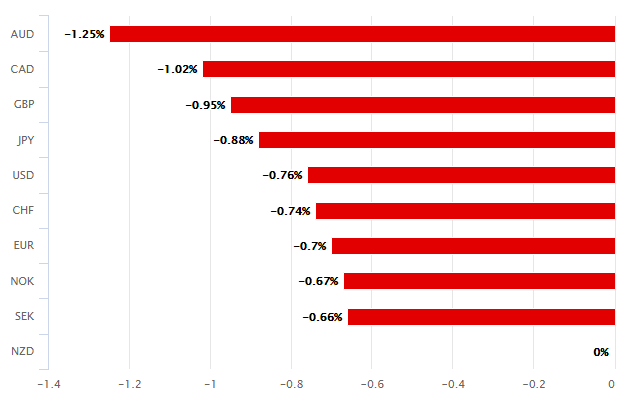

- NZD at bottom of barrel after RBNZ doubles QE programme.

- RBNZ to buy NZ$60bn Gov bonds, warns of negative rates.

- Stops NZD/USD rally at 50% retracement of 2020 downtrend.

- Drives GBP/NZD spike but GBP risks 1.93-to-2.0 range ahead.

Above: RBNZ Governor Adrian Orr. File Image © Pound Sterling, Still Courtesy of RBNZ

- GBP/NZD spot at time of writing: 2.0416

- Bank transfer rates (indicative): 1.9702-1.9845

- FX specialist rates (indicative): 2.0111-2.0233 >> Get your quote now

The New Zealand Dollar was left reeling by the Reserve Bank of New Zealand (RBNZ) Wednesday after the lender of last resort doubled the size of its government bond buying programme, ending a weeks-long Kiwi rally and prompting a short-term Pound-New Zealand Dollar rate spike in the process.

New Zealand's Dollar plumbed the bottom of the major currency barrel and was wallowing in heavy losses against all comparable rivals on Wednesday after the RBNZ increased its quantitative easing (QE) target from NZ$30bn to N$60bn and warned that it could yet resort to a negative interest rate policy.

"The global economic disruption caused by the COVID-19 pandemic is expected to persist and lead to lower economic growth, employment, and inflation both in New Zealand and abroad. Even if New Zealand successfully contains the spread of disease locally, reduced world activity will mean lower demand for many of New Zealand’s exports," says Governor Adrian Orr, in a statement. " The expansion to the [QE] programme aims to continue to reduce the cost of borrowing quickly and sharply. This is preferable to delivering a smaller amount of stimulus now, only to risk later realising more should have been done."

The increased QE programme could eventually see the RBNZ buy up around half of New Zealand government debt, if it becomes necessary in order to keep bond yields and borrowing costs for the government and rest of society low. However, any shift to negative interest rates would see investors forced to pay the Kiwi government for borrowing their money in the much the same way as happened with the German government.

Above: New Zealand Dollar performance against major currencies Wednesday. Source: Pound Sterling Live.

No currency would have taken well the idea of bond yields (investor returns) being pinned to the floor for any length of time, although certainly not a high-yielding commodity currency like the Kiwi Dollar. And negative interest rates would never have been welcomed by a market where the aim of the game is 'fixed income' rather than outgoings, which explains why the NZD/USD rate was turned away Wednesday from a key technical resistance level while the beleagured Pound was lifted sharply against the Kiwi.

"The kiwi suffered a very steep sell-off overnight as the aggressive RBNZ moved ahead with a surprise doubling of its intended QE purchase amounts and by bringing the prospects of negative rates into the discussion," says John Hardy, head of FX strategy at Saxo Bank. "Sterling is trading on the weak side again."

Kiwi losses turned the NZD/USD away from the 50% Fibonacci retracement of the 2020 downtrend at 0.6114, which it has attempted but failed to overcome on multiple occasions since the beginning of April. A sustained break above that level could have prompted a challenge of 0.6268, the 61.8% Fibonacci retracement. NZD/USD had risen 13% from its March lows, reducing a -23% 2020 loss to just -9.9% on Tuesday, in a move that was arguably always likely to get the attention of the RBNZ sooner or later.

"The "NIRP card" must in some ways be linked to the RBNZ's views on the NZD," remarks Stephen Gallo, European head of FX strategy at BMO Capital Markets.

The Pound-New Zealand Dollar rate rose from beneath the 2.02 handle to test the 2.04 handle in response to the RBNZ decision, although these rates and those available in the coming days could be as good as they get for some time to come because the UK's slowcoach 'lockdown' exit and returning Brexit heawinds risk pushing Sterling into a 1.93-to-2.0 range over subsequent weeks. And once committed to such a retreat, Sterling might need a definitive resolution of the Brexit question before it can recover.

Above: GBP/NZD at weekly intervals, fails to sustain 2020 move above 78.6% Fibonacci retracement of 2016 downtrend.

These above Kiwi Dollar rates would only available at interbank level, with those quoted to retail and SME participants likely much lower. Specialist payments firms can help squash the spread between interbank and retail rates.

"The RBNZ wants to see interest rates within the economy fall further. Some easing is in the pipeline and the RBNZ is counting on retail lending interest rates falling. The RBNZ has several other options that will be timelier and likely more effective than setting a negative OCR. There is a good chance the RBNZ puts them to use as it assists fiscal stimulus to help get the economy out of the COVID hole," says Nick Tuffley, chief economist at ASB Bank.

The RBNZ has cut the cash rate from 1% to 0.25%, where it remained on Wednesday, since the beginning of the coronavirus crisis and launched for the first time a government bond buying programme that could ultimately see it owning more government debt than any other central bank including those like the Bank of England (BoE) and European Central Bank (ECB) who've been doing quantitative easing for years already.

Wednesday's decision came after New Zealand reported just three new coronavirus cases for Tuesday and with the country prepaing to shift from 'Alert Level 3' to 'Alert Level 2' as the government moves through the gears of its 'lockdown' exit strategy following a succesful effort to contain the pneumonia-inducing disease. Daily cases have been in the single digits since April 19 and the total number of Kiwi infections was just 1,497 on Wednesday.

Above: NZD/USD repeatedly tests 50% Fibonacci retracement of 2020 downtrend before being turned away on Wednesday.

"Although COVID-19 is firmly on the retreat in New Zealand, it is wreaking economic devastation abroad. And the balance sheet damage done in the last couple of months in New Zealand is huge. It’s going to be a long slog out, and both fiscal and monetary policy will need to do their bit to help the economy recover. A ramping up of both the size and breadth of the QE program is certainly possible, with purchases of foreign assets to dampen the exchange rate potentially on the cards," says Sharon Zollner, chief economist at ANZ. "And next year, when the financial system is technically ready, we can’t rule out the possibility of negative interest rates."

Zollner is "highly dubious" that negative interest rates will do anything positive for economic activity but expects the mere threat of them to continue weighing on bond yields, thereby reducing borrowing costs for the government and country. That threat will also continue to weigh on the exchange rate, which the RBNZ has a long history of discussing - although RBNZ discussions of the Kiwi Dollar only tend to come amid bouts of appreciation in the currency.

Currency strength risks making Kiwi exports to a still-struggling global economy less competitive while reducing import prices, which can crimp inflation and compromise the RBNZ's ability to deliver the 2% midpoint of its 1%-to-3% inflation target. Kiwi inflation rose above that midpoint for the first time in years during the first quarter, after a laborious effort on the part of the RBNZ, but a Kiwi Dollar rally might kibosh that tentative rebound in price pressures and necessitate further experimentation with even more unconventional monetary policies further down the line - like negative interest rates.

"Realistically, the prospect of negative rates might only become a reality if there was a view that the main policy tool – QE – was going to reach its limits. This if course is possible but it is easy to forget given the RBNZ’s actions that New Zealand have more or less completely eradicated COVID-19 and are in a considerably better position than most other developed economies. Still, the actions of the RBNZ will mean the scope for any notable move higher in NZD is limited for now," says Derek Halpenny, head of research, global markets EMEA and international securities at MUFG. "We have a roughly flat forecast profile over the initial period ahead before NZD/USD rises to 0.6400 by end Q1 2021."