The Australian Dollar stumbled on Friday the 12th August owing to developments in the Chinese economy which is giving ominous signals concerning the outlook.

The Pound to Australian Dollar exchange rate has just completed its third consecutive weekly decline.

Those with Australian Dollars are looking at their best rate of exchange against Sterling since November 2013.

However, there was a smidgend of disappointment for Aussie bulls on Friday as we saw the currency reverse some of its recent advances.

The GBP/AUD moved higher to 1.6874 while against the US Dollar the weakness took AUD/USD down a notch to 0.7676.

The fall in the AUD stemmed from data out of China which has confirmed a continued slowdown in the economy; to whose fortunes those of the Australian economy are tied.

The headline data was that of Chinese Industrial Production numbers for July which were reported at 6%, below the 6.1% figure forecast.

This is hardly a big miss, which suggests to us more focus may have been placed on news that new credit in China dried up severely in July.

Latest Pound / Australian Dollar Exchange Rates

| Live: 1.9239▼ -0.22%12 Month Best:2.1005 |

*Your Bank's Retail Rate

| 1.8585 - 1.8662 |

**Independent Specialist | 1.897 - 1.9047 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Only ¥25bn of new credit coming from shadow financing was made available, versus expectations of ¥300bn, and new loans of ¥463bn, versus expectations of ¥1,380bn.

New local government debt of ¥396bn is down from ¥1,028bn in June.

“As a caveat this is a volatile data series and credit drawn in the first half of the year will still be having an impact on the economy. To hit the government targets for credit growth of 13%, all system aggregate financing will have to average c.¥1.5tn for the remainder of the year,” says Ben Davis at Liberum Capital.

Davis says the data all points to a slowing down in the Chinese economy, and it “bodes poorly for commodity demand,” says Davis.

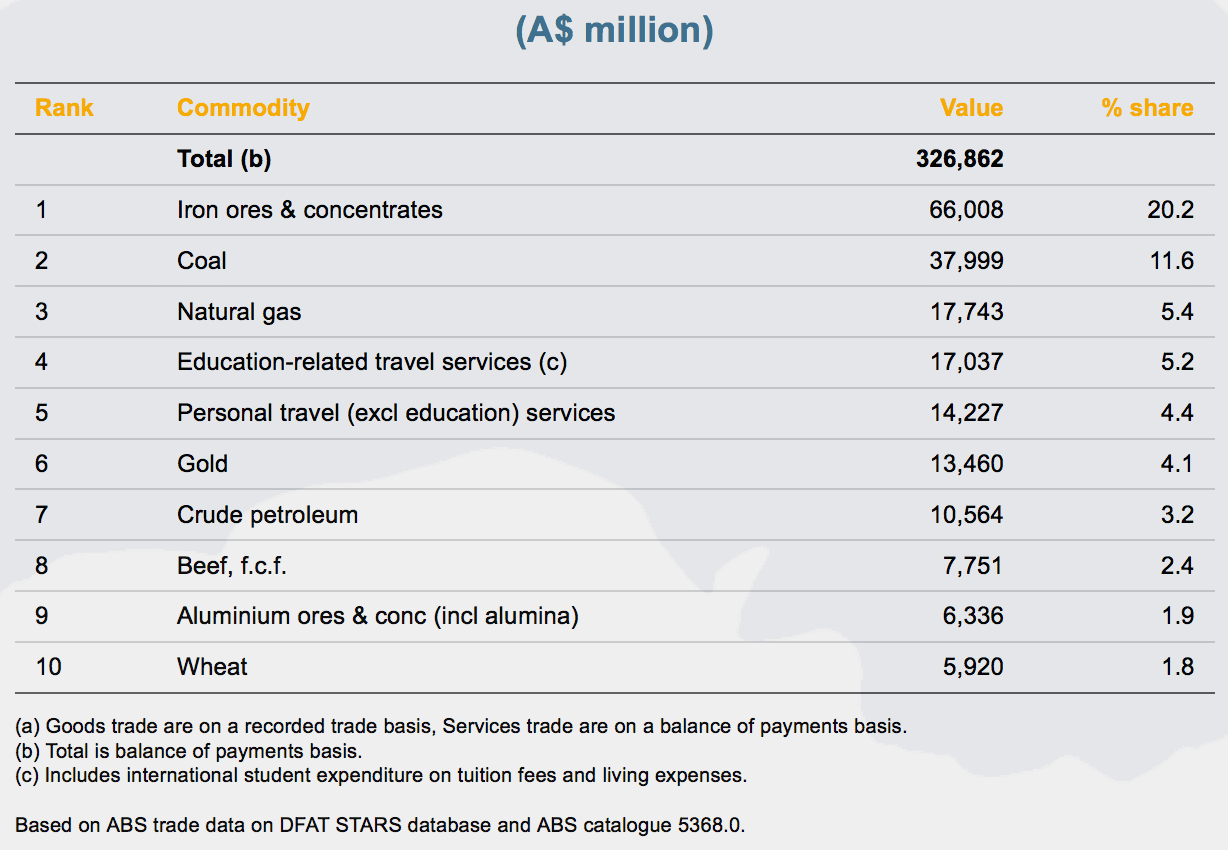

This is a problem for Australia whose top three exports are all commodity orientated:

A falling in commodity prices will hit foreign exchange inflows notably via the current account.

It will also hit the profits of local commodity producers who will in turn rein in investments, hiring intentions, pay rises etc.

Lending was not the only data proving question marks.

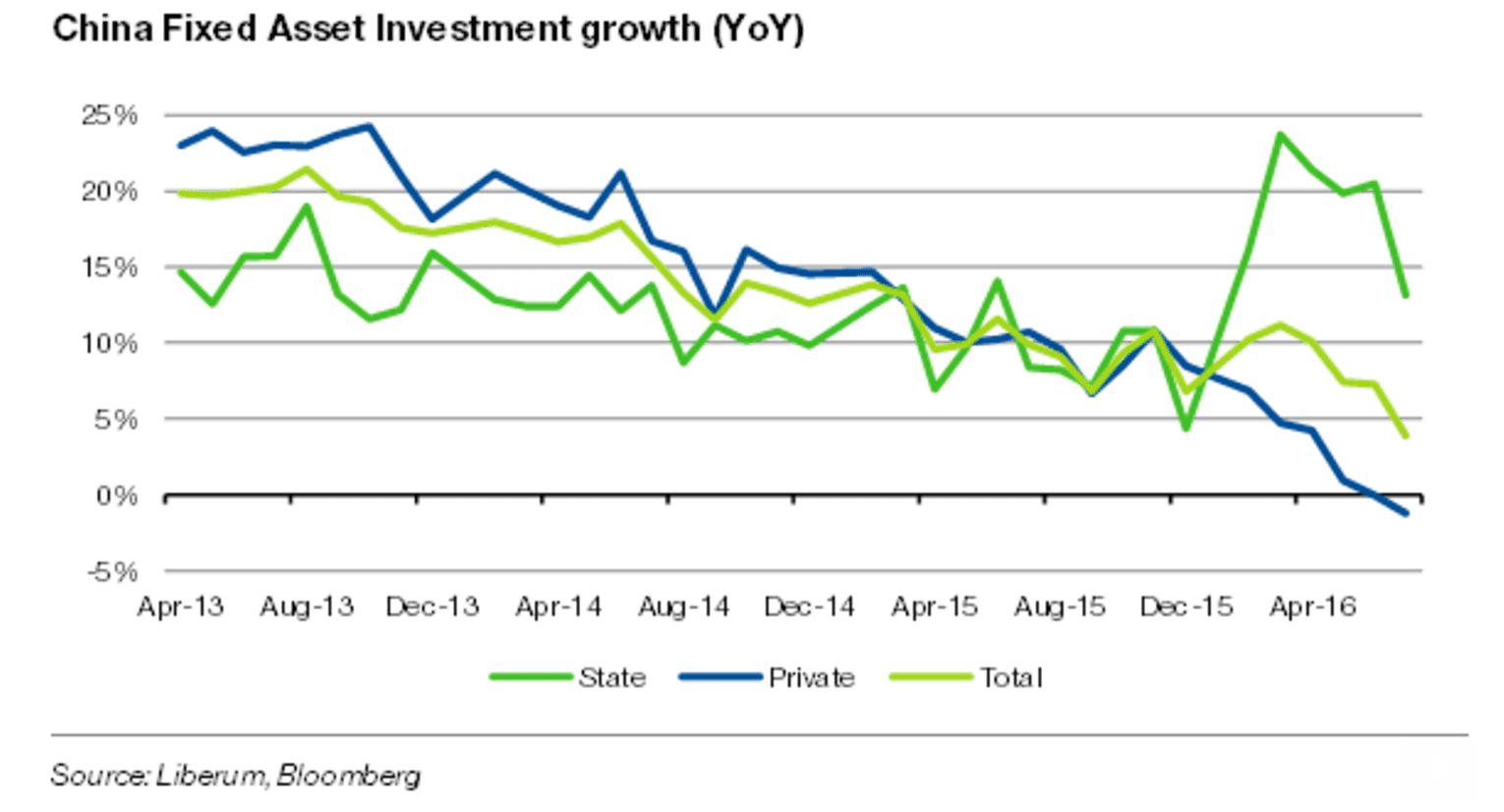

Fixed Asset Investment, the driver of the H1 rally, showed a further marked deterioration in July and land purchases also lurched down.

“Momentum in the commodity intensive parts of the Chinese economy continues to deteriorate, whilst equities continue to shrug off the data. Remain underweight miners,” says Davis.

July fixed asset investment missed expectations, with cumulative growth YTD of 8.1% vs the survey of 8.9% YTD YoY%.

Breaking it down further, private fixed asset investment continue its negative trend and is now -1.2% YoY, a clear result of substantial overcapacity across the economy.

State spending was still up 13% YoY but has slowed materially as the impact from fiscal stimulus begins to wear off.

“We continue to see low risk of further stimulus following comments of the PBoC last week that are prioritising a stable currency and not inflating asset bubbles,” says Davis.

The signals coming out of China will certainly worry the Reserve Bank of Australia, however, any decline in the AUD will be welcomed with open arms.

The RBA appears to be fighting a losing battle against the Australian Dollar - the interest rate cut delivered this month did little to halt AUD appreciation.

This confirms the view that depreciation will ultimately stem from external sources.

The RBA will be hoping that any hit to economic growth via the Chinese channel will be countered by any drop in the AUD.

Why the Aussie Just Won't Fall

The carry trade continues to gain momentum and the AUD is a key beneficiary. This is the process whereby investors can borrow where money is virtually being given away (UK, Eurozone, Japan), and invested in jurisdictions with higher interest rates (New Zealand, Australia, South Africa).

"It’s difficult for central banks to lower their currencies by cutting rates in an environment of low yields globally and a weaker USD," note ANZ Research in a recent brief to clients.

The reaction to the RBA and RBNZ decisions over recent days - when both currencies rose in response to rate cuts - underscore this point.

"Should the AUD push above USD0.80, there is a sharply higher probability that the RBA will ease rates further, though the impact this easing can have on either the currency or the economy is uncertain," say ANZ.

Domestic data has recently elicited little response from markets, but the labour force data (due out next Thursday) will be important given mixed leading indicators.

Data for the Australian Dollar for Week Starting 15th August

On the data front the first significant release for the Australian Dollar is the Reserve Bank of Australia (RBA) meeting minutes on Tuesday.

According to CIBC Capital Market's Jeremey Stretch, “We can expect the RBA minutes to reveal ongoing concern as regards the strength of the currency, while holding out the possibility of yet more monetary easing, although as Stevens underlined earlier in the week merely easing monetary policy is no panacea to broader ills.

However, we can expect the RBA to maintain a campaign for a cheaper AUD, although again they remain rather reliant upon the Fed to play their part.”

On Wednesday the Westpac Leading Index and the Wage Cost Index are released for the second quarter.

Wage costs will be of significant interest to the RBA as they have highlighted sluggish wage growth as a dampener of inflation so a weak result in wage costs will weigh on the Aussie dollar, as it will increase expectations of the RBA further cutting rates in 2016.

On Thursday employment data comes to the fore, with the Unemployment Rate (July) expected to stay at 4.9%, and employment change to rise by 11k.