Pound sterling has been consolidating for days now but there are reasons to be optimistic that an upside break could ultimately transpire.

- Upside is forecast, but there are limits according to the dates considered

- Once market orders are cleared out of the market expect freedom for the GBP to EUR exchange rate to extend higher

- Bank of England to provide sterling with near-term direction - what to expect?

Pound sterling has been stuck in a rut against the euro of late with the GBP/EUR pair successfully defending the 1.26 area but unable to stage any notable bounce.

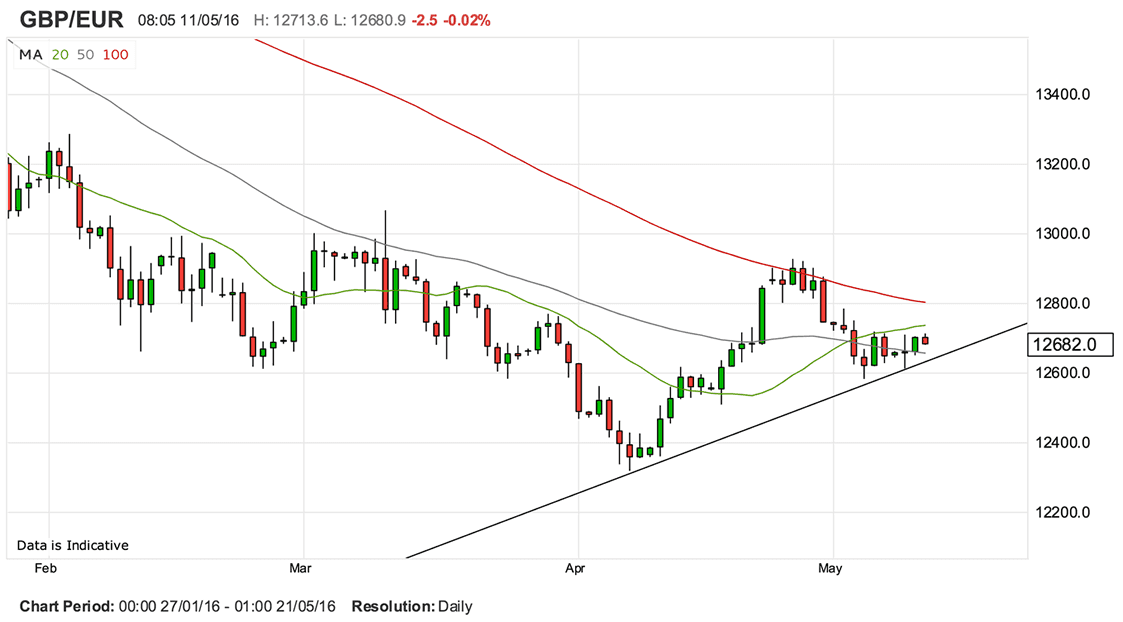

The upside has been capped by the late 1.26s/1.27 confirming a tight range that has been in place for eight trading sessions now.

Such consolidation is unusual and when a breakout of the range comes there is a chance it is a notable one.

Therefore we are left considering whether the break will be to the topside or downside and in the absence of fundamental drivers we have to consider the underlying structure of the GBP v EUR market.

Technical studies suggest that an upside break should be preferred based on the observation that sterling’s April/May recovery is still valid.

If we look at the below chart we can see a trend line between the lows exists, and it appears to have been respected even through this period of consolidation.

So, on the assumption the trend-line will be respected we could expect gains. But how far will they extend?

It must be noted that the 100 day moving average continues to descend and late April’s rejection by the 100 day moving average confirms it is a force to be reckoned with.

There remains significant selling interest at the 100 day average with traders setting sell orders here in anticipation of a resumption of the move lower.

We would imagine the validity of this scenario to remain valid were GBP/EUR to find upside traction and therefore look the the current position of the 100 day moving average at 1.28 to be the target.

Should a break of the average take place then we would be confident that a more sustained recovery may be enjoyed - this is because the sell orders layered around the resistance point will have been cleared out allowing buyers unhindered access to higher levels.

Latest Pound/Euro Exchange Rates

| Live: 1.1604▲ + 0.03%12 Month Best:1.1754 |

*Your Bank's Retail Rate

| 1.1209 - 1.1256 |

**Independent Specialist | 1.1442 - 1.1488 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Of course we must respect the fundamental fact that with the EU referendum fast approaching reading the market could become increasingly hard to do and with this in mind we must keep in touch with movements on the odds markets.

While the polls are tight markets are more inclined to take guidance from the odds markets which have been proven by recent history (Scotland referendum, 2015 General Election) to be more accurate in pricing the outcome.

Odds for an EU exit currently stand around 33% and only a notable push towards the make-or-break 50% area would really bring the sellers out.

If that were to be the case then those Brexit-inspired forecasts of the pound falling to 1.10 and even parity against the euro could be realised.

Most big-name analysts continue to base their forecasts on the assumption that the UK will vote to remain in Europe and therefore a decent recovery could transpire post the June vote.

In fact I would argue that a break of that 100 day moving average mentioned above would only likely occur on such an event - be under no doubt it will take something big to break that resistance zone.

Lloyds Bank told us this week they are forecasting levels above 1.30 over coming months and we can only agree.

Bank of England is Near-Term Fundamental Driver

The Bank of England delivers its quarterly Inflation Report on Thursday the 12th of May and markets will pay close attention to changes made to the Bank’s in-house inflation and growth forecasts.

There is wide agreement that any sustained uptick in sterling would require higher UK interest rates at the Bank.

Higher interest rates will only come were inflation to be accelerating at a faster-than-expected pace, so upgrades to the UK’s inflation profile could result in some GBP gains.

“The BoE has said that it will ignore any weak data until the EU Referendum is out of the way, so the accompanying Inflation Report and Press Conference will be where to focus. We think recent weak data is mostly related to heightened Referendum uncertainty, but will look carefully at the IR for the BoE’s interpretation,” say TD Securities in a briefing ahead of the event.

If Bank communicates that it sees something more than just Referendum-related uncertainty, it reduces the odds of a late-2016 hike in Bank Rate.

Indeed, domestic data out of the UK has continued to slow with May’s release of PMI data coming in well-below consensus. The manufacturing PMI data even showed the sector to have contracted in April!

There is therefore the chance that the Bank strikes an even more cautious tone than normal based on recent data; this should be GBP negative in our view.

Nevertheless, there are some out there who see the clearing of the mid-year hurdle that is the referendum as an invitation to a 2016 interest rate hike.

Markets are less sure of this and 2018 appears to be the earliest date priced in.

If markets do bring forward this date to align with those analysts who are forecasting a 2016 rate rise then expect the GBP to rally notably