“But in countries that are spending a lot more abroad than they are taking in, the current account is the point at which international economics collides with political reality.” - Atish Ghosh and Uma Ramakrishnan at the IMF.

If you want to know why the British pound could hit parity against the euro over coming months you would be correcy in citing the EU referendum.

So far the debate on Brexit has mainly focused on the potential economic and political repercussions for the UK and the EU alike. But explaining why a Brexit would punish the pound requires an understanding of the UK's trade deficit.

Turning up the heat on the economic debate is one prominent investment bank who warns an exit from Europe could force the UK to come to terms with the consequences of its heavy reliance on foreign imports.

“From a macro standpoint, the main source of risk is the outsized UK current account deficit that currently features as one of the largest in the world,” says Themos Fiotakis, Strategist at UBS.

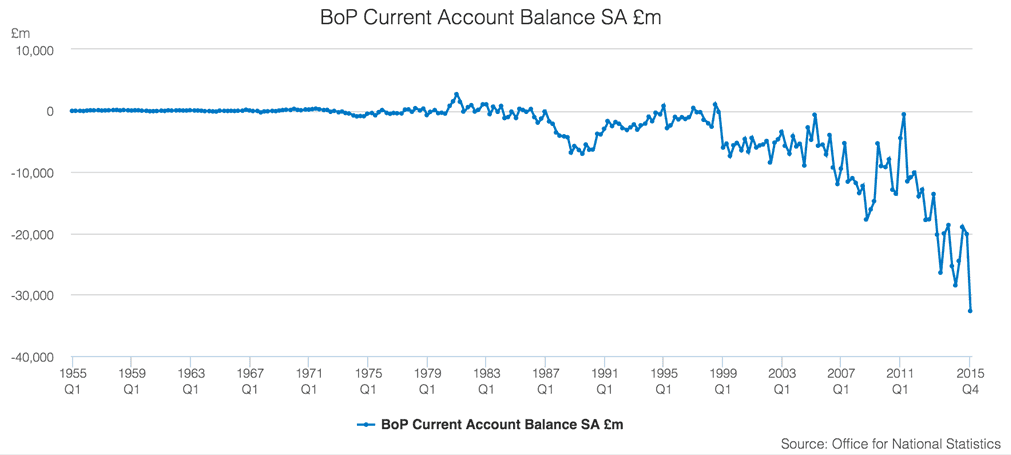

The current account is the difference between the value of exports of goods and services and the value of imports of goods and services.

A deficit then means that the country is importing more goods and services than it is exporting, and the gap is only growing when it comes to the British economy as the UK saw its current account deficit surge to record levels in the final quarter of 2015:

“When a country runs a current account deficit, it is building up liabilities to the rest of the world that are financed by flows in the financial account,” point out Atish Ghosh and Uma Ramakrishnan at the IMF in a paper addressing the potential problems associated with a trade deficit.

One would expect the pound exchange rate complex to be lower on the back of such dynamics as high import demand suggests the pound is being sold to purchase foreign exchange.

But, sterling has managed to remain elevated in the face of heavy import demand thanks to foreign investor inflows into areas such as property, stock markets etc. This ‘financial account’ creates enough demand for the pound to balance out any losses seen on the import-export front.

The question is - what happens to the UK economy when these inflows dry up?

Latest Pound/Euro Exchange Rates

| Live: 1.1676▲ + 0.02%12 Month Best:1.1701 |

*Your Bank's Retail Rate

| 1.1279 - 1.1326 |

**Independent Specialist | 1.1513 - 1.1559 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

A Massive Shock Could Await

Fiotakis argues that while the current account deficit is an issue whether the UK votes to leave Europe or not, the potential for a Brexit scenario brings the imbalance into sharp focus as financial inflows that typically balance the books are stalled on uncertainty.

“Such reversals can be highly disruptive because private consumption, investment, and government expenditure must be curtailed abruptly when foreign financing is no longer available and, indeed, a country is forced to run large surpluses to repay in short order what it borrowed in the past,” argue Ghosh and Ramakrishnan.

Brexit could trigger a confidence shock that stops the incoming flow of money that keeps the exchange rate, and economy, balanced despite the current account deficit.

Pound sterling is therefore most likely to be in the firing line.

The Currency Must Bear the Brunt of the Adjustment

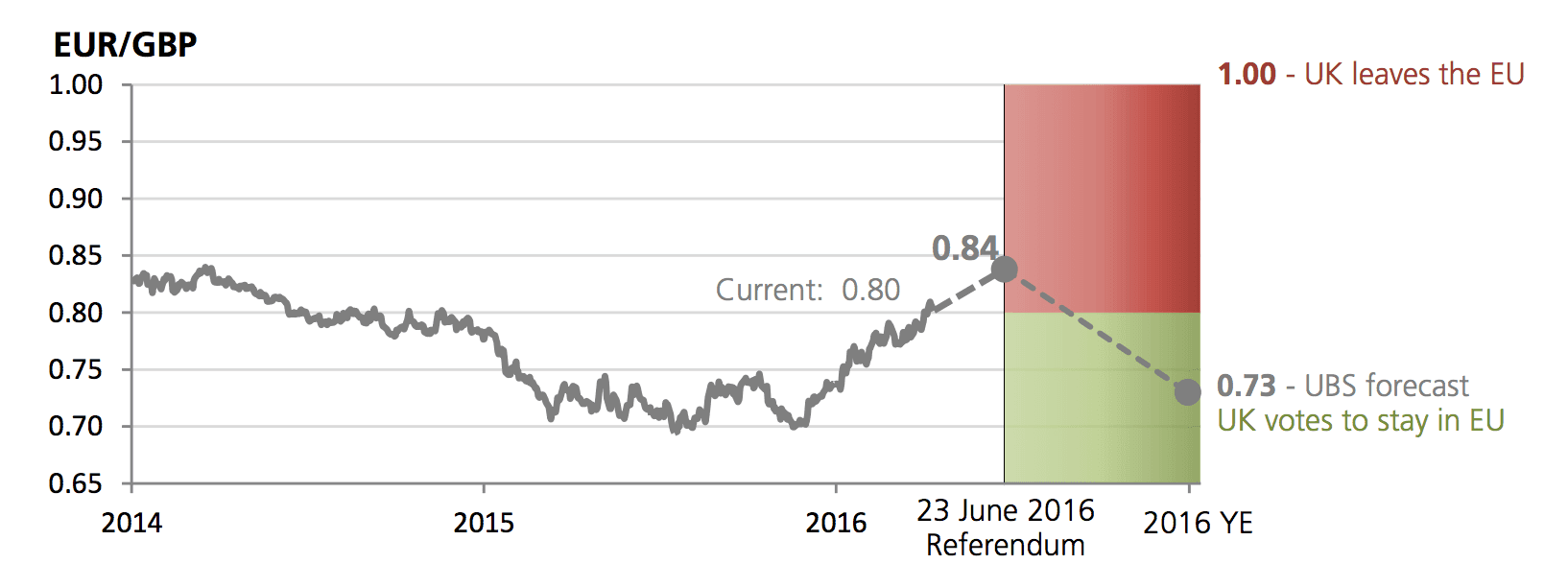

UBS reckon that the British pound ‘nominal effective exchange rate’ has so far depreciated by about 8% year-to-date and there is more weakness to come, particularly if the odds of a Brexit increase.

Right now polling data shows the outcome evenly split, however the odds market remain unchanged in their view of an exit being at around 33% chance.

If that probability moves to 40% the EUR to GBP exchange rate could surge to 0.84.

Under a range of outcomes, the risk is that a vote to leave the EU, or the expectation thereof, could force the UK current account deficit into quick rebalancing mode.

“The currency could bear the brunt of the adjustment if markets focus even more on the imbalance. A range of outcomes is possible, but one risk is that GBP could then depreciate by a cumulative 30% on a trade-weighted basis.”

UBS say it is a “reasonable assumption” that the GBP could par the EUR, a view echoed elsewhere.

EUR/GBP Downside Risks:

- UK votes to stay in the European Union

- Brexit risks do not have lasting impact on economy

- UK economic activity and inflation accelerate

EUR/GBP Upside Risks

- UK citizens vote to leave the European Union

- As we approach the referendum date, uncertainty rises earlier than expected.

Commerzbank: UK Can Weather Impact of Falling Capital Inflows

As mentioned, one of the key concerns is the size of the current account deficit, which is one of the largest in the OECD, and implies that the UK is reliant on capital inflows to cover the shortfall.

However Peter Dixon with Commerzbank in London believes the UK can continue to fund its deficit by running down its net asset position, without running into solvency concerns anytime soon.

There are three reasons cited:

- the negative net international investment position is relatively small;

- the balance sheet is underweight sterling, which implies that the sterling value of the balance sheet rises when the currency depreciates and

- asset values are higher than their book value suggests.

"Although the pound is expected to suffer in the event of a Brexit vote, our simulation analysis suggests sterling will not be permanently weakened, although it may take a considerable time to recover," says Dixon.

Is a Fall in the British Pound’s Value a Bad Thing Though?

Those who argue for a more balanced economy should see the silver lining that a sudden plunge in the exchange rate brings.

A weaker pound means UK exports suddenly depreciate in price - imagine supermarket prices suddenly fell by 30%, how would shoppers react? There would be a frenzy of bargain buying.

The same would arguably go for the UK’s exports; a cheaper pound would arguably boost our exports and close the gap.

Therefore it is not unrealistic to suggest that the UK economy could rapidly rebalance in favour of a more export-orientated model.

And, as the UK exports more so demand for sterling ultimately grow once more.