Staunch anti-Brexit proponents HSBC have told clients they forecast steep declines in the GBP to EUR conversion should the United Kingdom opt to leave the European Union.

Pound Sterling Live first reported on HSBC's forecast for a 15-20% decline in sterling back in February when the report was first released to media. Strange that the bigger publications are only reporting on it now.

Nevertheless an updated version of the report has been released and it is the startling forecast of a fall to parity in the pound to euro exchange rate that has caught our attention.

If you are a decided Out voter be warned, there are not many good points for you in this piece; HSBC are Brexit bears and their research does not contain the kind of balance that, for example, characterises that from Capital Economics who argue leaving the EU is economically a 'nil-sum' game for the economy.

We now know that on 23 June 2016, UK voters will be asked the question: “Should the United Kingdom remain a member of the European Union or leave the European Union?”.

"At stake is the UK’s relationship with its largest trading partner, the future growth of the City of London as a financial hub and the ability of workers to move freely between the UK and EU countries," say HSBC in a note on the matter released mid-week.

The note looks at the economics and investment implications, in the view of HSBC's various analyst teams, of a UK exit from the EU.

Latest Pound/Euro Exchange Rates

| Live: 1.1674▼ -0.01%12 Month Best:1.1828 |

*Your Bank's Retail Rate

| 1.1277 - 1.1324 |

**Independent Specialist | 1.1511 - 1.1557 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

The Currency Reaction is Real

Whether you are pro or anti the EU one thing can't be denied - the British pound is not happy with the prospect of leaving Europe.

Sterling has reacted violently and has fallen to lows not seen since 2014 against the euro and lows not seen since 2009 against the US dollar.

The bank notes that an out vote will be a momentous decision and a vote for Brexit would have potentially huge consequences for all asset classes.

Following a vote to leave, HSBC think uncertainty could grip the UK economy, triggering a potential slowdown in growth and a collapse in sterling.

Pound to Euro Exchange Rate Foreast @ Parity

HSBC's David Bloom and his currency strategy team called the end of the bull run in the US dollar at a time when it was still charging ahead - where most analysts were going with the trend HSBC said 2016 would not be kind to the dollar.

They are being proven correct on this call thus far - will they be correct on their dramatic calls for the EUR/GBP?

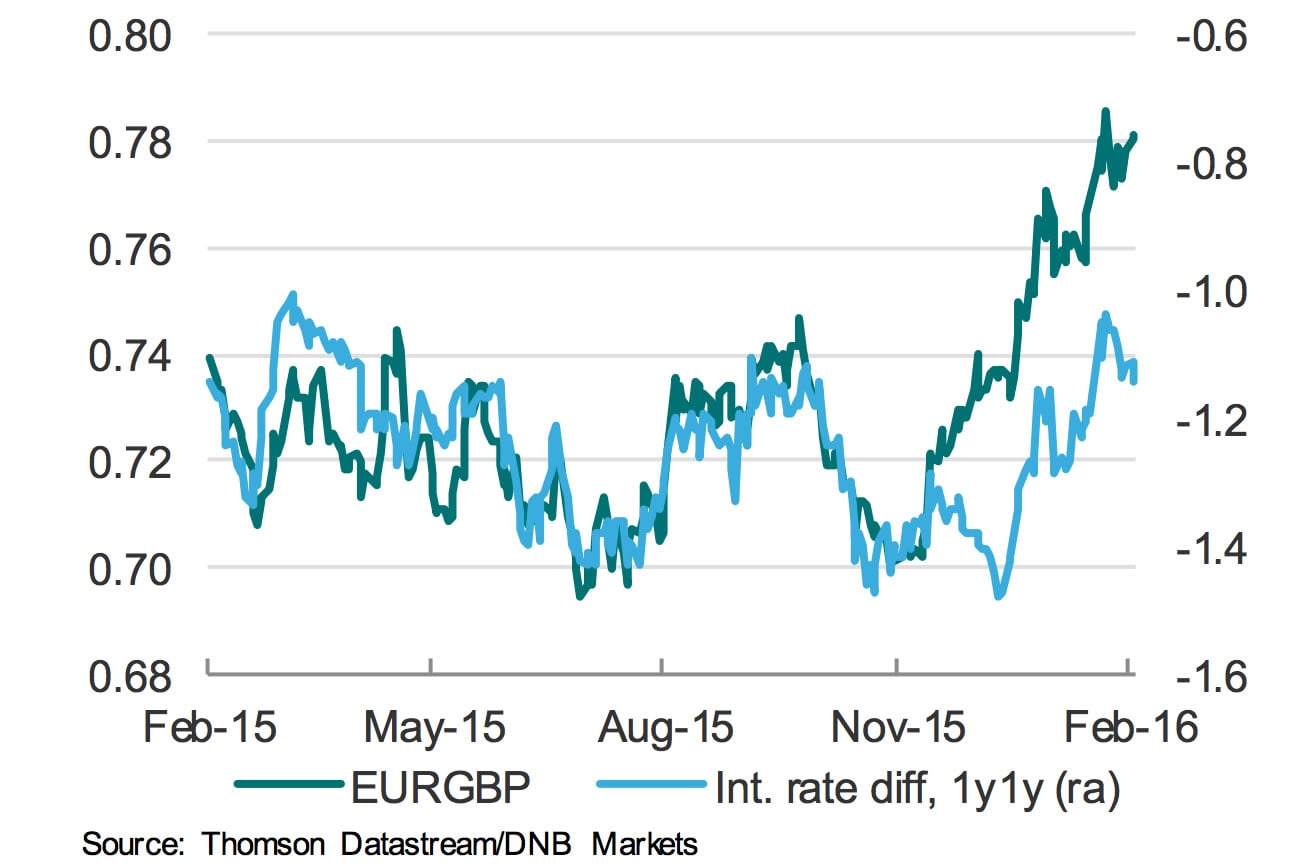

Already a gap has opened up between the observed level of sterling and the level implied by interest rate differentials.

As we can see from the above, the Euro v pound sterling exchange rate usually tracks the difference in yields between the Eurozone and the UK. That is why we, and other, currency commentators spend so much time obsessing over the Bank of England and European Central Bank!

Since December the relationship has broken down, implying something else was happening in the background. The culprit - the EU vote - is now firmly in focus and could well drive the gap further apart.

"If the currency market is pricing in around a 33% probability of a Brexit vote, GBP-USD could fall by around another 15-20% should a Brexit vote occur i.e. if the probability shifted from 33% to 100%," say HSBC.

This would see GBP-USD falling to levels not witnessed since the early 1980s.

"We also think that the GBP would come under pressure against the EUR," say HSBC, "indeed, EUR-GBP could move towards parity in the aftermath of a Brexit vote," say HSBC.

Forecasters see EUR-USD at 1.20 at end-2016, suggesting that EUR-GBP could move close to parity in the aftermath of

“Brexit”.

"And while such an event might create some market concerns about further exits from the EU and Eurozone, we think this would not be reflected as starkly in the EUR compared to the fall out for the GBP," says the note.

The Eurozone also enjoys a current account surplus, making it less vulnerable to short-term financing squeezes than the UK.

This currency collapse could push inflation up by 5pp and raise import prices for firms warn HSBC.

What About the Export Boost Coming from a Weaker Pound?

Both Capital Economics and the Bank of England have recently urged us to look at the brighter side of sterling's decline - the boost it provides to the UK's export sector, and manufacturing in particular.

It is argued that the rebalancing of the UK economy towards exports and manufacturing is desperately needed, hence we should not fear a weaker currency.

Interestingly, the stimulatory effect on the UK export sector is given little mention by HSBC beyond a glance: "UK exports should become more competitive."

The short part-sentence is quickly countered with the argument that, "but sterling would have been driven down by uncertainty surrounding future trade arrangements with the UK’s largest trading partner, which could deter potential buyers of UK exports within the EU, despite lower prices (in EUR terms)."

The argument is sketchy at best - at no point has an argument been made that all trade agreements with the UK and the rest of Europe would be torn apart. Sure, there would need to be some negotiations in the future but the status quo would surely be left in place while negotiations proceeded.

And it is in neither the UK's nor Europe's interest to inhibit trade.

Furthermore, EU companies are rational, profit-driven, entities that will pick up cheap goods no matter where they are produce. Suggesting they would shun sterling-induced bargains on their doorstep is hard to imagine.

Other HSBC Forecasts on a Post-Brexit World:

Growth could be 1-1.5pp lower, roughly halving our current 2017 growth forecast of 2.3%.

Market uncertainty could be good for gilts, given their safe-haven status.

Labour supply would shrink if some existing migrants returned home or restrictions on inflows were imposed.

Sectors with a large proportion of non-British EU workers could face higher labour costs – notably in retail, construction, airlines and facilities management.

In construction, where skills shortages already exist, costs could spiral and limit capacity tom deliver on housebuilding and infrastructure targets.

Uncertainty could hit UK bank stocks, although they should be relatively well placed to weather a growth slowdown.

A reduction in passenger traffic might affect airlines and corporate structures might need to change if the UK left the single EU aviation market.

Immigration raises trend growth and is needed to help close the public sector budget deficit: lower inflows could have long-term consequences.

Over time, Brexit could be beneficial if it allowed the UK to ‘cherry pick’ immigrants from all over the world and forge new trading partnerships.

Regardless of the outcome, the UK should remain a flexible and dynamic economy – the unknown is how economically destructive and drawn out the transition phase would be.

Woodford Brings Some Balance to the Debate

The heads of a third of the constituents of the FTSE 100 have written an open letter to the Times telling the UK voting for Brexit would be bad for the country.

But there are some voices who see the economic arguments against exit as bordering on hysterical.

Respected fund manager Neil Woodford has said he disagrees with the views expressed by the FTSE 100 bosses

Woodford has already stood by the findings of research they commissioned on the matter in which Brexit is ultimately seen as a 'nil sum' game.

"ECB chief Mario Draghi is printing money and trying to do his bit, but the macro headwinds are intense and unemployment remains high. It is these problems that a UK exit could shine a brighter light on," Mr Woodford told the BBC.

He believed investors should be braced for more "extraordinary monetary policy" by the world's central banks, such as negative interest rates and negative yields on 10-year government bonds.

UK Economy Continues to Outperform Rivals

The pound really is undervalued if we were to consider the economics behind the currency.

Coming in unchanged at 0.5% the UK’s second estimate fourth quarter GDP figure places the country atop the G7 growth race for the final 3 months of 2015, the closest rival Germany’s 0.3% expansion.

"The number was enough for the FTSE to increase its gains to 130 points, the index continuing to receive the double bump of a dividend lifted Lloyds and a verdant commodity sector," says Connor Campbell at Spreadex.

The Eurozone’s data was problematic this Thursday; whilst, at 0.3%, the region-wide inflation figure was at its highest point since just before the Grexit crisis last summer, this still marks a drop from the initial 0.4% (and 15 month high) reading.

The data is strong enough to suggest UK interest rates should be rising and should an In vote prevail then we would certainly look for a solid bounce in sterling.

Markets Latest, All Eyes on G20

Market risk sentiment was mildly positive in Asia, as the two day meeting of G-20 finance ministers and central bank heads started in Shanghai.

"Should the UK manage to include into the G20 communique the reference of the Brexit being a risk to the global financial stability, there is a scope for a short-term GBP relief rally on Monday given the large degree of Brexit risk premium priced into GBP," says Chris Turner at ING.

Turner is referring to reports that Chancellor George Osborne is hoping to get a G20 endorsement for Britain to stay in the EU.

China’s central bank Governor Zhou indicated that there is scope for further policy stimulus. In the UK, the GfK consumer confidence fell to 0 in February from 4, the weakest since December 2014.

BoE Governor Carney said that central banks have not run out of ammunition, but that stimulus needs to be well aimed.