The GBP/USD exchange rate remains pointed firmly lower as we approach year-end, and the structure of the underlying foreign exchange market suggests we can expect futher losses moving forward.

A dwindling supply of dollars in international FX markets, due to falling FX reserves, is providing underpinning support for the Dollar into the end of the year says Societe Generale's FX Strategist Kit Juckes.

"Lower oil prices and falling global FX reserves have reduced the availability of dollars in global money markets in 2016. Demand from those with dollar liabilities, especially those with debt to roll over, is strong," says Juckes.

The lack of supply and increased demand is putting upwards pressure on the Dollar.

"And yet, if the strains reflect stronger demand for and decreased supply of dollars in markets, intuitively, it's bound to be dollar-supportive to some degree," says the strategist.

The imbalance is likely to be reflected in a rise in the Dollar and consequenctly a fall in the EUR/USD rate, especially - however, the same is likely for GBP/EUR given the Pound's recent underperformance versus the Euro.

"The bottom line from our perspective - we see plentiful evidence of tightness in the supply/demand for dollars, and this increases the risk of overshoot on the upside for both US yields and the dollar, particularly around sensitive times like quarter and year-end. I also observe that the 10yr real yield differentials between the US and Europe, and between the UK and the US, are moving out to new highs for this cycle. It all points to dollar strength into the year-end," concludes Juckes.

Latest Pound / US Dollar Exchange Rates

| Live: 1.3242▼ -0.15%12 Month Best:1.3867 |

*Your Bank's Retail Rate

| 1.2791 - 1.2844 |

**Independent Specialist | 1.3056 - 1.3109 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Dollar Supported as US Consumer Confidence at 15-year High, GBP/USD to Continue Lower

The Dollar strengthened against the Pound on Tuesday after US Consumer Confidence peaked in December.

Conference Board Consumer Confidence came out at 113.7 when it had been forecast to correct back to 108.5.

The strong result, coupled with unexpectedly good data for the Richmond Fed Manufacturing Index, which rose to 8 versus the 4 expected, and the Dallas Manufacturing Index, which came out at 15.5 when a 10.2 had been forecast, further supported the Dollar.

The strong data has led to a weakening of the Pound against the Dollar.

GBP/USD has pushed down to 1.2233 at the time of writing and looks poised to extend the existing short-term downtrend which began at the December 6 highs.

Having breached support at 1.2300, Lloyds Commercial Banking now see the pair as likely to continue down to 1.2000-1.2080.

Our own studies leave us a little more cautious and see a likely continuation to 1.2100 confirmed by the exchange rate breaking below the 1.2200 level.

MACD is under the zero-line signaling the short-term trend is now down and has crossed its signal line providing another bearish signal.

An Elliot Wave analysis of the pair (see chart below) suggests the pair has lower to go, in what may be a wave 5 down, in the direction of the long-term downtrend.

If so, then the pair could continue down to the vicinity of the October lows in the 1.14s.

According to Ellioticians at J P Morgan, the pair completed a wave 3 at the October lows.

It was then seen as likely to rise in a wave 4 to a target at the 1.2650 – 1.2800 level highs, which it appears to have now done, having ended the last move up at 1.2770.

The move down since then is either still part of wave 4 or a new bearish wave 5 down.

Trump's Policies to Boost Dollar in 2017

The Dollar's current rally is expected to continue during 2017, as the implementation of Donald Trump's new policy agenda is likely to be positive for the currency.

Trump's promise to force corporates to repatriate an estimated two trillion in overseas earnings is likely to see a surge in demand for the dollar based on the previous period of repatriation in the 1990s when the Dollar rose significantly from the inflows.

Any concerns that House Republicans might attempt to curb Trump's policies have been deterred by their seeming acceptance of one of his trade initiatives called "Border Adjust", which would provide tax relief to exporters whilst adding a tax to imports.

Border Adjust alone is expected to lead to a 10-15% rise in the Dollar as it seeks to offset the increased demand according to Morgan Stanley.

These policies alone are expected to push up the Dollar, without even accounting for the impact of his reflationary fiscal spending policies, which will increase inflation, interest rates and therefore the value of the Dollar, due to both Fed rate hikes and rising yields.

Could Potential Downturn in Housing Impact on Dollar?

Not all analysts see the Dollar's strong uptrend as a one-way street.

Some, like Nordea's Aurelija Augulyte, see the potential for an upset in 2017.

Augulyte forecasts a slowdown in the US property market in 2017 due to rising mortgage rates as credit becomes more expensive.

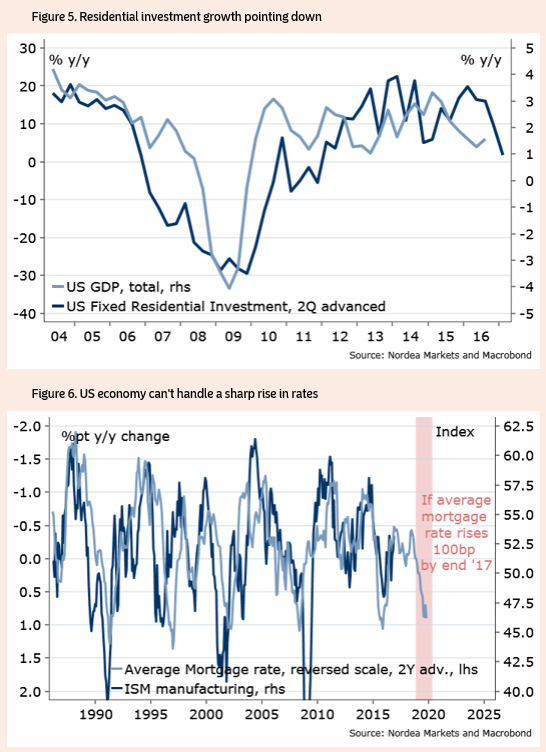

Since Housing is a leading indicator for the US economy the Nordea analysts sees a high probability that the downturn in housing could be an early indicator of a deeper contraction and the dreaded 'r' word.

"Recession? The US economic cycle is mature, so the lagging labour market indicators are of little added value.

"Housing market is key, residential investment is one of the best leading indicators for the US economy.

"The recent rise in yields will dampen the housing market activity.

"In fact, it doesn’t take much – just another 100bp rise in mortgage rates, and we have a US recession? (Figure 6)

"Yes, I think in some form or shape, we will have a word “recession” as a theme and driver during 2017," says Augulyte.

Figure 6 below shows that only another 1.0% rise in mortgage rates will start to dampen the housing sector. and since the Federal Reserve has said it will be increasing interest rates by three 0.25% rate hikes, which equates to 0.75% in total the tipping point for the market has almost been reached.

Bearing in mind the Federal Reserve expects to be increasing interest rates by three 0.25% rate hikes, which equates to 0.75% in total, the tipping point for the market to dampen will almost be reached by the end of 2017.

Apart from the decline in Residential Investment (Figure 5), however, there are few other early signs suggesting a slowdown in the property market is already beginning.

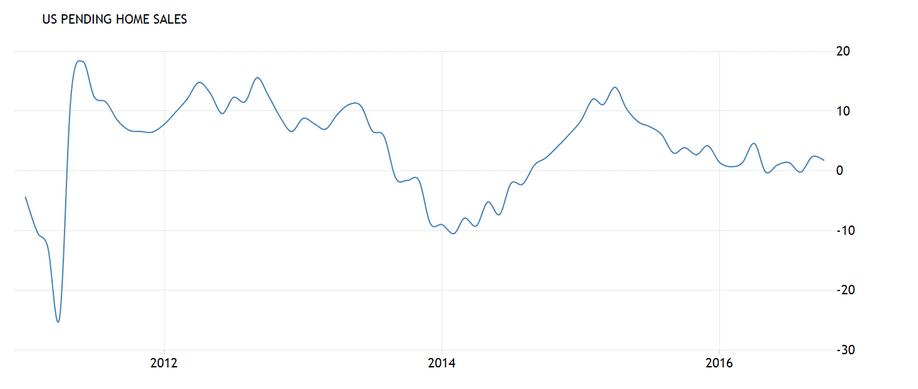

Pending Home Sales, due for release later today, have been trapped in a wide range since the great depression, and most other indicators have been rising gradually.

The S&P Case-Schiller House Price Index has risen slowly and steadily and recent data out on Tuesday showed another 0.1% rise in November.

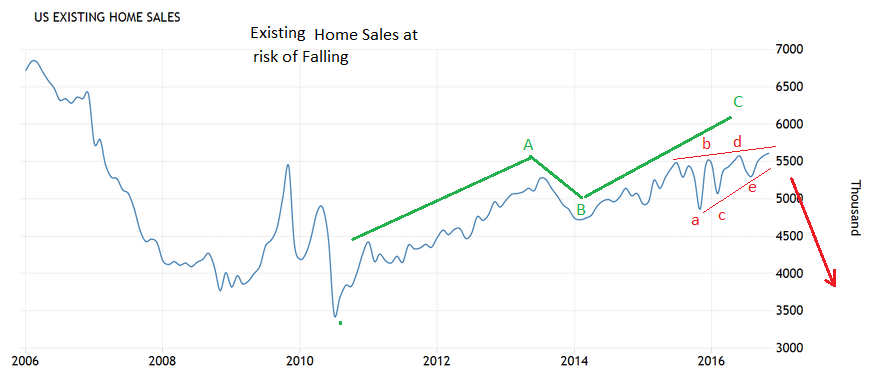

The only other sign of weakness we have noticed is the 10-year chart of Existing Home Sales, which is showing what looks like an Elliot ending diagonal pattern forming at the end of a measured move, otherwise known as a zig-zag, or Elliot ABC correction.

This ending diagonal is an Elliot Wave pattern which forms at the end of major moves and is usually followed by a surprisingly steep sell-off.

This ending diagonal on Existing Home Sales (See second chart below) looks to be almost complete as it has formed 5 internal waves a,b,c,d and e, which is the minimum number for completion.

Elliot Wave Theory is applicable to any data set, not just financial prices or rates, as it is a graphical representation of social mood which can be reflected by data such as House sales, as well as actual price data.