Above: The SNB. Image © SNB

- EUR/CHF is falling on global flight to safety

- Euro also destined to weaken as ECB prepare

- SNB constrained in preventing CHF appreciation

EUR/CHF has tumbled to a new 2019 lows of 1.1073 at the last reading, and it is at risk of going lower, say analysts at ING Bank N.V.

A combination of trade war fears and a negative outlook for the Euro are seen by ING as the main drivers for a stronger Swiss Franc.

The Swiss authorities are meanwhile likely to resist a stronger Franc, which makes their exports less price competitive, but they may be limited as to the weapons at their disposal to prevent it.

A potential strategy that could keep the Franc pegged lower would be to ‘mirror’ the European Central Bank (ECB) as it prepares to inject stimulus to boost a slowing Eurozone economy.

Since such measures tend to weaken the Euro, the Swiss National Bank (SNB) can, in theory, maintain exchange rate equilibrium by mirroring them and loosening their already ultra-loose policy by cutting interest rates yet further into negative territory.

Such a policy response seems highly likely given given SNB President Thomas Jordan's recent comments in which he stated he would have no compunction in easing Swiss monetary policy, “If we come to the conclusion that it’s necessary to fulfil our mandate, then, of course, we’re ready to use our monetary policy instruments.”

Yet, in reality, it may be highly problematic for the SNB to try to emulate the ECB this time round, says ING, and this could drive a EUR/CHF lower.

“Expect the market to now question the Swiss national bank’s ability to match ECB rate cuts and undertake large scale FX intervention,” says Chris Turner, chief FX strategist at ING in London.

One probable method the ECB might use to stimulate the economy could be to cut interest rates (specifically deposit rates) by 20 basis points, thus making it more expensive for Eurozone banks to park their money with them, and incentivising lending instead.

Yet the SNB could find it difficult to copy such a move and cut its own rates any lower, says Turner, as they are already the second-lowest in the world after Sweden’s Rijskbank, at -0.75%.

The reason is that lower rates create a problem for Switzerland’s banking industry. If base interest rates set by the SNB are low it drags down all other rates, and since a bank’s primary method of making money is to charge interest on loans to customers, a lower rate means less profit. So far the SNB has offset the damage by making exemptions.

“The average interest rates on customers deposits amongst Swiss banks in 2018 was 0.12%, while for large banks it was just 0.06%. No wonder the SNB would have to expand the current (generous) exemptions for negative rates on CHF sight deposits – were they to cut rates further,” says Turner. “This would be especially necessary given the Swiss aversion to negative savings rates – as discussed by our colleagues in the results of our consumer finance poll last year. A separate poll of over 1000 Swiss savers showed 25% keeping cash at home if savings rates turned negative.”

Another method the Swiss might use to offset a weaker Euro is direct intervention in the currency market. This would involve the SNB selling Francs to devalue them.

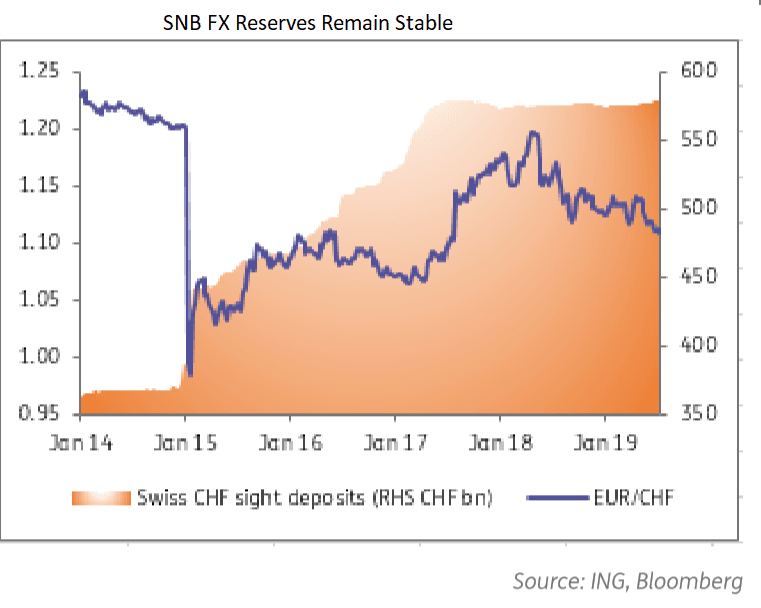

The problem with that is several fold. Firstly, the U.S. would probably accuse the Swiss of being currency manipulators and raise tariffs on their goods. Secondly, the SNB already has extremely high FX reserves from previous interventions. They are now equal to circa 100% of GDP and this creates a financial stability risk from the risk of foreign currency devaluation.

“While the SNB may feel it has unlimited room for FX intervention and to grow FX reserves, the sheer size of reserves, now over 100% of GDP may make the SNB a little queasy,” says Turner.

The other main issue with direct intervention is that it would probably break the US's rules on currency manipulation.

The U.S has three criteria that must be met for a country to be classed as a currency manipulator, these are they:

1) A bilateral goods trade surplus with the US in excess of US$20bn over the last 12 months. 2) A current account surplus larger than 2% of GDP and 3) FX intervention (buying FX) greater than 2% of GDP, again over the prior twelve-month period.

In the last U.S. Treasury report Switzerland just about escaped the first criteria with a US$19bn bilateral surplus, it contravened the second condition with a 10% current account surplus, and on 3) was identified as having intervened to the tune of 0.3% of GDP in FX markets.

It would not be difficult for the Swiss to meet criteria 1) and 3) and be classed as a manipulator, since the SNB conducted very little identifiable manipulation during the report period, and if it really did proper intervention it would easily exceed the 2% line.

“The third criteria could be a challenge for the SNB this year. 2% of Swiss GDP is around CHF 14bn – that is not a lot at all given Swiss FX reserves grew CHF300bn during the ECB’s 2015-2018 QE campaign. Of course, there is no suggestion that the ECB will repeat a three year, EUR 2.5trn asset purchase programme, but even a programme worth one-tenth of that suggests SNB FX intervention could fall foul of the US Treasury rules,” says ING’s Turner.

The end result would be the imposition of U.S. tariffs or - a new idea doing the rounds in washington - ‘reverse intervention’ where the U.S. Treasury would start purchasing Francs.

Nevertheless, the first line of defense where the Swiss might start to resist Fran appreciation would be 1.10, according to ING, which is very close to the current rate.

“As our team points out, the SNB would probably try first to intervene in FX markets to hold EUR/CHF above 1.10, but failure to do so could prompt another small rate cut from the SNB,” says Turner.

Overall, however, ING forecasts the EUR/CHF pair to fall to 1.05 during the coming cycle as the aforementioned factors and scenarios play out.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement