The GBP/AUD's down-trend looks likely to continue over coming weeks, but there are strong signals that a rebound from oversold conditions is due.

The Australian dollar's period of dominance only looks more entrenched following the slashing of odds for a Reserve Bank of Australia interest rate cut over the past 24 hours.

Markets have cut odds of a May rate cut to 24%, down from 35%, in the wake of PM Turnbull's decision to bring the Budget to May. The clash with the May RBA decision means the latter is unlikely to budge for fear of stealing attention.

The promise of higher Australian interest rates for longer, has only encouraged further Aussie dollar buying.

This leaves the Aussie looking overbought against sterling.

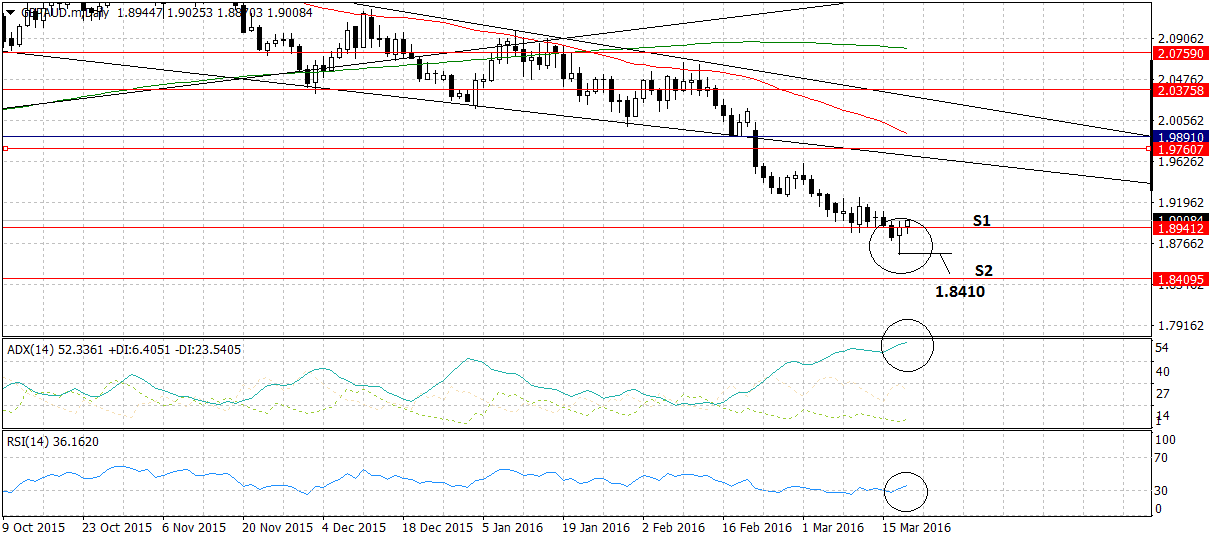

The pound to Australian Dollar rate has formed a text-book hammer candlestick (circled) at the lows.

Hammer’s form at the end of extended down-trends, when the exchange rate moves lower but then recoups most of the day’s losses to close the day back up in the top third of the range.

The hammer warns of a possible rebound, although it is a short-term indicator.

The Relative Strength Indicator (RSI) in the bottom pane is also warning of oversold conditions and is giving a buy GBP/AUD signal.

RSI is a momentum indicator which gives a result between 1 and 100.

When it moves below 30 it is said the asset is oversold; when it moves back above 30 it’s a signal to liquidate shorts and buy the asset instead, as the short-term trend may have changed.

Another indicator, the ADX, is above 50 which is a sign the down-trend is reaching an exhaustion point, providing further indication that the asset may be bottoming.

ADX measures how strongly an asset is trending. When it measures over 50 it is often a sign of over exhaustion. The pair may either now start going sideways for a time or reverse trend and start going higher.

Latest Pound / Australian Dollar Exchange Rates

| Live: 1.9084▼ -0.13%12 Month Best:2.1005 |

*Your Bank's Retail Rate

| 1.8435 - 1.8511 |

**Independent Specialist | 1.8817 - 1.8893 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

The down-trend is in doubt but not ruled out

However, we stress that despite these reversal indicators the down-trend remains dominant and a continuation lower a strong possibility.

This may come after a period of consolidation or a correction. There is insufficient evidence yet to be more sure the pair will reverse its down-trend, although the hammer, RSI and ADX are signalling the possibility of a bounce, pause or consolidation.

Eventually it is still probable the pair will continue lower in line with the dominant long-term bear trend, and a break below the current 1.8652 lows would probably lead to a continuation down to the S2 monthly pivot at 1.8410.

Aussie Fundamentally Sound

The Aussie has been supported by a rally in commodities, which has seen WTI Crude rise above $40/barrel and Iron Ore, the country’s number one resource, rise to above $60/tonne.

Commodities are a very important source of revenue for Australia.

Higher commodity prices are indicative of more demand for Aussie commodities and therefore more demand for the Australian Dollar, which is likely to rise due to the increase in demand.

A relatively strong housing market, reasonably low unemployment, and an economy which has adjusted well to being more services-orientated are just some of the reasons why AUD has recovered.

The Reserve Bank of Australia’s base lending rate of 2.0% is relatively high within the G10 (only lower than RBNZ) and is still a magnet for investors searching for interest on their savings or the carry trade.

In a recent note, Credit Suisse viewed current market expectations that the RBA would cut rates in 2016 as over-exaggerated, expecting the RBA to stay on hold instead.

Indeed, conviction that the RBA will remain on hold for the rest of the year appears to have gained as a result of recent data showing a fall in the unemployment rate from 6.0 to 5.8% in February.

Sterling meanwhile remains dogged by the threat of Brexit, with recent downward pressure coming from polls showing the vote likely to be extremely close run.

Economic Data

In the week ahead there is a dearth of Australian data, with only the House Price Index, on Tuesday 22, which rose 10.7% in the previous quarter.

Crude oil Inventories on Wednesday 23 could also impact on the Aussie.

For the UK there is inflation data, with Headline UK CPI (yoy) for February, forecast to come out at 0.4% from 0.3% previously.

The previous three prints were positive.

A surprise bump in inflation would be pound-supportive as it would increase the chance of the Bank of England raising interest rates, which would increase demand for pounds from investors seeking a higher interest rate for their money.

UK Public Sector Net Borrowing for February is expected to rise to 5.4bn from -11.8bn previously.