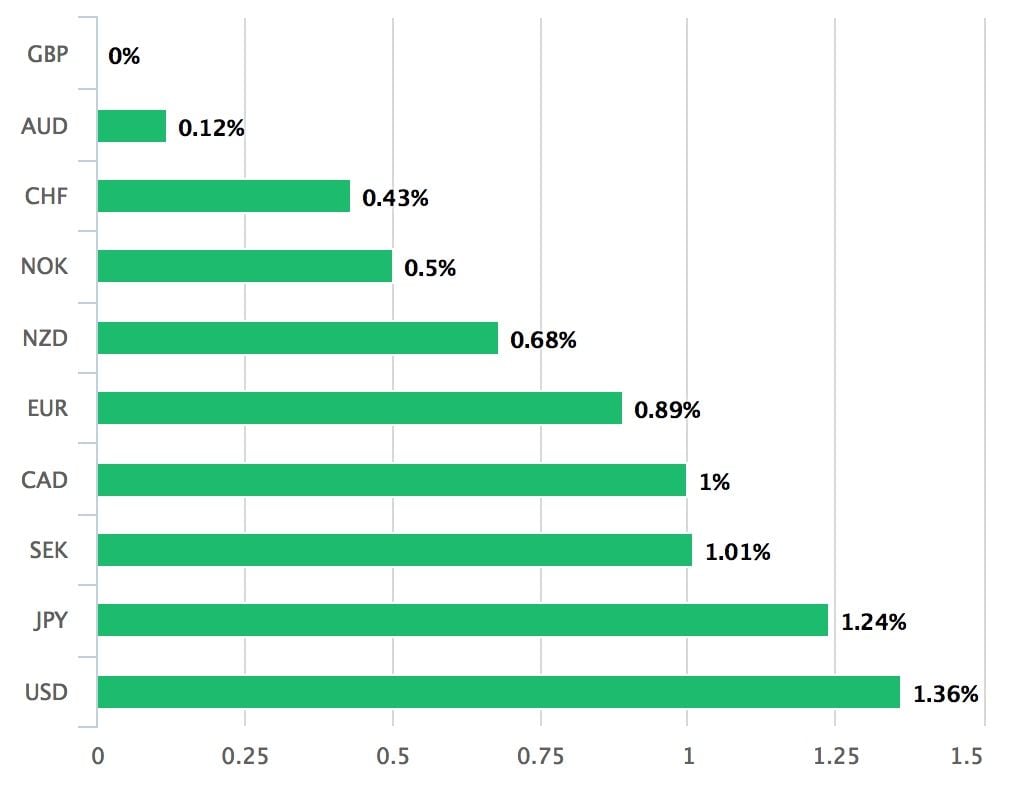

Above: Pound Sterling was the best performing major currency of the week January 15-19.

At the same time, European lawmakers were also said to be considering watering down efforts to force financial clearing houses to decamp from London after Brexit.

This augers a more conciliatory approach to talks between the two sides, as well as increased hopes of a so called “soft Brexit” or a BINO (Brexit in Name Only).

But a forthcoming renewal of the Brexit negotiations is a potent risk to these recently improved sentiments toward the Pound argue CBA.

“We anticipate GBP will struggle to appreciate over the coming months reflecting poor optics at the beginning of EU-UK trade talks in March,” notes Grace, in the Australian bank's latest review of European currencies.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.

Recovery on a Brexit Deal

Sterling's January’s rally against the Dollar and Euro followed another strong period of performance throughout December, which came in response to the European Council voting to allow Brussels’ negotiators to begin discussing the future relationship.

Phase two will see Prime Minister Theresa May attempt to negotiate the future trading relationship between the UK and the EU as well as a period of transition to the new model, with talks set to renew later in January.

“The beginning of the negotiations are likely to be acrimonious, and we anticipate heightened rhetoric from the EU and UK negotiation teams,” says Grace.

All of this will be carried out under fire from the opposition Labour Party, which is armed with a seemingly endless book of blank cheques it is brandishing to woo the voting public, while the government remains under close scrutiny from rebels on both sides of the Brexit divide within the PM’s own party.

But a recovery in Sterling should ultimately occur as, “over the medium-term we anticipate a trade agreement will be reached, which will remove uncertainty. Consequently, trade weighted GBP will likely lift over the medium-term,” Grace writes.

The Commonwealth team say the UK is most likely to be offered a trade agreement along the lines of the EU-Canada trade pact, often referred to as CETA (Comprehensive Economic and Trade Agreement).

This would cover most goods and some services, but importantly for the UK, not financial services. The UK buys a far greater volume of goods from EU countries than those countries do from the UK, while the opposite is true in terms of services.

However, crucially, much of the UK’s “services surplus” comes from exports of financial services, which wouldn’t be covered by a CETA type deal if it were copy and pasted as it exists today. Therefore, it could be seen as a one-sided deal.

“We anticipate the Bank of England (BoE) will raise interest rates by 25bps in Q3 2018 and subsequent rate hikes will be limited and gradual. Markets have priced in one more BoE rate hike. Consequently, GBP is unlikely to benefit significantly unless the BoE surprises markets with further or earlier interest rate increases,” Grace says.

The Bank of England Could be the Wildcard for Sterling

The Bank of England raised interest rates in November for the first time since the financial crisis, a move that can in some part be credited to Sterling's strong performance towards the end of 2017.

The rate rise helped lift Sterling off from the post-referendum lows its saw relative to the Euro in August 2017 however, markets have been reluctant to bet heavily on another move coming from the BoE anytime soon.

There are reasons to think this market-reluctance might change over the coming months although this cannot be taken for granted.

“The risk to the EUR/GBP forecast is on the downside. UK productivity growth, which has disappointed since the financial crisis, is starting to show notable improvements,” Grace notes. “If this trend continues, upward UK GDP growth revisions may lead to better GBP performance.”

Indeed, the research comes in the same week that markets digest the first communication from the Bank of England in the form of an assessment given by Monetary Policy Committee Member Michael Saunders.

Saunders delivered what we consider to be an upbeat assessment of the UK economy, saying wage rises should breach 3% in 2018 and this will ultimately force the Bank of England to reassess interest rate settings.

If Saunders is correct, the market might be underestimating the path of future UK rate rises; and this will certainly bode for a stronger Pound.

CBA's Forecasts for the Pound

Grace and the CBA FX team forecast the Pound will trade between 1.0989 and 1.1360 against the Euro during the year ahead, which implies there is little upside to be had from the current 1.1340 level.

Sterling should fare better against the Dollar, according to CBA forecasts, rising from its current level of 1.3900 to 1.4200 by year end. However, this expectation is more than result of anticipated Dollar weakness than it is hopes of Sterling strength.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.

Retail Sales Don't Dent Enthusiasm for Sterling

Pound Sterling is still the best performing G10 currency this week after shrugging off some dire news from the UK retail sector.

The Pound appeared to shrug off a steeper-than-expected fall in UK retail sales in the month of December, the details of which were released on Friday, January 19.

The resillience suggests there may be scope for the British currency to cling to its best-performer crown as the week draws to a close.

Office for National Statistics data showed UK retail spending fell by 1.5% during December, a steeper reduction than the 0.8% decline expected by economists, while fourth-quarter growth came in at a measly 0.4%.

Economists had predicted retail sales would grow by 0.8% for the final three months of the year, which would have been in line with the expansion seen in the third quarter.

The annual pace of growth in high street spending, at 1.9%, was the slowest since 2013.

Consumers, after all, faced a steep rise in inflation during 2017 that put pressure on real incomes and spending.

"A fall in retail sales volumes in December had always looked likely, given November’s hefty rise," says Ruth Gregory, a UK economist at Capital Economics. "After all, UK retailers’ adoption of “Black Friday” discounting appears to have caused consumers to bring forward their Christmas purchases, rather than to buy more overall in recent years."

December's data followed surprisingly strong growth of 1.1% in November although this expansion now looks to have been more than reversed.

Friday's report came closely on the heels of dire news for home furnishings retailer, Carpetright, which saw its shares crash by nearly half after posting a surprise profit warning confirming the UK high street finds itself in a precarious position.

"Despite a positive start to our third quarter, we have seen a significant deterioration in UK trading during the important post-Christmas trading period," Wilf Walsh, chief executive at Carpetright, announced Friday.

"While average transaction values were up year on year, the number of customer transactions since Christmas was sharply down, which we believe is indicative of reduced consumer confidence."

The impact on Sterling of the headlines was ultimately muted however.

"A disappointing set of retail sales figures out of the UK has done little to dent the ascendancy of the Pound, amid a week of upside for sterling. However, today’s figures should be taken with a pinch of salt, with the deterioration in December retail sales coming amid a shift in shopping trends, towards the black Friday/cyber Monday fuelled November rather than last minute pre-Christmas spending in December," says Joshua Mahony at IG.

The Pound was quoted 0.22% higher at 1.3920 against the US Dollar after the release Friday, broadly unchanged from before the retail sales data were announced, which is its highest level since the referendum of 2016. The Pound-to-Euro rate was seen 0.20% lower at 1.1338.