Is the New Zealand Dollar's negative response to expectations the RBNZ's mandate will be changed by the new Government overdone, or are they warranted?

In the run-up to and after the New Zealand general election in October the New Zealand Dollar fell heavily due to fears about how the policies of some of the parties would impact on the economy and the way the central bank operates.

The Labour party included proposals to shift the Reserve Bank of New Zealand's mandate to focus on employment which implies interest rates would stay lower for longer in order to achieve optimal employment levels.

Thew New Zealand Dollar has long enjoyed the support of the high interest rates set at the RBNZ relative to other developed nation - the advantage encourages a flow of funds into the country from investors seeking higher yield. That this advantage could be threatened by changes to the RBNZ's mandate weighed on the currency.

Of course, the Labour party now leads the country in coalition with New Zealand First and the Green party, a combination which analysts had thought was the worst possible outcome for the Kiwi. And, the new Government appears intent intent on sticking to their pledge to alter the RBNZ's mandate.

And the currency fell as a result: before the election, the Pound could buy 1.84 Kiwi Dollars; after, it could buy significantly more at 1.94 - reflecting a substantial depreciation in NZD.

How Negative are Potential Changes to RBNZ Mandate for the Kiwi?

Kyle Uerata, an analyst at ANZ, is rather sceptical about the extent to which these changes will impact on the currency.

By not changing his forecasts for the NZD in his latest assessment of the currency, he suggests they will only have a marginal effect.

Most central banks only need to be concerned with managing inflation but the policies of the new government have added the requirement to foster 'full employment' to the RBNZ's job 'spec'.

Low interest rates tend to be more 'jobs-friendly' since they encourage borrowing, spending and investing, and these lead to greater job creation, therefore, it is logical to assume this new aspect to the RBNZ's mandate is more likely to keep interest rates lower for longer, thus dampening the Kiwi in the process.

ANZ's Uerata, however, suggests that whilst broadly true the real picture is complicated by several factors.

Firstly, the RBNZ already has to take employment into consideration in deciding its policy strategy, because employment determines how much 'slack' there is in the economy and that is a variable used in the decision-making on interest rates.

When there is a lot of 'slack' it means a lot of people are unemployed and the central bank traditionally keeps interest rates low, in order to encourage more job-creation.

However, when there is little 'slack' in the economy, which is basically when more people have jobs, inflation tends to be higher because everyone has more money and spends more, and in response to this, the central bank tends to raise interest rates.

Uerata argues, therefore, that by mandating for 'full employment' the RBNZ will only be highlighting a function it already carries out viz: the monitoring of, and acting in accordance with, the state of the labour market.

"In itself, we don’t see the introduction of an employment mandate as likely to dramatically change the way monetary policy is conducted," says ANZ.

When is Employment 'Full'?

In addition to these theoretical arguments, ANZ also makes an attempt to assess the state of the labour market at the moment and how far away it is from 'full employment'.

Clearly, if the labour market has a long way to go before reaching what would be described as 'full employment' the implication is that the RBNZ will keep interest rates lower for longer in order for help foster more jobs, and this will further devalue the Kiwi.

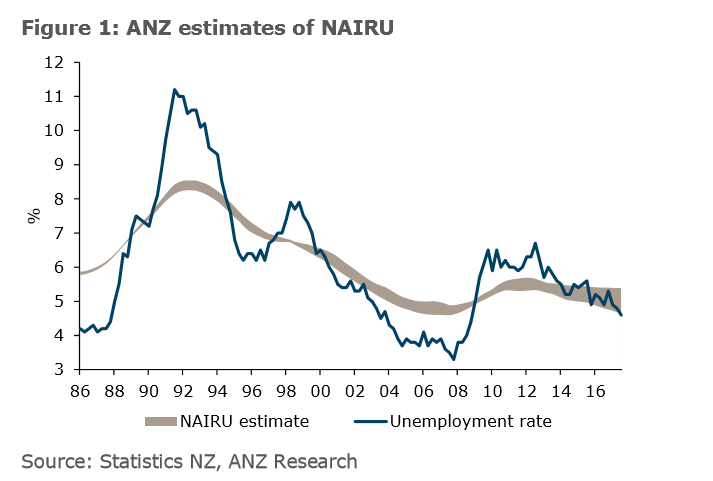

ANZ uses a method to determine the state of the labour market called the level of 'NAIRU' which stands for Non-accelerating inflation rate of unemployment - or the tipping point where lower unemployment will push up inflation.

ANZ argue that the RBNZ probably use NAIRU in their estimates for 'full employment' as they are primarily concerned with price stability and NAIRU reflects the interaction between jobs and inflation.

The rate of NAIRU could, therefore, be a proxy for 'full employment' or ideal employment as the central bank is not likely to want so many people to be employed that it pushes up wages so high inflation starts to surge since this would compromise its mandate to keep inflation down.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.

"Our estimates of the NAIRU (non-accelerating inflation rate of unemployment) fall somewhere between 4.6% and 5.4% (depending largely on which measure of inflation or wage growth is used), so the current unemployment rate of 4.6% is obviously at the bottom end of that," says ANZ.

If the current inflation rate falls any lower it is likely to start placing inflationary pressures on the economy as it will have fallen below NAIRU.

This seems to suggest the RBNZ will not be focusing too much on fostering 'full-employment' as it has almost already achieved it.

From Single Chair to Committee

In addition to the jobs-requirement, the new government also wants to change the way the RBNZ actually makes it interest rate decisions.

Previously it had been the job of the governor of the RBNZ alone to decide whether or not and when to raise or lower interest rates or enact any other policy decisions, however, the new government now wants a committee to vote on policy decisions.

The committee will be composed of officials within the RBNZ and experts from outside and whilst this could change the current policy trajectory much depends on the exact composition of the committee, the number of independent outsiders, and their individual policy preferences.

However, overall, ANZ do not see a big change as resulting from the move away from 'autocracy' to committee as, "the same inputs will be used that the RBNZ currently use to decide on where the OCR should go (how well the economy is performing, current and future inflation expectations, how much spare capacity exists etc) will still be the same inputs that a formal committee will be discussing too."

If there are to be any major changes, Uerata expects it to be as a result of, "the timing of policy moves. Introducing an employment mandate obviously means there are a few more boxes to tick."

He says, adding:

"Having a formal (and one suspects larger) committee structure means a consensus would need to be formed with a greater number of opinions."

Blurring the Inflation Target

The final change the government wishes to make to the RBNZ relates to its definition of 'ideal' inflation.

Currently, the deal inflation level is set a target at 2.0%, previously it was a range between 1-3%.

One of the changes being considered is to revert to the more flexible 1-3% range target.

According to research carried out by ANZ comparing the way the RBNZ practices policy using the two targets, it would historically allow inflation to run higher when adopting the more elastic target before stepping in and raising interest rates.

This would seem to suggest a further factor which could keep interest rates depressed and as a consequence the Kiwi weaker.

No Change to New Zealand Dollar Forecasts

Although ANZ's Uerata does not see the actual policy changes as impacting too much on the outlook for RBNZ policy, ANZ's negative outlook for growth means he sees interest rates remaining low for some time to come.

"We are less optimistic on the outlook for growth than the RBNZ, and see housing market softness persisting. But we also acknowledge rising risks of more cost-push inflation from the labour market," says Uerata.

As a consequence, ANZ is to keep its current interest rate (OCR) forecast for RBNZ:

"Overall we are happy to retain OCR hikes within our forecasts, although the timing of those hikes is far from clear-cut."

Overall there is a higher chance of a delay in increasing interest rates:

"Perhaps if anything, allowing the RBNZ a little more flexibility on its inflation target means that it can be even more cautious in its approach to tightening this cycle than it would have been otherwise," says Uerata.

The Pound-to-New Zealand Dollar exchange rate is forecast to end 2017 at 1.8181 ahead of a climb to 1.85 by mid-2017 and 1.92 by end-2018.

The New Zealand-to-US Dollar exchange rate is forecast at 0.73 by December 2017, where it should still be around mid-2018 ahead of a slide to 0.68 by the end of the year.

The New Zealand-to-Australian Dollar exchange rate is forecast at 0.89 by the end of 2017, ahead of a fall to 0.88 by mid-2018 and 0.92 by end-2018.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.