Image © Adobe Images

The Swiss Franc is forecast to remain strong in 2023 on the back of a resilient domestic economy and its inflation advantage says Swiss private bank, J. Safra Sarasin.

Analysts say the Swiss National Bank (SNB) will remain a source of support to its currency as further interest rate rises can be expected, recognising both interest rates and exchange rates as key levers when targetting lower inflation levels.

Despite the currency's strong appreciation in 2022, "the Swiss franc has not risen substantially beyond its 10y average in real terms," says Claudio Wewel, FX Strategist at J. Safra Sarasin.

The SNB raised interest rates to 1.0% on December 15 and communicated, "additional rises in the SNB policy rate will be necessary to ensure price stability over the medium term."

A shift in SNB policy - that meant it started the interest rate hiking cycle before the European Central Bank - has been instrumental in delivering an advance of 4% against the Euro over the course of 2022.

Meanwhile, a more substantial gain of 9.0% was recorded against the Pound with investors seeking out the safety of the Swiss currency amidst a broad downturn in global equity markets.

However, against the Dollar - 2022's top G10 performer - a 1.40% decline was recorded.

"We expect the SNB to welcome further currency appreciation as this effectively limits the inflation pass-through from abroad," says Wewel.

The Swiss economy has seen inflationary levels far below those registered in the major economies, offering a further positive investor sentiment towards Swiss assets.

"Going forward, we expect the resilience of the Swiss economy to support its currency amid a slowing global economy," adds Wewel. images/2022/H2/SNB-policy-CHF.png Above: SNB FX policy has flipped to being supportive of currency strength.

J. Safra Sarasin's short-term outlook for EUR/CHF warns that a renewed widening of bond yield spreads in the Eurozone, as peripheral bond yields rise, could temporarily push the Swiss franc higher.

The ECB is raising interest rates which put upward pressure on bond yields right across the Eurozone economy.

But the risk is that bond yields rise faster in countries such as Italy and compromise its ability to raise debt, thereby creating stresses in the Eurozone system.

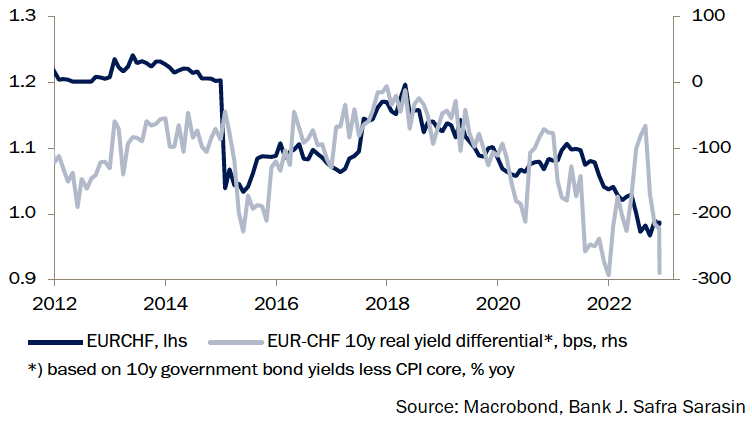

On a medium-term basis, Wewel says the currency should remain strong on the back of low domestic inflation, which keeps the currency's real yields attractive. Global economic weakness should act as further support.

Above: Real yields differentials favour EUR/CHF weakness.

Long-term, J. Safra Sarasin expects the Swiss Franc's appreciation trend to carry on against the backdrop of relative structural advantages, along with a strong net international investment position and high current account surpluses.

The bank's EUR/CHF year-ahead forecast is 0.97 by the end of the first quarter of 2023, 0.97 by the end of the second quarter, 0.96 by the end of the third and 0.95 by year-end.

The forecast profile for USD/CHF is 0.97, 0.97, 0.96 and 0.95.

For GBP/CHF it is 1.11, 1.10, 1.09 and 1.08.

(If you are looking to protect or boost your international payment budget you could consider securing today's rate for use in the future, or set an order for your ideal rate when it is achieved, more information can be found here.)