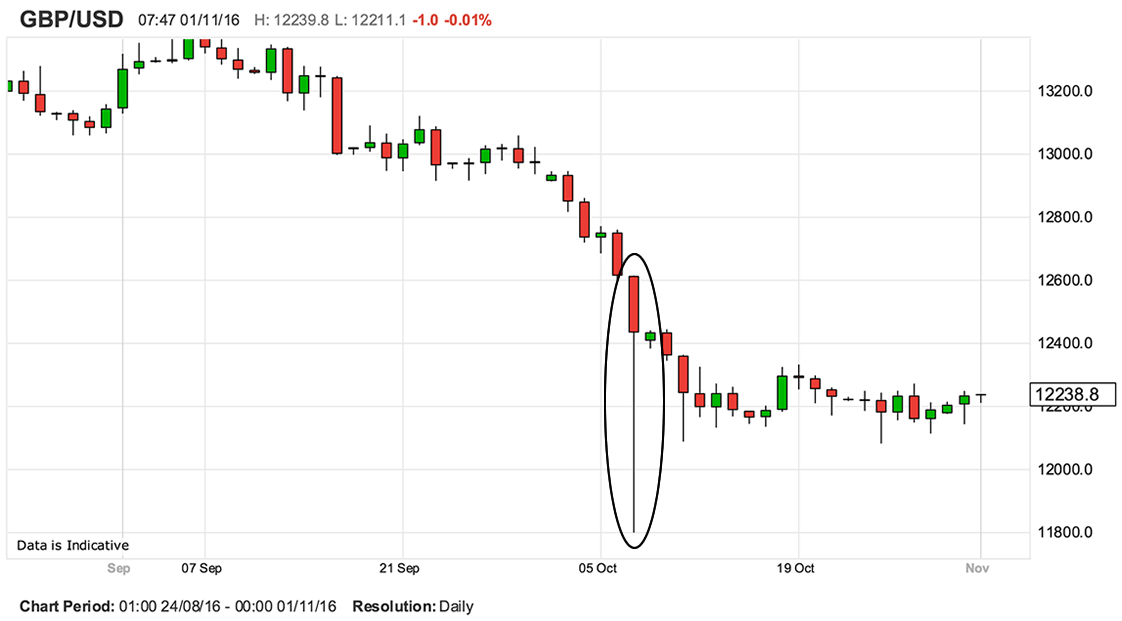

GBP/USD edges higher into the new month and we believe there remains the prospect of further gains over coming days.

GBP/USD trades within a familiar range at the start of the new month with a late kick higher on October 31st taking the currency pairing to 1.2238.

The Pound recovered across the board partly on news the Bank of England's Governor Mark Carney will stay in his role until 2019 which should provide some stability during the Brexit negotiation process.

We believe the supportive fundamental picture provided by the Carney decision chimes nicely with our technical studies which advocate for a recovery in GBP/USD.

The long exhaustion bar, circled in black, would typically suggests the downtrend is over – at least temporarily - and a bounce is due.

A move above the range highs at 1.2350, is expected, with a continuation from there to a target at 1.2500.

For confirmation of more downside, a break below the spike lows at 1.1450 would be necessary, with a downside target at 1.1400.

With hard-Brexit being baked into Sterling we believe the trigger required for such a break lower will be hard to pull.

J P Morgan see the pair as likely to rebound higher to between 1.2600 and 1.2850.

Using Elliot Wave analysis, which is a type of cycle analysis, J P Morgan expect a correction higher up to the aforesaid band in a wave 4, before moving lower again in a final wave 5 down.

Elliot Waves are composed of 5 waves, with 1,3 and 5 in the direction of the trend and 2 and 4 against the trend and corrective.

Once the 5-wave cycle has ended the pair will make a much larger correction against the dominant trend, as the cycle turns.

Latest Pound / US Dollar Exchange Rates

| Live: 1.3476▼ -0.03%12 Month Best:1.3867 |

*Your Bank's Retail Rate

| 1.3018 - 1.3072 |

**Independent Specialist | 1.3287 - 1.3341 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

The Big Drivers for the Week: PMIs, Bank of England and High Court Challenge to Article 50

The key fundamental for the Pound is whether the Bank Of England (BOE) cuts interest rates any lower at its meeting on Thursday.

Markets appear to be attributing a roughly 50/50 chance to the possibility.

What will also be of interest are the changes made to growth and inflation forecasts in the Bank's Quarterly Inflation Report.

The Bank's forecasts could well hint at future policy decisions, particularly if they believe inflation will rise faster than previously anticipated.

The Bank will not tolerate inflation much higher than 2% and is expected to raise interest rates should this level be threatened.

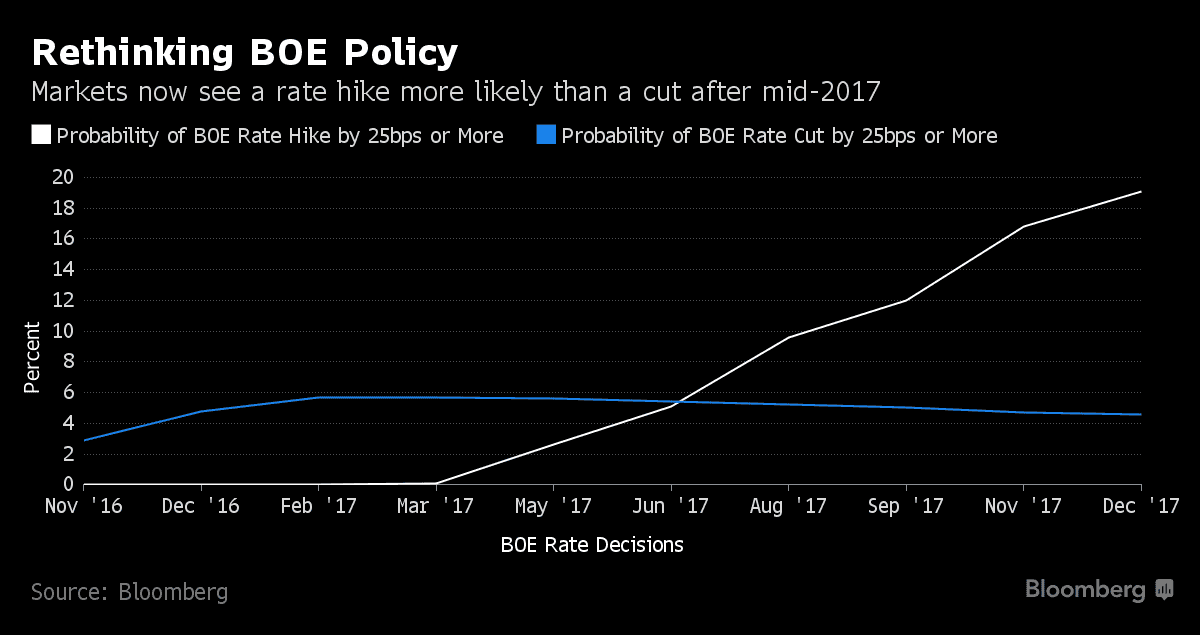

It is because of rising inflation expectations that markets are starting to price in higher interest rates in the future:

Overnight index swaps indicate that there is now more of a chance of an interest rate rise than a rate cut in 2017.

Rising interest rates are deemed to be supportive of a currency in that they attract capital inflows as global investors seek out yield. Clarity on Brexit, combined with rising interest rates, will be the ultimate catalyst for a longer-term and more sustainable Pound recovery.

Traders are re-evaluating how long monetary policy policy will remain accommodative following better-than-forecast economic growth data and BoE Governor Mark Carney’s suggestion two days ago that the prospect of faster inflation is diminishing the case for easing.

Carney also said the Bank would consider the impact of future decisions on the already weak Pound.

This suggests the BoE may hold fire for fear of weakening the Pound, which would make imports more expensive, and risk excessive inflation.

The other major theme for Sterling relates to the current high court challenge to the government’s authority to trigger Article 50 on its own without the agreement of parliament.

The failure of a similar challenge in a high court in Belfast is thought to have set a precedent which the London court is likely to follow.

If the challenge is unsuccessful the pound will fall; if not it will rally strongly.

It is not clear when the London court will make its decision.

The main data releases in the week ahead are the trio of October Purchasing Manager Indices (PMI) releases.

Tuesday, November 1 sees release of the final estimate for Manufacturing PMI for October at 10.30 GMT, which is expected to come out at 54.5 from a preliminary estimate of 55.4.

Construction PMI is out on Wednesday at 10.30 (GMT) and is forecast to moderate to 51.8 from 52.3.

Thursday sees the release of Services PMI at 10.30 (GMT), which is forecast to come out at 52.1 from a preliminary estimate of 52.6.

Data Ahead for the Dollar

The first major release of the week is ISM Manufacturing in October, at 15.00 (GMT) on Monday, which is forecast to come out at 51.7 from 51.5 previously.

This and Non-Farm payrolls at the end of the week are expected to be “constructive” and to, “confirm solid growth fundamentals are in place,” according to economists at TD Securities.

This is followed by the Federal Reserve's interest rate decision (FOMC) on Wednesday at 19.00 (GMT), with only a very low 7.2% probability of a rise being agreed at the meeting, mainly due to the proximity of the US presidential election.

We think the market is being complacent and that recent strong GDP data could have increased the odds of a surprise rate hike at the November meeting.

If not then the Fed is highly likely to at least ‘pave the way’ in its statement, for a hike in December which markets are currently pricing in as 78% probable.

ISM Non-Manufacturing PMI for October is set to be released on Thursday at 15.00 (GMT), and is expected to show a dip to 56.0 from 57.1 previously.

Another big release at the end of the week is Non-Farm Payrolls at 13.30 (GMT) on Friday November 4 , with analysts expecting a rise of 175k in October from 156k previously.

The Unemployment Rate, released at the same time, is forecast to fall to 4.9% from 5.0% in October.

With expectations for a December interest rate rise now largely priced into the US Dollar there is a risk that this week's reading does not trigger the kind of big moves in the USD we have seen in the past.