- GBP/NZD nearing 1.94 as USD rises with U.S. yields.

- But further upside could be limited & difficult to sustain.

- NZD seen drawing bid, aided by commodity price rally.

© Adobe Stock

- GBP/NZD spot rate at time of publication: 1.9364

- Bank transfer rate (indicative guide): 1.8687-1.8817

- FX specialist providers (indicative guide): 1.9069-1.9223

- More information on FX specialist rates here

The Pound-to-New Zealand Dollar rate was nearing three-month highs on Friday but could struggle to extend much further in the short-term, despite Sterling's newfound appeal to investors, because an anticipated strong performance from the Kiwi is likely to curtail its rise.

Pound Sterling was nearing 1.94 again ahead of the weekend as the U.S. Dollar rose alongside American bond yields and the New Zealand Dollar beat a hasty retreat with other non-oil commodity currencies.

Price action came as stocks tumbled across the board after a steep and ongoing rise in U.S. as well as global yields spooked investors, although Federal Reserve (Fed) Jerome Powell indicated Thursday that he and the bank see these moves as merely reflecting an economic recovery in motion.

"We think an important factor in rising yields since the latter half of February has been that longer-term investors, rather than pushing back against short trades in sovereign debt made primarily by speculative investors, have instead been following the speculators'," says Masanari Takada, a strategist at Nomura. "What may be happening, we think, is that traditional longer-term investors (including real money) have been intermittently contributing to the rise in yields by reshuffling their portfolios in accordance with a more optimistic view."

Above: GBP/NZD at houry intervals with 10-Yr U.S. bond yield (purple) and GBP/USD (green).

Previously and in February Sterling rose back above 1.90 and a level it lost following the U.S. election amid a market reappraisal of the British currency. This was at least partly compelled by a hint from the Bank of England (BoE) that a negative interest rate policy might not be a foregone conclusion after all.

"There has been a significant shift over recent weeks from the pricing of negative rates in the UK to discussion about when the BoE could start firming up guidance on the timing of the first rate hike (or changes in asset purchases). This is likely to build as a theme," says Yuan Cheng, a strategist at Natwest Markets in a late February note. "The impact of Brexit on activity may yet corrupt the uptrend, with monthly trade and GDP data on March 12th presently the first opportunity to gauge the impact. For now, we stay long Sterling vs both the EUR and CHF, while anticipating gains against the USD to 1.45. Underperformance vs commodity currencies is also expected to continue."

Britain's early move to begin vaccinating against the coronavirus has given the economy a headstart in recovery and seen the BoE go from worrying about the likely depths of a double-dip contraction of the economy this quarter, to fretting about upside risks to its inflation target over a two-to-three year time horizon.

Above: Pound-to-New Zealand Dollar rate shown at daily intervals alongside NZD/USD (blue) and GBP/USD (green).

Chief economist Andy Haldane said in a February 26 speech that "there is a tangible risk inflation proves more difficult to tame, requiring monetary policymakers to act more assertively than is currently priced into financial markets," which has left the BoE stood in stark contrast to the Reserve Bank of New Zealand (RBNZ) and others.

A recovery that comes earlier and stronger than elsewhere, supported by unprecedented public financial support as well as so-called enforced savings, has led Haldane and others to mull upside risks to the BoE's 2% inflation target. All while saying nothing to discourage a bid for Sterling.

Meanwhile, RBNZ Governor Adrian Orr said Wednesday the Kiwi Dollar would be even higher if not for actions taken by the bank already, echoing his Trans-Tasman colleague in Reserve Bank of Australia (RBA) Governor Philip Lowe, whose deputy said the same about the Aussie last month.

This is after the RBNZ made clear in February that negative interest rates remain on the table as a potential policy tool, despite the bank having encouraged markets to believe it'd abandoned that idea back in November when the RBNZ lifted forecasts for its own interest rate while noting a stellar performance from New Zealand's economy.

Above: Bank of England graph shows market expectations for Bank Rate in February and March 2021.

"While the operational backgrounds differ for these tools, they all act to lower the interest rates faced by households and businesses so as to incentivise spending and investment and keep the NZ dollar exchange rate lower than otherwise," Orr said. "These actions aimed to head off unnecessarily low inflation or deflation and unnecessarily high and persistent unemployment."

Few central bankers would ever be likely to acknowledge it, but antipodean central bankers are admittedly calibrating their communications as well as policies to prevent increases in their commodity-backed currencies, which have proven popular buys with speculative investors since last year.

With the global economy on the verge of a new business cycle, commodity currencies were always likely to be in demand this year, although like others elsewhere the central banks in Australia and New Zealand have long been unable to sustainably meet their inflation targets.

This has led them to fear rising exchange rates, which cheapen the cost of imported goods and can potentially reduce inflation over a one-to-two year horizon or just more. Hence recent and increasingly frequent complaints about strength in their currencies.

Above: Bank of England graph shows market expectations for UK inflation.

This is not so much the case for the BoE, which is partly why Sterling recovered from around 1.86 in January to near 1.94 in February and March.

The Pound-to-New Zealand Dollar rate has held around 1.92 this week, although Orr's comments speak directly of the challenge faced by Sterling if it's to extend much beyond its current levels over the coming weeks and months.

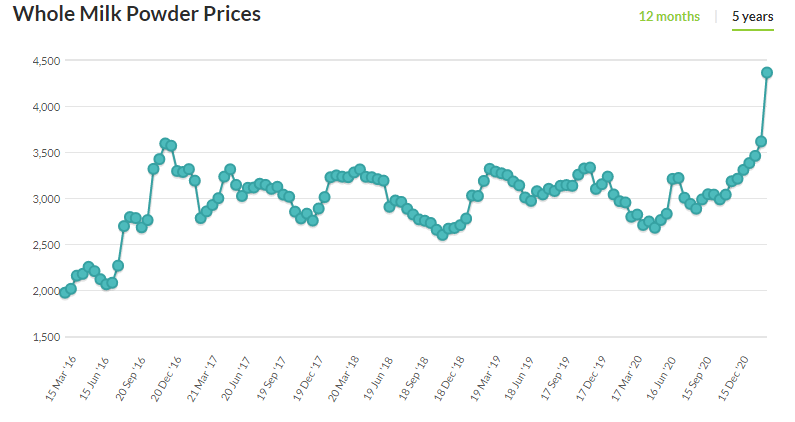

"NZD/USD is undervalued relative to the equilibrium implied by Whole Milk Powder prices," says Elias Haddad, a senior FX strategist at Commonwealth Bank of Australia. "The last time the price of New Zealand’s main commodity export was trading at these lofty levels (highest since March 2014), NZD/USD was trading near 0.8000!"

GBP/NZD would be found trading back at 2.01 and its highest since August 2020 if Natwest Markets is right about GBP/USD rising back to 1.45 in the weeks ahead, although this would only happen in the evidently unlikely event that NZD/USD remained around Thursday's 0.72.

But the rub for Sterling is that ' bullish views on commodities are increasingly as vindicated as they are unrelenting, which is partially evidenced by the whopping 15% increase for the average dairy price in this week's Global Dairy Trade auction. That merely disguised even larger gains in prices of New Zealand's main export.

Source: Global Dairy Trade.

Whole milk powder prices rose 21% to $4,364 per tonne this week, the strongest increase of any good at the auction and taking prices up to a level that is historically consistent with a much higher NZD/USD.

"Fx markets had ceased watching GDT results over the past few years because the results were trivial (average change of 2.5%), but last night’s outturn should grab attention and a belated pricing into the NZD is plausible," says Imre Speizer, head of NZ strategy at Westpac. "Medium-term we remain bullish and target 0.7550 by April."

Rising prices for export commodities are a recipe for increases in the 'terms of trade' ratio of export prices to import prices, which would be a positive fundamental influence on any currency, and when taking place in relation to an economy that is thought to have already recovered output lost to the coronavirus last year the New Zealand Dollar's credentials for outperformance become clear. This is why Natwest Markets and almost all antipodean banks anticipate Sterling will struggle to rise further against the Kiwi.

The main Sterling exchange rate GBP/USD would have to rise all the way back to 1.45 and directly in line with the target of Natwest Markets over the coming weeks simply in order to prevent GBP/NZD from falling below 1.92 in a market where NZD/USD is at the 0.7550 level envisaged by Westpac. GBP/NZD always closely reflects relative price moves in NZD/USD and GBP/USD, as the exchange rate is determined by an amalgamation of the aforementioned two.

Above: Pound-to-New Zealand Dollar rate shown at weekly intervals alongside NZD/USD (blue) and GBP/USD (green).