Image © Naru Edom, Adobe Stock

- GBP/NZD neutral to bullish signs in short-term

- Break higher possible but bearish longer-term

- Pound impacted by Brexit fears; New Zealand Dollar by RBNZ meeting

The GBP/NZD exchange rate is trading at 1.9304 at the time of writing, little changed from the week before. Studies of the charts suggest that the exchange rate is likely to trade with a mildly bullish bias over the next five days.

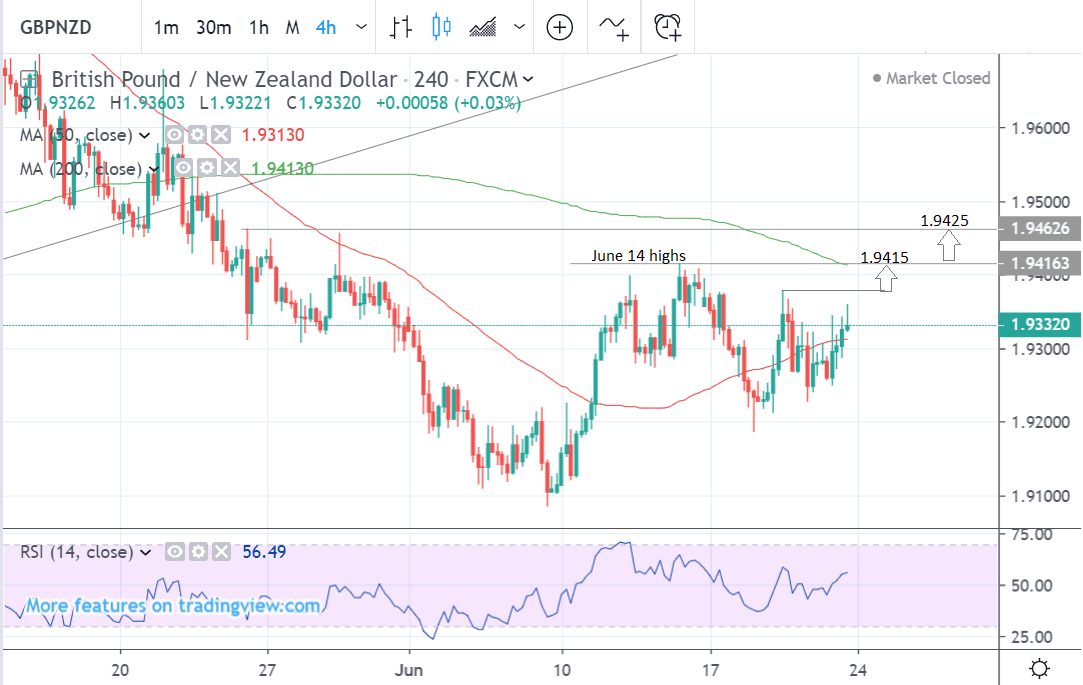

The 4-hour chart shows how the pair rose up at the beginning of June and then oscillated sideways from June 10. The initial rally established a short-term bullish bias.

There are two main possible outcomes in the short-term: the pair could either continue its ‘random walk’ sideways or break higher in line with the early June rally.

An upside break is conditional on a move above the 1.9380 June 19 highs, which would pave the way to a move up to a target at 1.9415.

A continuation of that uptrend to the next target at 1.9425 would be conditional on a further break above the June 14 highs.

The 4-hour chart is used to give us an indication of the short-term outlook which includes the next five trading days.

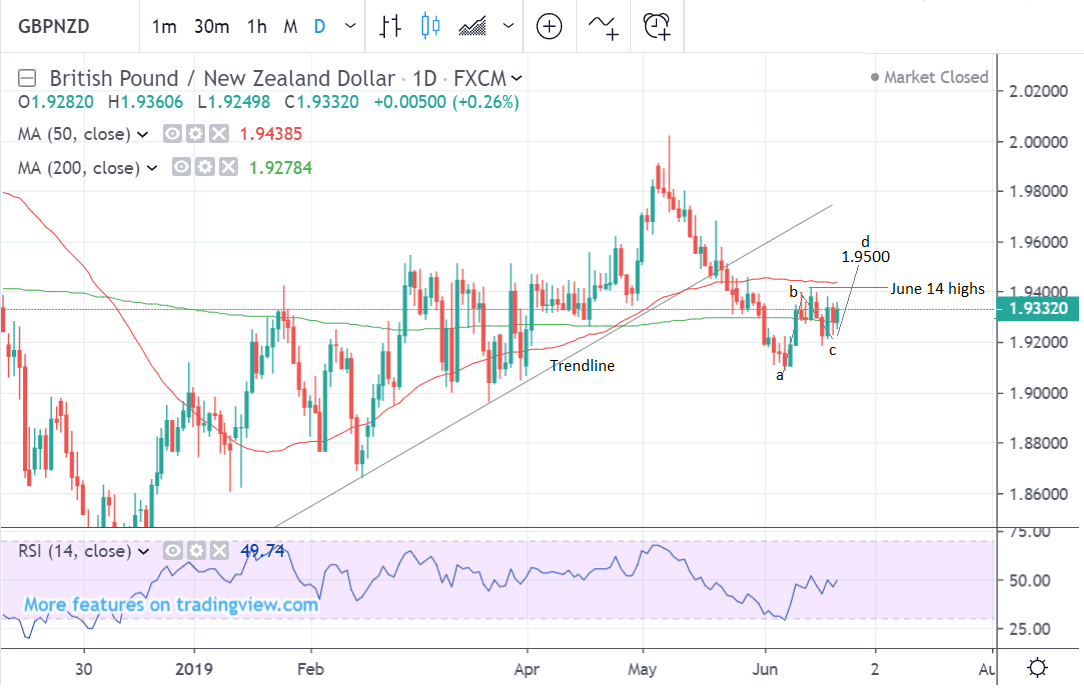

The daily chart shows how the pair was in a downtrend and broke below a major trendline. This trend seemed to bottom at the start of June, however, and since then the exchange rate has turned around and started to rise.

Whilst it is still early days, the pair could continue rising in what might be an ‘abcd’, or Gartley pattern. If so then the final c-d leg higher might very well reach a target at 1.9500.

However, such a continuation would be conditional on a break above the 1.9415 June 14 highs, since the pair still remains vulnerable to a breakdown.

The daily chart is used for an indication of the medium-term outlook which includes the next week to a month.

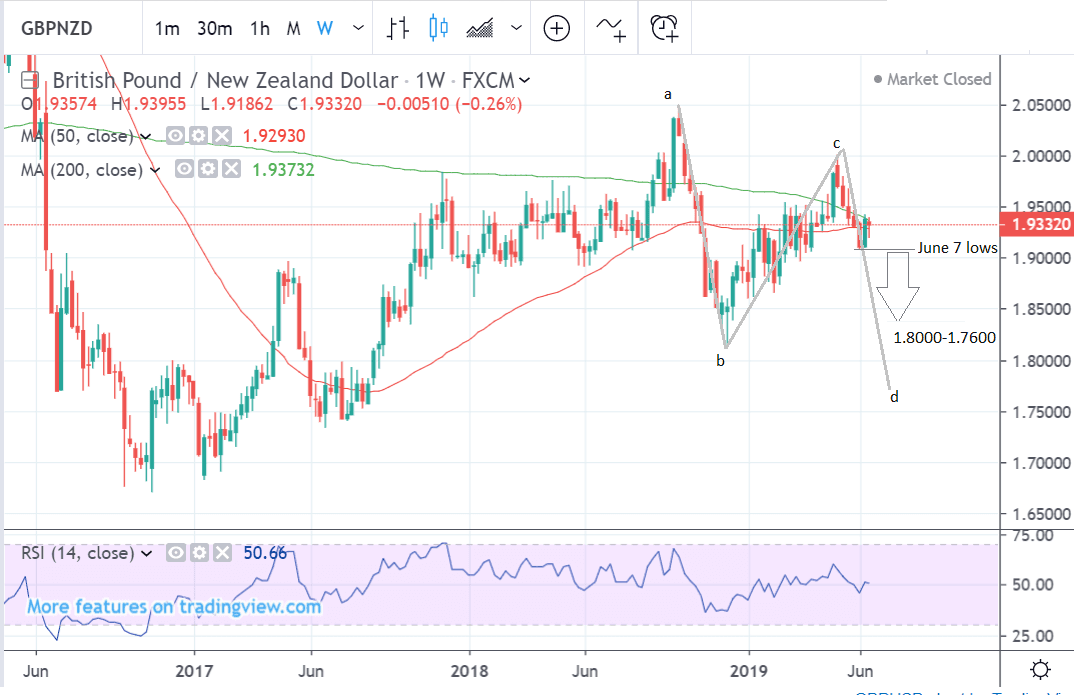

The weekly chart shows how the short and medium-term uptrends will probably eventually petter out and rotate to the downside longer-term.

The pair appears to be forming a bearish ABCD or Gartley pattern, suggesting an extension of the downtrend since the 2018 highs is possible.

These patterns are composed of three waves in a zig-zag formation. The length of A-B can be used to forecast the length of C-D. In this case it suggests an end target for C-D of around 1.7600 - 1.8000.

A downside development, however, would be conditional on a break below the June 7 lows.

The weekly chart is used to give an idea of the longer-term outlook, which includes the next few months.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement

The New Zealand Dollar: What to Watch

The main drivers of the New Zealand Dollar in the coming week are likely to be the Reserve Bank of New Zealand (RBNZ) monetary policy meeting and global risk trends, to which the currency is also highly sensitive.

The RBNZ is scheduled to end its monetary policy meeting and announce its decision on Wednesday at 3.00 BST, with a press conference hosted by governor Orr an hour later.

Most analysts do not expect another rate cut at the June meeting so soon after the RNBZ cut rates by 0.25% in May. However, there seems to be an agreement that conditions have worsened since May and this has increased the probability of a cut, if not next week, then perhaps in August.

Q1 GDP out last week, came in at 0.6%, as expected and the same as the previous quarter, however, the global backdrop appears to have worsened, increasing pressure on the central bank to ease policy.

"We expect the RBNZ to leave its cash rate on hold at 1.5% and reiterate its easing bias on Wednesday. A 25bp rate cut is partly priced, therefore there is room for NZD volatility on Wednesday, particularly if the RBNZ surprise the market and cut rates this week, rather than wait until August, and the release of the quarterly Monetary Policy Statement," says Joseph Capurso, a currency strategist with Commonwealth Bank of Australia.

The RBNZ will be conscious that global economic outlook remains uncertain and major central banks have recently shifted their stance on the dovish side.

Analysts at Westpac bank see the risks of a rate cut having increased further since May.

“The balance of risks has evolved in the direction of another cut, mainly due to global developments. But not so emphatically that the RBNZ needs to appear panicked by cutting the OCR again so soon,” says Westpac.

On the global risk trends front, the main event will be the G20 conference, on Friday, June 28.

All eyes will be on whether the two superpowers at the summit - the U.S. and the Chinese - can reach a detente, however, it seems highly unlikely they will. The consensus expectation is for the two sides to reaffirm a commitment to further talks.

"All eyes on the Xi-Trump meeting at G20. Most seem to expect an agreement to start talking again, and at best, an indefinite delay on the next tranche of tariffs (the public comment period on those ends next Monday)," says Elsa Lignos, a foreign exchange strategist with RBC Capital Markets.

China has clear red lines, making a full trade deal with the U.S. unlikely in the near-term.

The first is the removal of all tariffs - something the U.S. is dead against.

The second is for U.S. expectations of Chinese purchase of U.S. exports to be “realistic”.

The third is that China will not submit to intrusions on ‘national sovereignty’, which relates to the requirement from the U.S. that it enshrines the trade agreement in domestic Chinese law.

The New Zealand Dollar could fluctuate depending on the outcome for China since it is its largest trade neighbour, so a positive outlook for China would help NZ.

A further cause for concern is the trouble brewing between the U.S. and Iran in the Gulf of Hormuz. If the conflict escalates it could increase risk aversion, which would weigh on the Kiwi.

The Pound: What to Watch

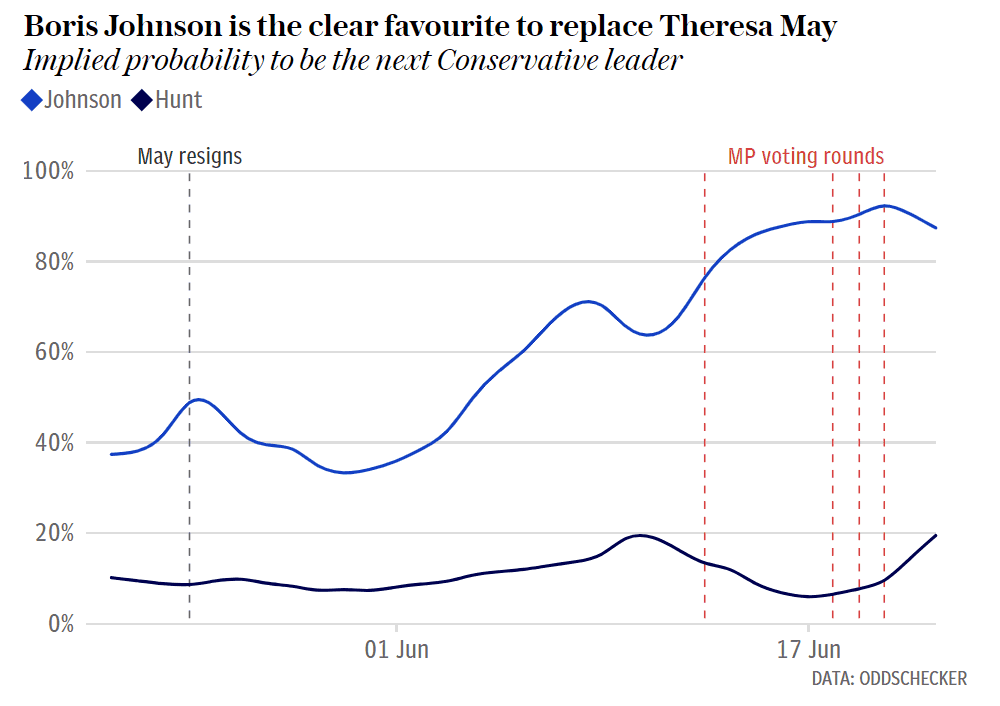

The leadership race may take a back seat as a Sterling driver in the coming week as the two remaining candidates Boris Johnson and Jeremy Hunt will be busy campaigning around the country, and the final results are not expected until July 22.

Johnson is the front-runner by a large margin and bar any major revelations which would make him unsuitable for the job he is likely to win the race and become the next Prime Minister.

Any details on Johnson's Brexit strategy could prove to be important for near-term Sterling direction.

Part of the reason Sterling has weakened over recent weeks is the growing likelihood this will be the case: Johnson is a hard-Brexiteer who could potentially take the UK out of the EU without a deal. However, such a strategy could almost certainly a handful of defections by Conservative MPs opposed to 'no deal', which would ultimately see the Government unable to govern, in turn inviting a General Election.

A General Election taking place over coming months is another source of uncertainty that should see Sterling remain under pressure.

Sterling has also fallen on the so-far unyielding response of EU officials to hints Johnson wants to renegotiate. This has increased the chances of a stalemate and the UK simply flopping out without a deal on October 31.

Another possible factor which could impact on the Pound is the inflation report hearing on Wednesday, June 26.

This involves the Governor of the Bank of England (BOE) Mark Carney and other BOE officials taking questions from the Parliamentary treasury select committee on the outlook for inflation and the economy.

Although most of their answers will be highly conditional on what sort of Brexit the UK has, they could still impact the Pound.

The BOE uses inflation and other economic data to decide on the level at which to set interest rates, and these have a direct influence on the Pound.

If growth and inflation rise the BOE tend to put up interest rates which appreciates the Pound. Higher interest rates attract greater inflows of foreign capital and vice versa for lower interest rates.

The second estimate of Q1 GDP is forecast to show growth unchanged at 1.8% year-on-year (yoy) and 0.5% (mom) when it is released on Friday on 9.30 BST. Only a revision would impact Sterling.

Other data out in the week ahead is the current account and business investment, which are both scheduled for release at the same time as GDP; and gross mortgage approvals, out at 9.30 on Wednesday.

* Advertisement