The Euro remains the driving force in global FX in mid-2017 having bounced against the world’s top twenty currencies in the wake of signs that the European Central Bank could be looking to start the process of squeezing their gargantuan money-printing programme.

ECB President Mario Draghi’s comments made at a central banking symposium in Portugal had investors betting conditions for a stronger Euro were indeed becoming entrenched.

“It was his shift of emphasis from ‘very substantial’ to ‘considerable’ where stimulus was concerned that really got everyone talking,” says Chris Beauchamp at IG in London. “This Delphic hint that a reduction in QE was possible was sufficient to send the Euro higher.”

Analysts believe the Euro should maintain an advantage going forward.

Against the Dollar consensus estimates now believe the EUR/USD will close 2017 above 1.10; a notable shift for a community that were eyeing levels towards 1.05 over the course of preceeding months.

Some are even eyeing a more aggressive advance towards 1.20.

“The EUR looks very cheap,” says Themos Fiotakis at UBS. “There is the view that Europe's large current account surplus may largely reflect a lag in Eurozone's cycle. Yet, even after we adjust for the cyclical nature of the current account, the Euro still looks cheap by a wide margin.”

UBS believe the Euro to be undervalued by as much as 23% and studies of the Eurozone’s current account standing (the Eurozone’s bank balance with the rest of the world based on trade and foreign earnings) supports their long-horizon bullish view on the Euro.

Pound Particularly Vulnerable to Euro Strength

The Pound is meanwhile said to be particularly vulnerable to the Euro.

“The GBP is quite expensive even in light of the recent C/A improvement – stress-testing the current account to Brexit risks as well as risks from fading global reflation implies significant downside risk for sterling,” says Fiotakis.

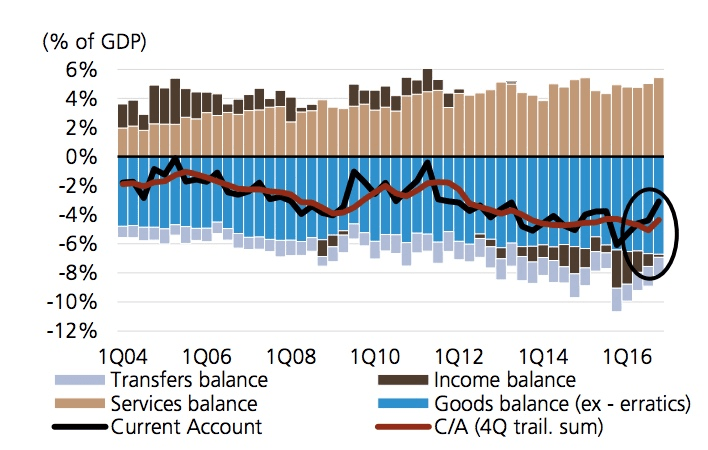

The UK’s current account is in deficit owing to the country’s large reliance on the import in goods. A decline in the value of earnings on foreign-owned assets are meanwhile also seen as contributing to a scenario whereby the country’s books are balanced by inflows of foreign investments.

Should these inflows cease, the Pound will be left looking incredibly vulnerable.

Above: The UK's current account balance has deteriorated significantly in recent years.

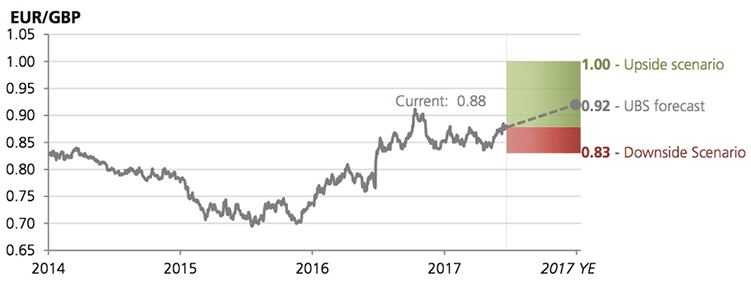

“We remain bullish EUR/GBP and EUR/CHF, and would trade continuing growth recovery in the Euro area,” says Fiotakis backing a rise in the Euro against the Pound and Franc.

UBS are forecasting the EUR/GBP exchange rate to trade at 0.90 by the end of the quarter-three 2017, 0.92 by end-2017 and 0.97 by end-2018.

This is equates to a Pound to Euro exchange rate of 1.11, 1.0870 and 1.0309 respectively.

"Recent improvements in the current account via the income balance have decreased the scope for sterling weakness, other things equal. That said risks are firmly skewed to the downside," say UBS. "Sterling remains vulnerable to a downturn in the global cycle and Brexit-related uncertainties add to these risks."

Recall an article we published at the beginning of June that warns that there was even a scenario set out by UBS that sees the Pound to Euro rate going as low as 0.95.

There are a wide-range of outcomes seen by the Swiss bank, but the unifying factor is that they all factor Pound weakness.

Draghi Greenlights Euro Strength

the Euro enjoying its strongest day in more than a year in response to European Central Bank President Mario Draghi’s suggestion that Eurozone’s improving economy no longer needed the central bank’s “very substantial” support.

Above: Watch ECB President Draghi talk up the Euro at the ECB Forum on Central Banking in Sintra, Portugal.

This support, in the form of record-low interest rates and quantitative easing, has long kept the Euro well below fair-value.

Analysts at UBS say some of their studies suggest EUR/USD fair-value could be as high as 1.25.

“President Draghi's more hawkish inclinations have set tongues wagging, with markets now seeing the end of the ECB's QE policy as a matter of when, not if,” says Viraj Patel, an analyst with ING Bank N.V.

The Euro raced higher against all its competitors. The EUR/GBP exchange rate is seen extending gains to reach a seven-month best at £0.8874 at the time of writing, having started the week at £0.8799. This equates to a seven-month low in the Pound to Euro rate at 1.1269.

The EUR/USD exchange rate is at nine-month best at 1.1358 having started the week at 1.1119.

But some analysts warn that the Euro might struggle to find further upside traction following its recent good run.

“In light of positive Eurozone data, few can question Draghi's optimism and for this reason, the move in EUR/USD could extend as high as 1.15,” says Kathy Lien, Director at BK Asset Management in New York.

But Lien cautions that it is also important to realise that a large part of the rally can be attributed to ‘short-covering’ and that "flow will start to ease as sellers turn into buyers".

Short-covering is the process whereby those who were originally betting against the Euro liquidate those trades; so it is a technical phenomenon.

“Investors should not get carried away,” warns Viraj Patel at ING. “The implicit reference to removing accommodation in line with changes in the neutral rate suggests a very slow normalisation process.”