Our studies confirm the charts are bearish on the GBP/USD exchange rate ahead of Chancellor Hammond’s Autumn Budget Statement.

GBP is quoted at 1.2343 at the time of writing, down from the 1.2353 where it closed the previous week.

The week starting November 14 and ending November 15 was the first notable down week since October and confirms a shift in momentum away from the Pound.

The technical outlook does not favour the Pound, which could imply the Budget will be a disappointment.

GBP/USD has formed a head and shoulders top reversal pattern which is clearly visible on the four-hour chart.

The is a bearish pattern which signifies the pair is about to change the direction in which it is trading in.

The exchange rate has already broken below the neckline and has now formed a typical characteristic of these patterns, which is the ‘return move’ following the initial break.

This return move is a temporary move back up into the neckline before ‘air kissing’ it goodbye before the final move lower.

The MACD indicator is declining on the formation of the head and the right shoulder of the pattern, showing declining momentum as the pattern formed, which is typical confirmatory sign for a head and shoulders top.

A break below the 1.2300 lows would confirm more downside to an initial target at 1.2175, followed then by 1.2100.

Analyst Ipek Ozkardeskaya at London Capital Group notes the GBPUSD broke below the five-week ascending channel base.

"GBP-shorts are in charge of the market before the UK’s Autumn Statement due on Wednesday. The downside pressures are expected to gather momentum below 1.2300, as decent 1.2300-puts are in play at the first part of the week."

Ozkardeskaya notes resistance at 1.2389 (minor 23.6% retracement on Nov 18st to Nov 18th decline), before 1.2443 (major 38.2% retrace) and 1.2460 (200-hour moving average).

Latest Pound / US Dollar Exchange Rates

| Live: 1.3455▲ + 0.08%12 Month Best:1.3867 |

*Your Bank's Retail Rate

| 1.2998 - 1.3052 |

**Independent Specialist | 1.3267 - 1.3321 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

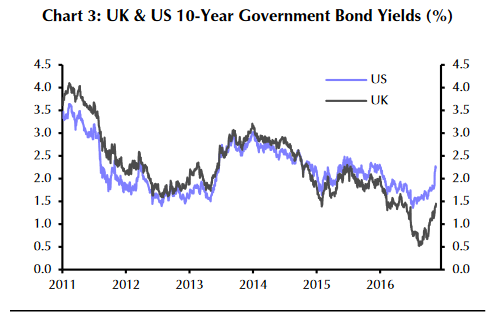

Yeilds Moving in Dollar's Favour

Since the election of Donald Trump the difference between UK 10-year and US 10-year bond yields has narrowed.

Yields are a bit like interest you earn on a loan, and investors generally prefer a higher return or yield over a lower yield.

The narrowing difference has reduced the advantage to the investor holding Dollars, and thus upside in the Dollar vs the pound.

According to Capital Economics’ Paul Hollingsworth the GBP/USD should now be close to ‘fair value’ as indicated by relative interest rate differentials.

“The Pound is now at a level that is broadly consistent with relative interest rate expectations, with no sign of a 'Brexit premium'," he said.

Autumn Statement Ahead

In the week ahead the main risk to this equilibrium is the Chancellor’s Autumn statement, delivered on Wednesday, November 23.

The focus will be on the amount of fiscal stimulus the government is willing to spend, which if substantially increased is likely to push up interest rates, favouring the pound, as it will take the pressure off the Bank of England to print money and use that as stimulus instead.

Talk of the government’s plans to expand stimulus may have been a little hyped, however, according to Hollingsworth, who says that ‘outright loosening’ now seems unlikely:

“All eyes are now on the Chancellor, who delivers his first fiscal set piece with the Autumn Statement on Wednesday.

“He will be constrained somewhat by recent poor borrowing numbers and a disappointing set of economic forecasts.

“Accordingly, we expect fiscal policy to be less tight than the current plans, rather than providing an outright loosening.”

Hammond has said the Government remains constrained by the country's huge debt pile and with economic growth remaining robust he will most likely opt for a conservative budget.

Expectations for a Trump-style fiscal boost are therefore likely to be misplaced.

In all, this should be a business-as-usual budget from a Pound Sterling perspective.

The government’s latest borrowing figures out in Tuesday, November 22 – the day before the budget - could provide a hint as to how generous Chancellor Hammond is willing to be.

Data to Watch

Economists estimate a rise of 5.6bn borrowing in Net Borrowing by the government in October, from a previous 10.1bn.

A rise much above that will probably weigh on sterling as it will reduce the Chancellor’s stomach to open up Treasury.

Investors are now almost 100% certain that the Federal Reserve will increase US base interest rates in December, so unless those expectations are drastically lowered, the dollar should remain relatively stable, notwithstanding probable volatility from the ‘Thanksgiving Effect’.

Thanksgiving Effect

On Thursday, November 24 it is Thanksgiving Day in the US, a national holiday.

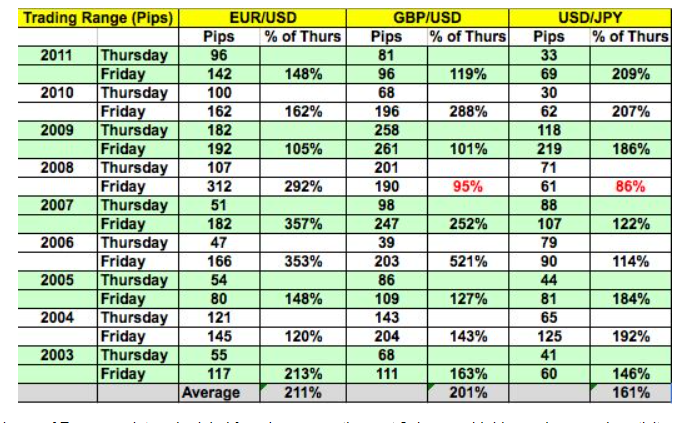

Research conducted by Kathy Lien of BK Asset Management, indicates that dollar pairs often experience much wider-than-average trading ranges on the day after Thanksgiving.

So common is the phenomenon, that it has led to a strategy called the ‘Thanksgiving Effect’.

“While many U.S. traders also take Friday off, the intraday range of the EUR/USD, GBP/USD and USD/JPY tends to expand significantly on the day after Thanksgiving.

“Some traders are back and the low liquidity exacerbates the volatility in the FX market,” says Kathy Lien.

She goes on to provide empirical evidence that the increase in volatility is quite marked:

“The following table shows that on average since 2003, the trading ranges for the EUR/USD and GBP/USD increases 200% the day after Thanksgiving. The impact on USD/JPY is less significant but we still see similar trading activity.”

We advise traders to adopt a breakout strategy, and will be watching the tight ranges on Thanksgiving day and providing guidance on how to position for the volatility on the day after nearer the time.

Week Ahead for US Dollar

This week will be dominated by continuing speculation about potential key appointments to Donald Trump’s new administration.

Other than that Existing Home Sales are out at 15.00 (GMT) on Tuesday, November 22, and are expected to show a reduction to 5.42 million from 5.47m.

Wednesday, November 23 sees the release of Durable Goods Orders at 13.30, with Core Orders forecast to rise 0.2% mom in October from 0.1% in the previous month.

“October’s durable goods report (Wednesday) is likely to reveal a big surge in orders, albeit mostly due to a spike in the notoriously volatile commercial aircraft component,” said Capital Economics’ Paul Ashworth.

New Home Sales are released on the same day and are expected to show a rise of 590k in October, from 593k previously.

Crude Oil Inventories, out at 15.30 could also influence the dollar on Wednesday, although many traders may have already taken money off the table before the Thanksgiving Holiday on Thursday.

Data for the Pound This Week

On the hard data front, the main release for the pound in the week ahead is Q3 GDP.

Preliminary estimates had it at a healthy 0.5% QoQ and unless the second estimate seriously disappoints we are unlikely to see much movement from this release.

Tuesday, November 22 sees the release of several lower tier releases, including Public Sector Borrowing, which is forecast to show -1.6bn net borrowing, followed by November data from the Consortium of British Industry, measuring Industrial Trends.