Image © European Central Bank

The British Pound looks to extend its recovery against the Euro amidst an easing of pressures in UK bond markets and ongoing weakness in the Euro-Dollar exchange rate.

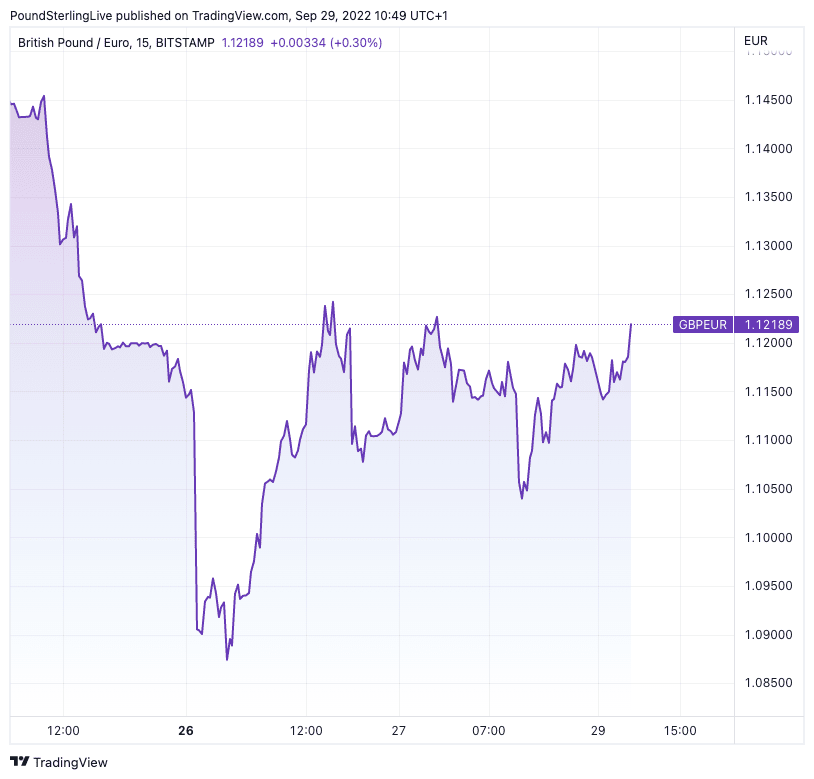

The Pound was flat against the U.S. Dollar in Thursday trade but was higher by 0.40% against the Euro at €1.1212. The pair had been as low as €1.0793 earlier in the week.

The Euro was meanwhile lower against the Dollar by 0.40% at $0.9681 with some unsavoury inflation data out of Germany proving unhelpful.

The Euro was softer after inflation in Germany's most populous state, North Rhine Westphalia, registered its biggest jump since the early 1950s, climbing 10.1% year-on-year in September.

The data lead to fears German inflation due later in the day would show Europe's largest economy is in the grip of a stagflationary crisis, echoing that of the UK.

Separately, Germany’s network regulator said gas consumption was well above average last week and urged households and companies to make more savings to avert a shortage this winter.

"This week’s numbers are very sobering," Klaus Mueller, president of the Bundesnetzagentur, said in a statement.

"Savings must also be made when temperatures continue to fall," he said.

The agency said that gas consumption needs to decline by "at least 20%” to prevent a shortage.

Germany has steadily filled its storage facilities over the summer as Russian gas supplies have been all but severed.

Fears of a winter shortage and rationing could therefore weigh on the Euro over coming weeks and months.

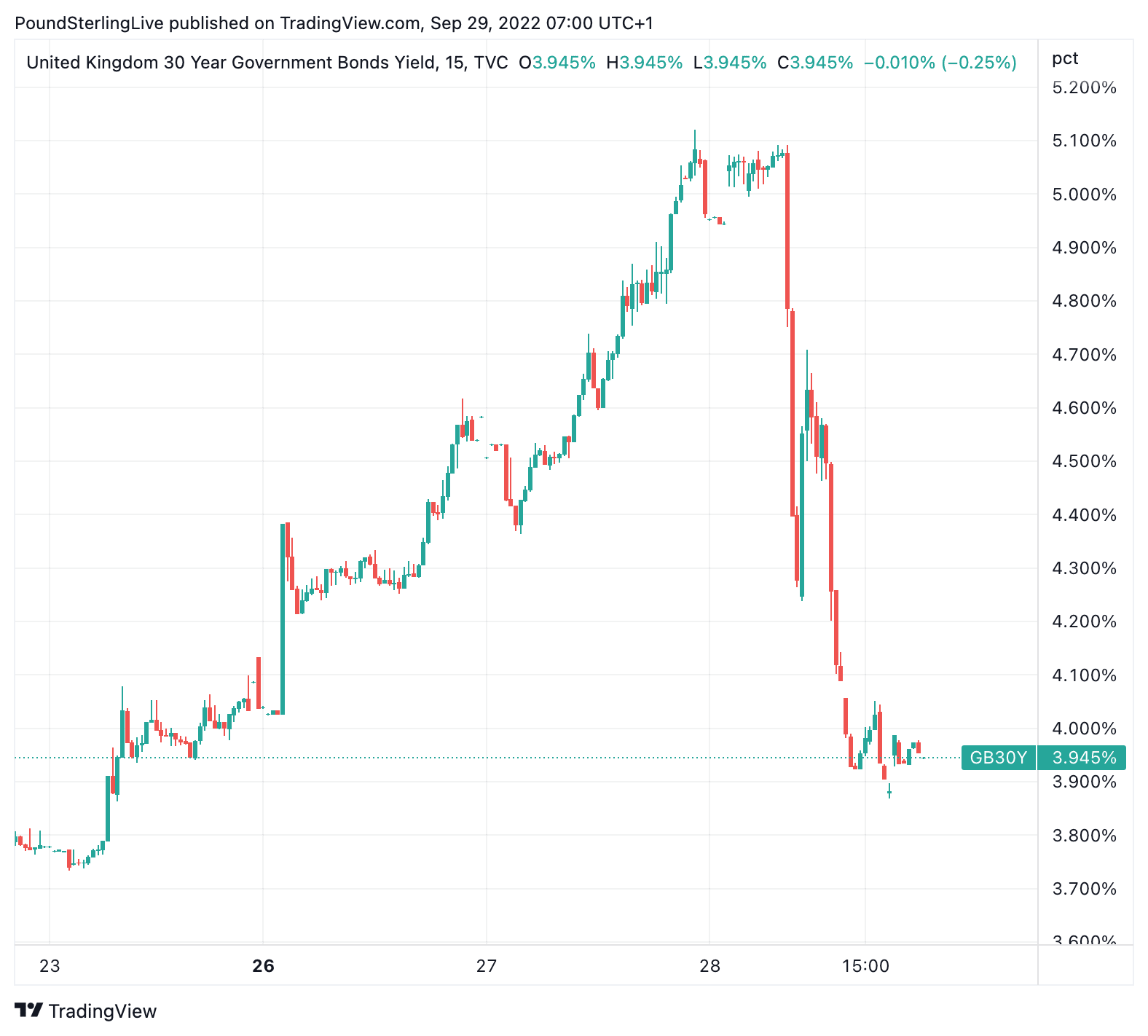

The Pound meanwhile continues to stabilise following severe selling pressure that followed the UK 'mini budget' last Friday, with investors welcoming the Bank of England's recent intervention in the bond market.

Above: GBP/EUR at 15-minute intervals. To better time your FX payments consider setting a free FX rate alert here.

The Pound on Monday fell to record lows against the Dollar and UK gilt yields surged amidst investor concerns the UK government's energy price cap and tax cuts would make UK debt unsustainable.

But surging gilts yields were effectively capped by the Bank of England midweek when it announced it would buy gilts to ease stresses in the pensions market.

The Bank spent around £1BN, far short of the ammunition it had in hand (it said it could spend up to £5BN per auction), suggesting the Bank remains a reliable backstop during times of stress.

Above: The yield paid on UK 30-year bonds fell sharply after Bank of England intervention.

Insofar as turbulent gilt markets are a primary cause of recent Sterling weakness, any subsequent calming of said markets would be beneficial to the Pound.

UK Prime Minister Liz Truss meanwhile said in various media interviews Thursday the government would not backtrack from their recently announced tax cutting agenda.

The announcement of unfunded tax cuts last Friday has been widely blamed for the selloff in UK gilts and the Pound, therefore further weakness in these asset classes cannot be ruled out.

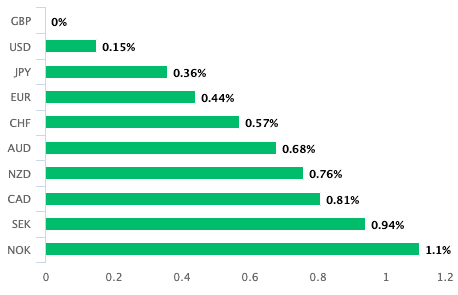

Above: GBP was the best performer in the G10 by midday London time.

There is a risk the current rally in the Pound to Euro exchange rate is a squeeze on investor positioning and therefore technical in nature.

If concerns for the UK's fiscal outlook come to the fore once more the selling pressures could resume.

"For the sharp moves to stabilise, the markets would need to see the nominal anchor restored. This can come in the form of a credible fiscal plan that can stabilise the public finances," says Sonali Punhani, Chief UK Economist at Credit Suisse.

But Credit Suisse is not expecting the UK government to backtrack from its plans, leaving it to the Bank of England to become a channel of support to Sterling.

"We expect the Bank of England to hike rates aggressively from 2.25% to 4.5% by early 2023, with a hawkish pivot in November. A failure to respond aggressively to the fiscal package in November is likely to worsen the confidence problem that the UK is facing and risks further sterling weakness," says Punhani.

Near-term trade in the Pound is likely to remain volatile and it will only be in November when the Bank of England announces its next policy decision and the Government lays out its fiscal programme that any major turnaround could be expected.

Of course, if the government and/or the Bank of England get it wrong, it could be a tough year-end for the Pound.