The Australian Dollar is expected to remain under pressure against Pound Sterling over coming days unless the Reserve Bank of Australia's policy meeting can shift the recent trend.

The British Pound has lost ground to the Australian Dollar at the start of the week with the commodity dollar family looking pretty handy.

It would appear that the notable rebound in Chinese house prices reported today are behind the move.

House price growth in China has been slowing since May this year, but the August CREIS (China Real Estate Index System) data highlights a re-acceleration of prices across all tiers.

Richard Knights at Liberum Capital notes Chinese house price growth has been a good lead indicator for the mining sector - and this would explain why the mining-intensive Aussie Dollar has caught a lift.

However, Knights does caution that he doesn't believe the recent acceleration is the beginning of a new upward trend that will drive new starts back to new highs, rather it is a result of buyers stepping into the market ahead of tighter lending conditions.

More Upside for the Pound Expected

The GBP/AUD pair has risen strongly in recent days as a result of widely diverging economic data, which showed a rise in Manufacturing activity in August in Britain but a fall in Retail Sales and Capital Investment in Australia.

The result was a stellar rise in GBP/AUD, which has reached highs of 1.7677 in the previous week.

This is still below a cluster of strong resistance levels likely to cap gains, starting with a trend-line at around 1.7730 and ending just above 1.7830, with the R1 monthly pivot, and resistance from the July highs, falling somewhere in between.

The existing, strong, short-term up-trend should continue higher, rising up to these resistance levels.

A break above the current 1.7677 highs would confirm such a continuation higher to a target at the trend-line at 1.7730.

Above that, and a clear break above 1.7875 would provide confirmation of a clearance, and extension up to 1.8000.

The most significant event in the week ahead for this pair is the Reserve Bank of Australia (RBA) rate meeting on Tuesday.

Whilst few analysts are expecting the RBA to lower interest rates or talk about lowering them, there is a chance s recent data has not been great and the outlook for key export commodities has started turning a little negative, with Iron Ore topping according to some analysts and oil also falling back into its mid-40 range.

“The latest economic reports from Australia were terrible with manufacturing activity contracting and retail sales stagnating.

"However since the RBA met in August, we've actually seen just as much improvement as deterioration in Australia's economy.

"Manufacturing and trade activity improved and most importantly, iron ore prices have found a bottom. So a signal to ease is not a done deal.” Said BK Asset Management’s Kathy Lien.

Broker TD Securities also expect the RBA to ‘sit tight’:

“Unanimous consensus is for the RBA to pause after last month's cut, and we expect the RBA to sit tight now into 2017.” Said TD analysts in a recent research note.

Apart from the RBA meeting Chinese data could also impact on the Aussie in the week according to Lien.

Latest Pound / Australian Dollar Exchange Rates

| Live: 1.9084▼ -0.13%12 Month Best:2.1005 |

*Your Bank's Retail Rate

| 1.8435 - 1.8511 |

**Independent Specialist | 1.8817 - 1.8893 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

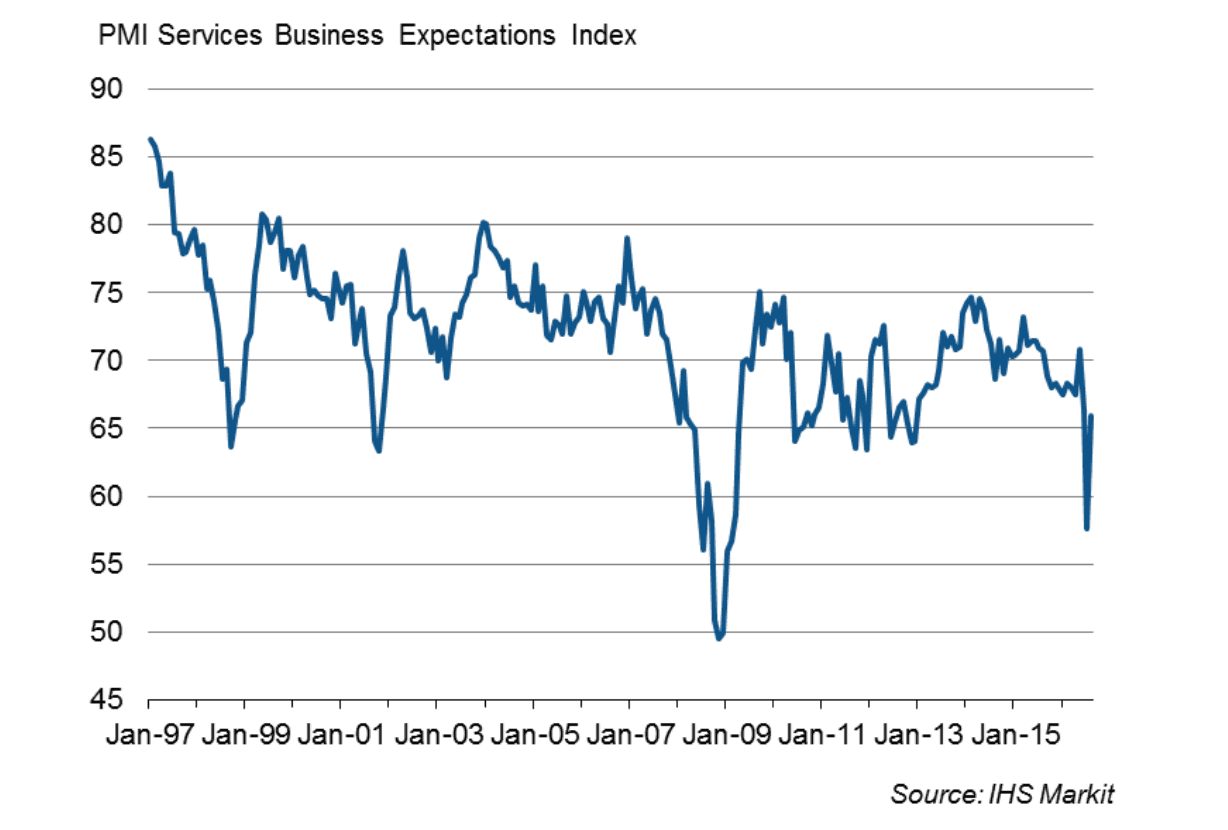

Services Data Gives Sterling a Shot in the Arm on Monday

A strong start to the new week was gifted to Sterling after Services PMI data from IHS Markit and the CIPS have confirmed the economy's largest sector expanded in the month of August, putting behind it the slump seen following the UK's vote to leave the European Union.

The data read at 52.9, well ahead of economist forecasts and market positioning that expected a reading of 50 to be delivered.

Business have reported that the uncertainty posed by the EU vote has started to abate with the forward-looking business expectations index recovering most of the ground lost in July:

Of note, it has also been reported that inflationary pressures are rising as a result of the weakened Pound.

Encouragingly, job creation has resumed in August having paused in July.

"Business optimism ricocheted back to pre-Brexit levels, reassured by market stability and clients bringing dormant projects back to life. Whether this steadiness continues will largely depend on the sector’s reaction to the UK Government’s approach to the Brexit negotiations as the sector keeps one eye on business as usual and one eye on possible obstacles ahead," says David Noble, Group Chief Executive Officer at the CIPS.

The other main release from the UK is Manufacturing Production – with analysts estimating a fall of -0.4% mom in Jul, from -0.3% in June.

The recent rebound in Manufacturing PMI suggests, however, that the consensus estimates may be overly pessimistic.