The USD will look to add further gains to the recovery; but it still has a lot of ground to cover before reclaiming all the ground lost at the start of February.

The US dollar dipped violently at the start of February on fears that the US was headed for a new recession and the US Federal Reserve would shy away from raising interest rates in 2016.

These fears hav ultimately proved unfounded and were symptomatic of a flighty market, one that has been severely psychologically influenced by the stock market sell-off.

“Fears of a recession have diminished recently as some economic data have been convincing. Industrial production, retail sales and the labour market figures are worth highlighting,” says Viola Julien at Helaba Research in Frankfurt.

The US Federal Reserve meanwhile maintains a confident tone and while four interest rates are certainly not likely in 2016, further rises are likely to keep the USD bid.

Data is likely to become the subject of even more intense focus as markets settle down and return to fundamentals.

Latest Pound / US Dollar Exchange Rates

| Live: 1.3358▼ -0.24%12 Month Best:1.3867 |

*Your Bank's Retail Rate

| 1.2903 - 1.2957 |

**Independent Specialist | 1.3171 - 1.3224 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Dollar buying interest first became evident on the 11th of February and since then we have seen moves higher in the US dollar index (DXY).

The dollar index is a composite of all the major US dollar exchange rate pairings and is the best gauge on sentiment towards the USD.

We have however witnessed the uptrend stall of late as dollar-buying interest struggles to take the index through the 97.00 with a breach failing to occur on four occasions.

Data will need to be unambiguously positive this week for the dollar to retake its status of ‘king of the currencies.’

The Big Numbers that will Make or Break the Dollar Comeback

The week starts with Manufacturing PMI, which because it is the preliminary estimate, is likely to be even more closely watched.

After the weak ISM data sparked recessionary fears at the start of February, investors will be looking to Manufacturing PMI for reassurance that the economy is actually not as bad as thought.

On Tuesday the main release is Consumer Confidence in February which is expected to slide to 97.5 from 98.1. This is followed by housing data in the form of the S&P Case-Schiller Composite-20 and Existing Home Sales in January (mom), which is forecast to show a recovery of 0.7%.

Services PMI for February heads the line-up on Wednesday, followed by Crude Oil Inventories, New Home Sales (expected to drop -3.5%) and MBA Mortgage Applications.

On Thursday the calendar is dominated by Durable Goods Orders, with Durable’s in January expected to show a 3.0% rise from -5.0% previously and Durables Ex Transport to come out at -0.3% from -3.0% previously.

According to TD Securities an even higher reading may be possible due to new orders with aircraft manufacturer Boeing.

“Boeing orders are expected to bias the headline durable goods report higher, though a weaker forecasted outturn for ex-transport and the core component (which ultimately matters for the economy) will dent any optimistic interpretation.

Helaba's Julien is also watching Boeing: "The pick-up in orders at Boeing bodes well for a rise and the consensus estimate could be exceeded. However, it is questionable whether the surprisingly sharp fall of the previous month can be reversed."

Finally, on Friday there is the second estimate from fourth quarter GDP. Preliminary estimates came out at 0.7%, however, analysts expectations are that it might fall to 0.3%.

"Confidence in the strength of the US economy will be put to the test again at the end of this week as another downwards revision to Q4 growth is foreseeable. Even a virtual stagnation in economic activity cannot be ruled out," says Julien.

GBP/USD Forecast

The GBPUSD pair is consolidating just above the 1.4000 level.

The dominant trade remains down, and the pair will probably go lower, in line with this trend.

A break below the 1.4080 lows will probably lead to a move down to 1.4000, where support from the round-number effect at that level will probably break its fall.

A further fall below the S1 Monthly Pivot at 1.3946 – confirmed by a move below 1.3900, would probably lead to a further move lower, to the next major support level at the S2 pivot at 1.3650.

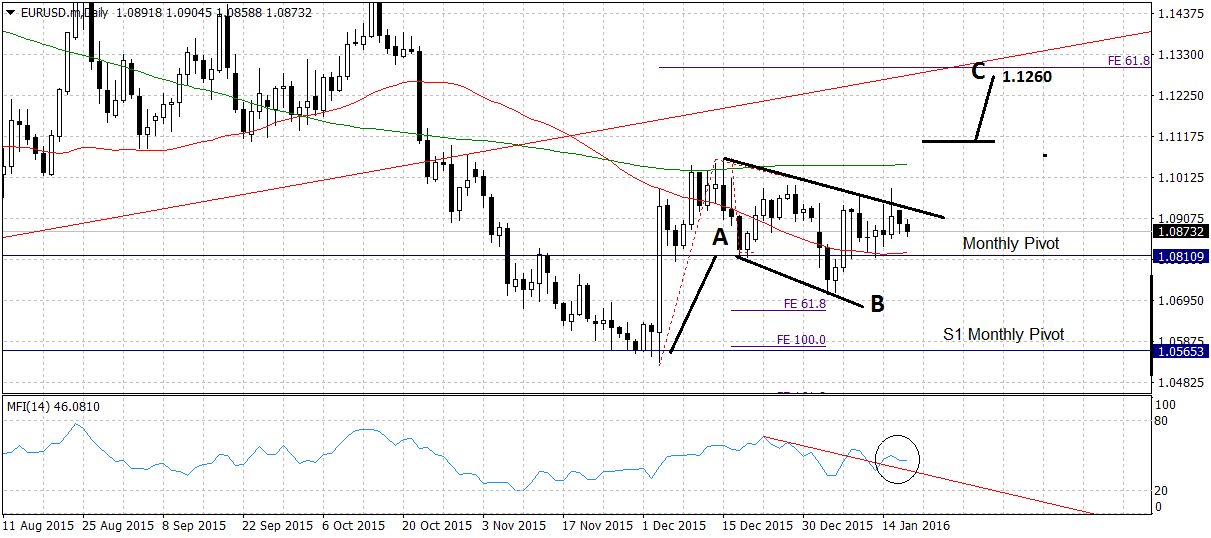

EUR/USD Forecast

EUR/USD has completed an A-B-C correction from off the December lows.

It rolled over on February 11 and then sold off for 5 days in a row, reaching lows of 1.1070.

It has found support on the R2 Monthly Pivot where it is currently consolidating.

If there is a re-break below the 1.1070 lows, however, that would confirm the onset of more downside for me, leading to a move down to a target at the 200-day MA situated at 1.1027.

US Federal Reserve + Interest Expectations Remain in the Driving Seat

The current major themes governing the dollar are mainly focused on whether and by how much the Federal Reserve is going to increase the Fed’s Funds rate.

The release of the minutes of the January Fed meeting increased the chances that the Fed might raise rates in November as measured by the Fed’s Fund’s Futures which before the release were estimating the probability at 0.0%, but afterwards the chance had risen to 0.25%.

Better-than-expected Industrial and Manufacturing Production in January, after the sectors had seen a recent trough, showed a 0.9% rise from -0.7% in the month before.

This and continued positive labour and wage data contributed to the more optimistic outlook.

Add to this Friday’s flat inflation data (markets had been expecting a decline) and many investors are starting to believe the Fed may in fact go ahead with further tightening.

The Fed meeting minutes highlighted how the Fed would now be closely monitoring the impact of Global economic changes and Commodity market’s on the US economy.

Currently there is no observable pass-through to the domestic economy yet – only the fear of impact.