Image © Adobe Images

The British Pound was the day's best performing major currency by the time U.S. markets started trading on Monday, Sept 26.

The gains formed part of a remarkable turnaround in fortunes for a currency that had just hours earlier suffered a significant decline that saw it post a new record low against the U.S. Dollar.

These declines came in thin Asian markets, bringing back memories of the 2016 'flash event' in Sterling, something the Bank for International Settlements blamed on three factors, most important amongst them the time of day.

It could be that Asian traders were accounting for the selloff in Sterling seen on Friday in Europe and the U.S., which of course occurred outside their hours.

The recovery seen through the day could be in part a correction in the market following a technical dislocation, but talk of a potential statement from the Bank of England could also be fuelling the recovery.

It is reported the Bank of England will make a statement following today's moves, giving investors pause for thought when it comes to opening fresh bets against the UK currency.

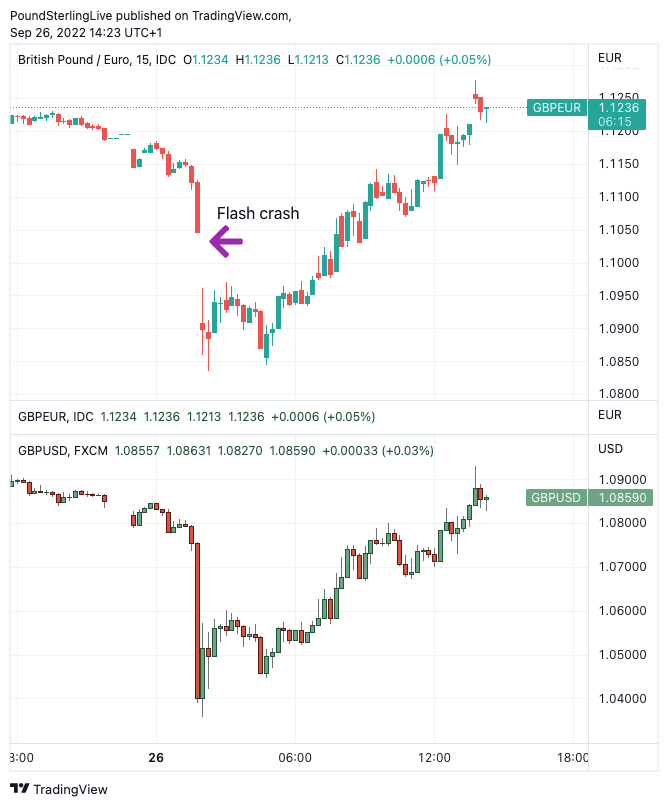

The Pound to Euro exchange rate was seen back at 1.1235 just before the U.S. open, having been as low as 1.0793 earlier in the session, taking bank account money transfer rates to around 1.1010 and the rate offered at independent providers to around 1.1200.

The Pound to Dollar exchange rate was seen back at 1.0860 at the time of publication having been to record lows at 1.0348 during the Asian session. Bank transfer rates are quoted towards 1.0640, those quoted at independent providers are in the region of 1.00825 according to our data.

Above: GBP/USD (top) and GBP/EUR (bottom) at 15 minute intervals. To better time your payment requirements, set your FX rate alert here.

"Aggressive GBP move overnight is being faded somewhat as European markets open. The retracement in the pound is coinciding with a substantially more hawkish BoE rate path and broad-based expectations of an inter-meeting rate hike from the sell-side," says Simon Harvey, Head of FX Analysis at Monex Europe.

The 'sell-side' referred to here are the analysts at major investment banks, such as Deutsche Bank's George Saravalos who has argued the Bank of England must now intervene by raising interest rates agressively.

The Bank is only due to meet in November and Saravelos suggest action would be required sooner to "restore credibility".

Tatjana Punhan, Deputy Chief Investment Officer at Tobam, agrees that the Bank of England would likely have to intervene before their next official policy meeting.

If they don't, she suggested the members of the Monetary Policy Committee "should lose their job".

Martin Malone, Chief Economist at Auriel, says much of the blame for Sterling's decline lands at the door of the Bank of England.

The Bank of England "is not in the game at all," said Malone in a Bloomberg interview Monday.

He said the Bank of England made "a huge mistake on Thursday" by only opting for a 50bp hike, when the Federal Reserve had gone 75 basis points just hours before.

In short, the Bank continues to be 'out hiked' by the Fed, and indeed, by most other central banks. But he says the Bank will however have to wait until November to hike, saying an inter-meeting hike would be coming from a position of weakness.

Malone says the government's strategy of trying to stimulate growth by its fiscal policy changes is actually "a positive one".

The British Pound suffered significant declines during the Monday Asian session that added to Friday's massive selloff, ensuring record lows against the Dollar and a move below 1.10 against the Euro.

Analysts say the Pound's weakness comes as traders bet the UK government will be unable to finance its debt burden at a time the Bank of England refuses to raise interest rates to the extent the market demands.

The falling Pound comes alongside rising debt costs in the UK as investors sell government bonds, thereby driving up their yield.

The selloff in both the currency and bonds follows the announcement by the UK government it would cut taxes at a time when it has significantly boosted spending to cap energy bills for households and businesses.

Economists suggest this combination means the government will inevitably be unable to borrow the amounts of money required to meet their objectives.

But is the Pound in a genuine crisis or has a long-overdue correction lower occured?

Paul Krugman, a Nobel Laureat, with ample experience in currency crises, has addressed the talk about a looming Sterling crisis:

"I'm supposed to know something about currency crises - I did invent the academic field! And as far as I know there are two ways a country with a floating exchange rate can have a currency crisis, neither of which seems to apply to the UK," says Krugman.

"Since the 1990s, most currency crises have involved balance sheet effects: a country (either public or private sector, or both) has large external liabilities in foreign currency. In that case depreciation worsens balance sheets, creating a self-reinforcing downward spiral," he explains.

"While the UK has a lot of external liabilities, they're overwhelmingly sterling-denominated; the UK also has external assets, largely direct investment

"The result is that sterling depreciation actually *improves* Britain's net international investment position (the same thing happens to the US). So a balance-sheet currency crisis story doesn't seem to make sense

"The other way you can have a currency crisis is if markets believe that you can't or won't service your public debt, and will monetize it instead; this was the story behind the 1926 franc crisis and, I think, the 1976 sterling crisis (which needs revisiting) 7

"But the Bank of England is independent these days, and unlikely to monetize debt. And despite everything, UK debt isn't *that* high by long-run standards

"At a guess, the moron risk premium has now been priced in. I guess I don't see the mechanism for a continuing sterling crisis."