Above: President Donald Trump monitors U.S. military operations in Venezuela, from Mar-a-Lago Club in Palm Beach, Florida, on Saturday, January 3, 2026. (Official White House Photo by Molly Riley).

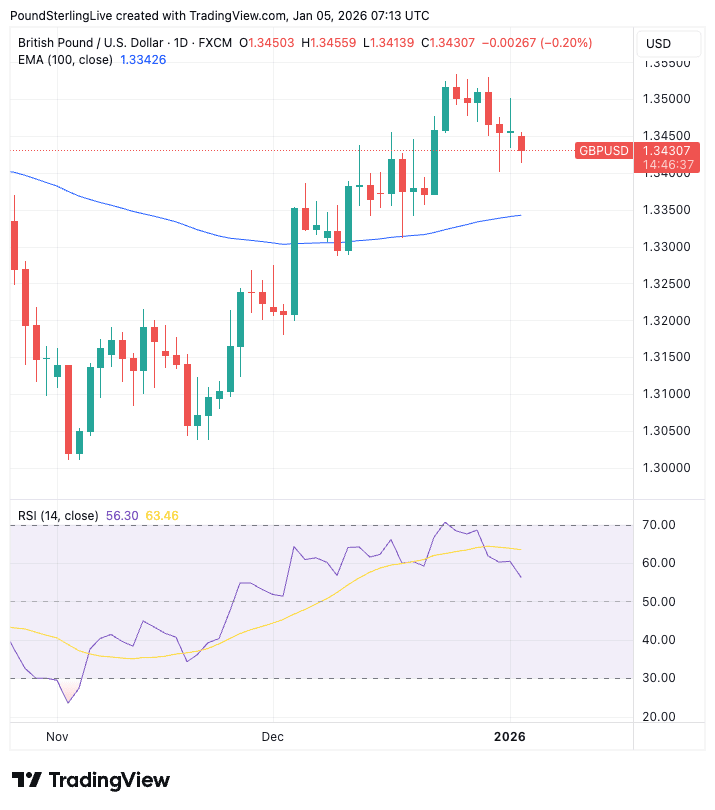

The British pound is pulling back against the dollar following a strong year-end lift.

The pound to dollar exchange rate (GBP/USD) retreats further from its Christmas Eve high of 1.3533, testing 1.3435 on Monday.

We note that some FX market commentators are saying the move is consistent with a stronger dollar in the wake of recent U.S. actions in Venezuela, and subsequent threats on Greenland, Colombia and Iran.

Analysts say this is creating tensions in FX markets that tend to support the dollar, the go-to currency when traders are nervous.

However, that claim is undermined by rising stock markets: a true 'risk off' event would see stocks falling sharply at the start of the new week in response to U.S. President Donald Trump's muscular foreign policy moves.

Given this, we are cautious of the idea that GBP/USD's pullback is purely linked to geopolitics and instead think we're watching a technically-driven paring of the late-2026 rally.

This is the natural pullback to the rally that needs further room to extend. The Relative Strength Index (RSI) on the GBP/USD's daily chart (see lower panel) rose to as high as 70 when GBP/USD peaked at 1.3533 in Christmas trade, the point at which the indicator reaches overbought.

The RSI is a mean-reverting indicator, meaning that it will inevitably turn lower once readings of 70 and above are reached. This is achieved via the exchange rate exiting its uptrend and either turning sideways or going lower.

This is playing out, and we would view a move back down to the 100-day exponential moving average (EMA) at 1.3342 as a potential outcome in the coming days.

There's nothing to bother sterling on the UK economic calendar this week; however, we do have some important U.S. data to contend with.

Monday brings the ISM manufacturing PMI release, which should shed light on how the sector fared in December. Here, another downbeat sub-50 reading is expected, consistent with the view that the economy continued to cool into year-end.

✳️ Secure today's exchange rate for a future payment. You may also book an order to trigger your purchase when your ideal rate is achieved. Learn more.

ISM's services PMI is due Wednesday, and here the news is expected to be more constructive with a reading of 52.3 expected, a level consistent with expansion.

However, the PMI's employment sub-index could be the more important reading on the day as it will offer fresh evidence of a slowing U.S. labour market, which would encourage traders to raise expectations for more rate cuts at the Federal Reserve.

This would, all else equal, weigh on the dollar.

Also on Wednesday are JOLTS job openings figures, another important indicator of U.S. labour market health, where a slowdown from 7.67M to 7.73M is expected for November.

Image courtesy of Brown Brothers Harriman.

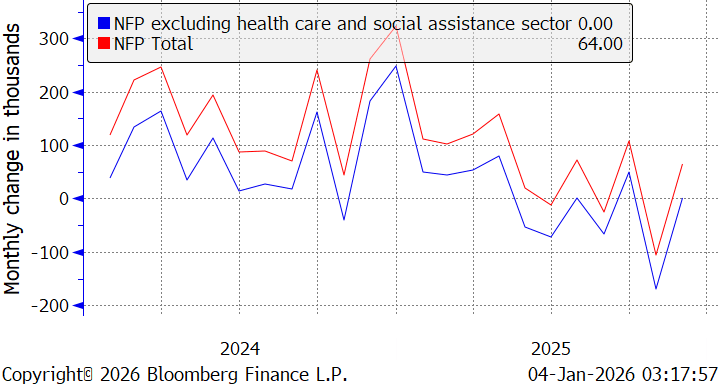

The big event of the week comes Friday when the non-farm payroll employment report is released. Here, 57K jobs are expected to have been created in December, confirming a steady deceleration (as above chart shows).

Anything less and the dollar falls as Fed rate cut bets ramp up, anything higher and the dollar extends its January recovery.

"The significance lies less in the headline job gains, and more in the sector generating them. In November, virtually all job gains came from the non-cyclical health care and social assistance sector, a pattern that has historically signalled an impending labour market slowdown," says Elias Haddad, Head of Global Markets Strategy at Brown Brothers Harriman.