The past two weeks have confirmed the British pound has definitely lost its April shine and the reason for this underperformance is probably not what most people would expect.

- Up to 2% worth of GBP/USD downside lies ahead warn ING

- Westpac confirm selling GBP/USD is a ‘high conviction’ call

- GBP to USD exchange rate at 1.4437 at time of writing, GBP to EUR at 1.2655

Without doubt, the dominant theme when discussing the performance of sterling, and its outlook, is the June referendum on continued UK membership of the European Union.

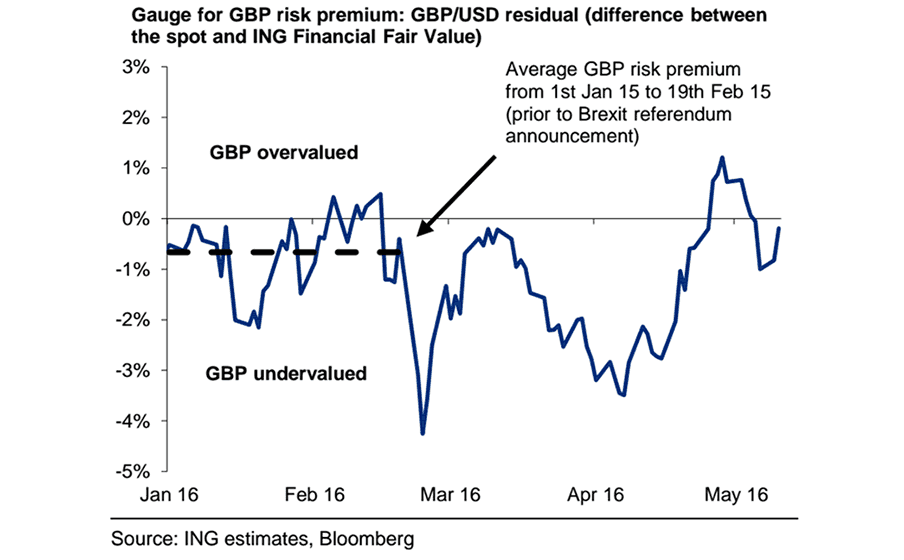

While the Brexit premium is certainly a factor in the GBP’s ups and downs in 2016, it is not the only factor and research suggests we should have our eyes on multiple drivers.

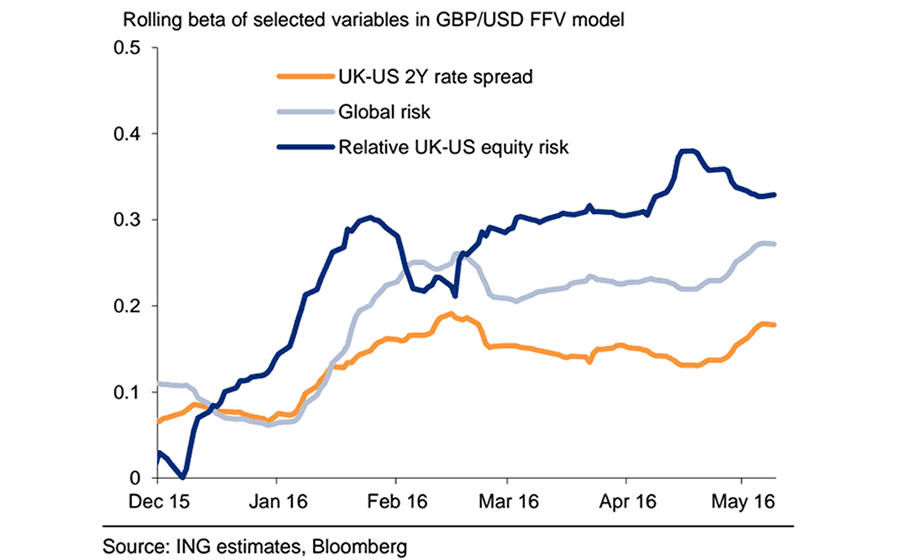

Of particular interest to us is the role played by risk sentiment - i.e that hard to define confidence amongst investors on a global scale.

We have hinted at the important role sentiment plays on sterling having at times observed how the GBP/EUR tracked the German DAX; stock market performance is typically the most obvious expression of investor sentiment.

The relationship between GBP and the DAX turns on and off, but analyst Viraj Patel at ING confirms the concept is valid.

“The initial shift in global risk sentiment in recent months (from bearish to tentatively neutral) has been a positive driver for GBP, accounting for more than half of last month’s recovery,” says Patel.

Furthermore, Patel notes that the impact of the EU referendum on pound valuation is waning.

(However, ING are aware that the impact of the referendum over the coming weeks will likely pick up once more as polling and odds markets converge.)

We would certainly expect sentiment around the vote to continue playing a part in GBP moves over coming weeks, but it could be the role of risk sentiment that has an outsized role.

Indeed, a look at the foreign exchange markets at the time of writing shows the pound sterling to be lower against the euro and US dollar, in line with lower European stock markets.

“Signs of a stabilisation in risk appetite (as opposed to new found optimism) means that this risk impulse is beginning to fade,” says Patel who has taken a negative stance on the pound’s outlook as a result.

Latest Pound/Euro Exchange Rates

| Live: 1.1609▲ + 0.15%12 Month Best:1.171 |

*Your Bank's Retail Rate

| 1.1214 - 1.1261 |

**Independent Specialist | 1.1446 - 1.1493 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Why Has Risk Appetite Fallen, Will it Improve?

Risk appetite has eased since mid to late April and the impact is particularly accute in emerging market equities, metals and bulk commodities and currency markets, while developed market equities, credit markets, energy markets and the VIX and Move indices have been on a more stable footing.

Going forward risk aversion could exert itself further.

“Expectations for a second quarter US recovery have been left wanting, at least so far, with the April ISM and payrolls data coming in weaker than expected,” says Richard Franulovich at Westpac Institutional Bank.

Franulovich cites China’s recovery as another factor that could be playing on investor confidence.

The recovery appears to have stalled after barely a month, certainly that’s the impression left by the softer April PMIs and weaker April import data.

Past stimulus cycles going back to 2008 produced a recovery in the PMIs that typically lasted 4-5 months.

“A run of weaker US and China data would obviously have broad negative implications for risk appetite. As the slide over shows our risk appetite index (smoothed) has been highly correlated with our global data surprise index and the latter appears to be on the cusp of rolling over,” says Franulovich.

Weaker Q2 growth signals out of the US and China growth are so far more tentative than definitive.

“After all, we are barely half-way into Q2. That said, data due later this week - US April retail sales due Friday and China April industrial production due Saturday - could be highly informative and very consequential for global markets,” says Franulovich.

The Economy: 2% Downside in Sterling Ahead

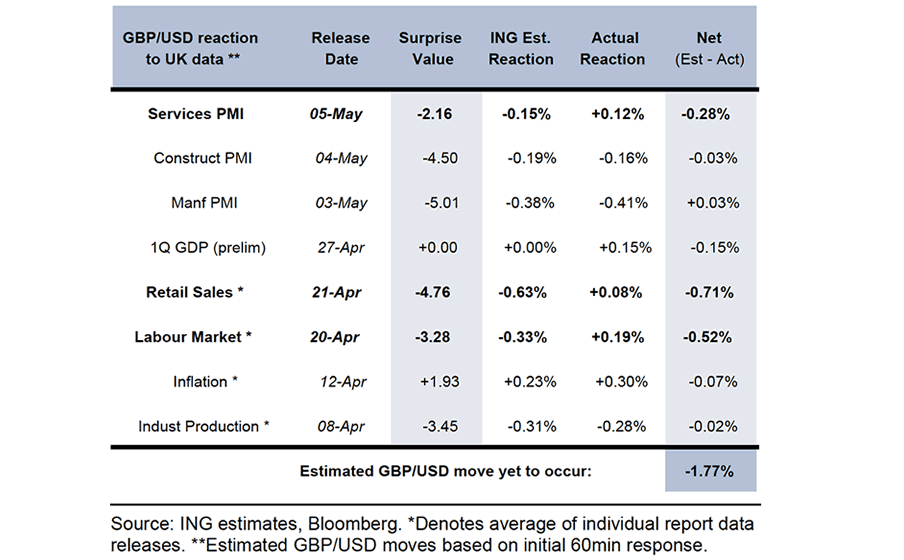

The British pound has certainly not found any support from recent data releases with official industrial production data confirming the slowdown flagged in the PMIs as being on the money.

The all-important services PMI data came in well below analyst expectations confirming a slowdown in the middle part of 2016 is real.

Despite the trends in data we saw GBP hold its ground, and even advance against the US dollar in the positive risk environment that we note allowed GBP/USD to pop higher in April.

This all leaves the pound looking exposed to a downside correction should fundamentals exert their control over GBP argue ING:

“GBP brushed off the weak UK data in April; BoE meeting might be the catalyst for pent-up weakness to manifest. Despite a sequence of hefty negative surprises over the past month, we note that typically data-sensitive GBP pairs (eg, cable) have been remarkably dismissive of the weaker UK data.”

“Our data surprise analysis shows that there could be around 1.5-2.0% worth of pent-up downside in cable due to the deterioration in the UK fundamental outlook,” says James Knightley, Senior Economist with ING in London.

Franulovich and his team at Westpac are also negative on the pound’s prospects saying their High Conviction model is advocating for a decline in GBP/USD:

“We remain short GBP, from 1.4710, exit shifted down to 1.4605. GBP still looks expensive even after the +2% pullback from the highs. Further downside more likely than not as the referendum on EU membership approaches.

“A weaker suite of April PMIs (construction, manufacturing and services) along with softer BRC sales and Halifax house price data suggest growth momentum is waning into Q2, adding an additional cautionary layer to GBP.”

Westpac’s “High Conviction Trades" model blends the long/short/neutral recommendations from three of their research streams: G10 FX model (quantitative analysis), ForeX focus (macro analysis) and technical analysis.

The aim is to underscore their highest conviction ideas.

And it looks like the British pound has attracted enough attention on all three fronts to warrant a sell recommendation.