The fate of the Pound-to-Dollar over the next five days could be dictated by a duel of central bankers' words.

The US will witness speeches from no less than 11 of the 16 members of the Federal Reserve rate-setting committee, six of which will be voting members.

In the UK Bank Of England’s Carney and Broadbent will host the UK’s version of the Jackson Hole central banking conflab at London’s Fishmonger’s Hall – if there was a week to hear the clash of central bank rapiers then this is the one.

Currently both central banks are poised to hike rates and the expectation is for this central view to be supported by individual officials – if it is not, then there is a risk of one or other currency weakening.

Conversely confirmation that future hikes are likely, will push the respective currencies higher, assuming their strength does not cancel each other out.

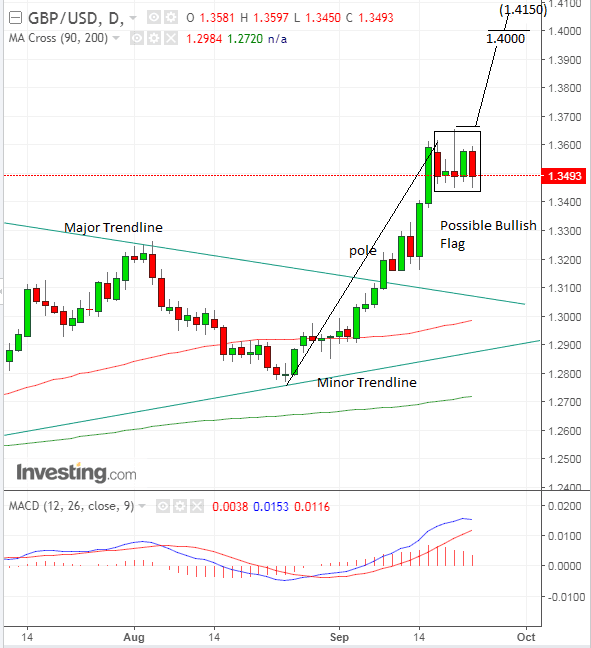

Indeed, looking at the chart of GBP/USD we note how this ‘cancelling-out’ effect, due to co-hawkishness, seems to have characterised last week’s range-bound mode, and look and feel of the chart suggests this may extend further in the week ahead.

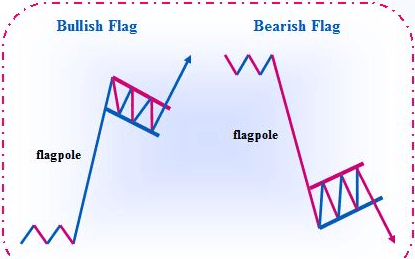

The current sideways move, coming as it does, after the steep rally from the late August lows, presents in its entirety a pattern which is similar to what technical analysts call a bullish flag.

These are – as the name suggests – signifiers of further uptrend, and it would suggest the Pound is set on appreciating versus the Dollar.

However, the look and feel of the pattern suggests that it may as yet be incomplete and the sideways move probably has further to unwind, thus we see a chance of CB talk this week jointly cancelling-out volatility due to sharing a similarly hawkish bias.

Eventually, the compelling flag pattern betokens a breakout and continuation of the uptrend higher, and such a move would probably be confirmed by a break above the 1.3658 highs – let’s say by a move above 1.3665 to be on the safe side.

Once underway the breakout move would be expected to reach its initial target at 1.4000.

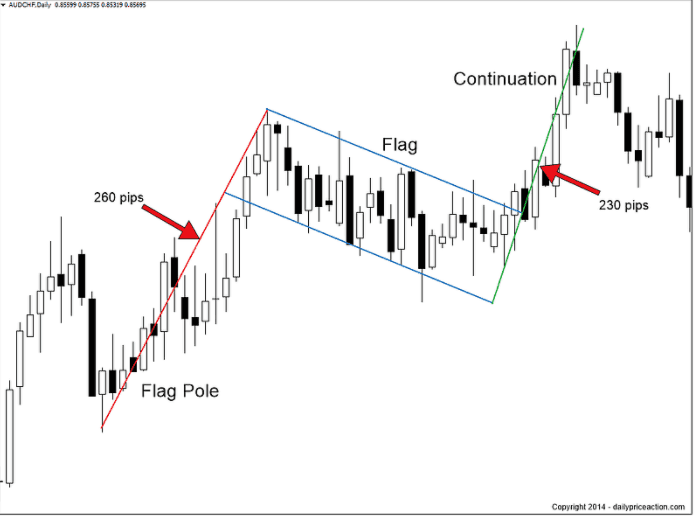

Flags generally move to a target established by measuring the length of the pole and extrapolating it higher from the point of breakout.

They can move as far as 100% of the length of the pole but the minimum reach is normally 61.8% of the length – which is the ratio of the golden mean, a mathematical formula which mysteriously describes many shapes and forms in nature and is used as a guide in financial markets.

A 61.8% move would reach 1.4150 but we have highlighted the 1.40 level as a minimum target since it is a psychologically significant round-number, and would be the obvious place for bullish traders to take profit.

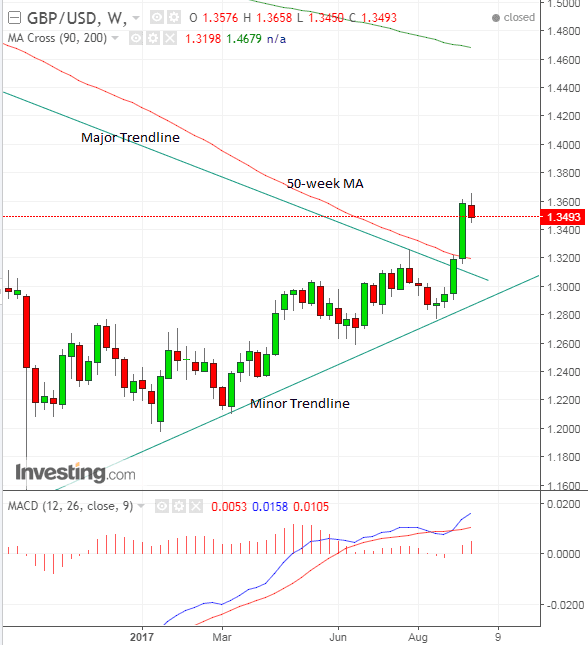

The overall outlook favours a continuation of the uptrend expecially after the recent breakout above the major trendline, which was an extremely bullish event, and indicates the trend is probably changing to a more bullish longer-term mode.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.

Data and Events for the Dollar

Despite moribund inflation the Federal Reserve reiterated its plan to raise interest rates three times in 2017, at the September Fed meeting last week, leading to a slight recovery in the Dollar.

With 11 Fed speakers scheduled to speak this week, including key Fed personnel: Dudley on Monday, Yellen on Tuesday and Fischer on Thursday, the market is expecting them to reaffirm their view that another rate hike is warranted this year as they are unlikely to have changed their view so soon after the meeting.

Any more concrete admissions of a hike will support the Dollar’s recovery.

Also relevant to the Fed is the release of its preferred gauge of inflation the Personal Consumption Expenditure metric on Friday, at 13.30 BST.

Canadian investment bank TD securities, expect a slight upwards surprise month-on-month of 0.2% rather than 0.1% from the consensus of economists.

Year-on-year PCE is stood at 1.4%. Ideally it needs to shift higher to warrant the Fed’s hawkish stance but whether that will happen now is debatable – as their view that inflation will catch up is more a medium-term expectation based on the tighter labour market.

There is much debate currently in the analyst community as to whether the Fed is right to just assume inflation will catch up and deserve the rate hike regime they are currently outlining.

There are those – including many Fed officials - who point to the extremely low level of unemployment as indicating wages must and will rise as employers find it increasingly difficult to source labour from the dwindling pool, which will eventually shunt up inflation.

However, the opposite argument is equally compelling, which is that globalisation, automation and the internet are longstanding changes to the global economy which have instituted a new inflation ‘paradigm’ leading to a lower new-normal rate of inflation internationally.

They also point to obstinate deflation in Japan against an unlikely backdrop of ferociously low unemployment and a populace with an engrained work ethic.

In a recent note CIBC make an interesting point about how there is now a gulf between online and offline retail inflation, with offline actually in a deflationary spiral, compared to online which continues rising, and this highlights the discounting effect of the internet.

“A relatively new “Digital Price Index” compiled by Adobe suggests that, within the online space itself, prices have been falling quicker than elsewhere as big players vie for market share. In other words, the cheap online prices have been getting even cheaper,” says CIBC’s Andrew Grantham.

Back to the hard data outlook for the coming week and the other main releases are as follows, on a day by day basis:

Tuesday, September 26: S&P Case-Schiller House Price Index at 14.00 BST. Consumer Confidence at 15.00 and New Home Sales at 15.00.

Wednesday, September 27: Durable and Core Durable Goods at 13.30. Pending Home Sales at 15.00.

Thursday, September 28: GDP, second estimate of Q2.

Friday, September 29: PCE at 13.30. Chicago PMI at 14.45 and Michigan Consumer Sentiment at 15.00.

Data and Events to Watch for the Pound

The fourth round of EU-UK Brexit negotiations commence on Monday, September 25.

The talks follow Prime Minister May’s Florence speech, with its 2-year transition and chief EU negotiator Michel Barnier’s moderately positive reaction to the speech, seems to be biased to supporting rather than undermining Sterling.

Negotiators are set to brief the press on the outcome of this round of talks on Thursday and the key for currency markets will be whether Barnier indicates he believes progress is being made.

The worst possible outcome for Sterling would be a disruptive Brexit - where negotiations fail to deliver a credible trading relationship between the EU and UK when the UK exits the Union in March 2019.

The first round of talks that see legacy issues and the practicalities of the exit dealt with must be cleared before talk of the trading relationship begins.

Also ahead, speeches by Bank Of England’s Mark Carney on Thursday and Ben Broadbent on Friday could provide potential focal points for Sterling traders.

The current market view is that the BOE is embarking on a tightening cycle with analysts now even pencilling in the likelihood of a November rate hike; and the speeches need to be read in light of that more hawkish backdrop.

Markets presently assign an 80% chance of a November rate rise.

Clearly an increase in hawkishness via stronger confirmation of a November rate move by either speechmaker would lead to fresh gains for the Pound, which is positively correlated to interest rates.

Data-wise, the next most significant release could be the Current Account for Q2, at 9.30 BST on Wednesday, September 27, which is forecast to show a slight reduction in the deficit to -15.8bn from -16bn in Q1.

A deeper contraction could help the Pound.

At the same time as the Current Account data is released Business Investment data will also be released for Q2 and will offer a further insight into the strength and resilience of the economy.