- GBP dips following decision

- But seen stabilising through afternoon trade

- More optimistic on UK growth outlook

- Decides to proceed with gilt sales

Image © Pound Sterling Live

The British Pound fell in the minutes after the Bank of England raised interest rates by 50 basis points on Thursday, which was a smaller increment than the 75bp the market was expecting.

The below-consensus hike was met with a knee-jerk sell-off in the Pound and analysts say they expect further declines in the UK currency.

However, a decision to proceed with the selling of gilts acquired under the Bank's quantitative easing programme - as well as expectations for an improved economic outlook relative to previous expectations - could offer the currency some immediate support.

Indeed, as the London trading session proceeds through the afternoon and the U.S. session begins the Pound is looking better supported.

By raising rates below the expected amount the Bank maintains a cautious approach to hiking interest rates, even as it expects inflation to be in double figures for months to come.

"An official Bank Rate of 2.25 percent will not curb UK inflation when it is around 10 percent. It is a shame that the BoE MPC don’t grasp this basic fact," says Andrew Sentance, former member of the Bank's MPC and an advisor to Cambridge Econometrics.

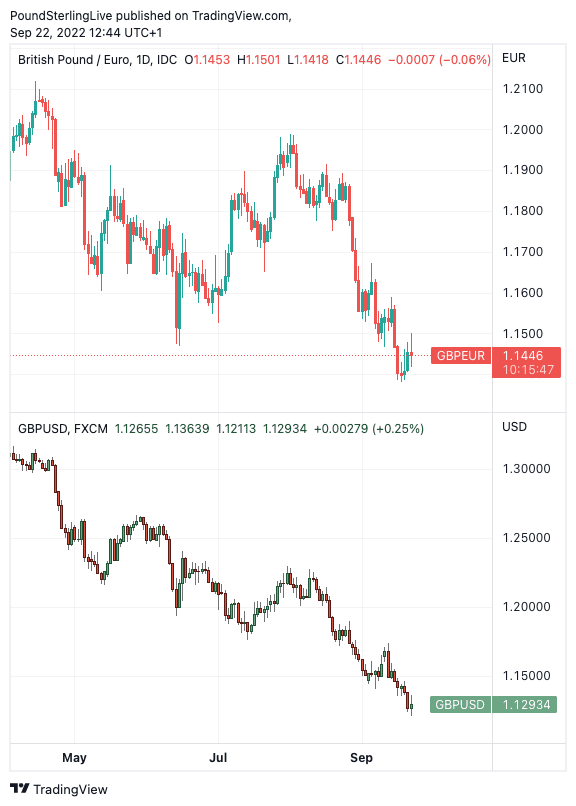

The Pound to Euro exchange rate fell half a percent in the 15 minutes following the decision to 1.1434, but was back to 1.1470 by the time of the U.S. open taking bank transfer rates to approximately 1.1240 and payment specialist rates to approximately 1.1440.

The Pound to Dollar exchange rate fell 0.60% in the 15 minutes following the decision to 1.1286 before recovering to 1.1330, bank transfer rates for dollar payments were down near 37-year lows at 1.1100 and rates at payment specialists at 1.1290.

Above: GBP/EUR (top) and GBP/USD (bottom) at daily intervals. To keep on top of the market you can set a free FX rate alert here.

Five members of the Bank's Monetary Policy Committee (MPC) voted for a 50bp hike while three were in favour of a 75bp hike. One voted for a 25bp move.

The decision to hike by 50bp comes despite the Bank warning inflation would remain elevated over the medium-term as the government's new energy price cap policy takes effect.

They expect the decision to cap prices would bring down the peak in inflation from 13% to 11%, although inflation would trend above 10% "over coming months".

The Bank meanwhile sees an improved growth outlook as consumers find relief in the limited rise in energy bills, a development that could also prove supportive of the Pound, as we noted here.

Friday's fiscal announcement from the government, at which significant tax cuts are expected, are also considered as supportive.

"An additional Growth Plan announcement is scheduled to take place shortly after this MPC meeting, which is expected to provide further fiscal support, and is likely to contain news that is material for the economic outlook," reads the Bank's statement.

"The statement makes it clear that extra government spending, and we'll get more details on that tomorrow, will lead to higher medium-term inflation, given that it should dramatically lower the risk of a deep recession," says James Smith, Developed Markets Economist at ING Bank.

But the Bank still believes at some point in the future inflation will fall to 2.0%, confirming this to be the last central bank on the block to believe inflation is transitory.

The implications if this for the Pound's outlook could be stark.

"If the BoE hikes by 50bps today the combined total will reach 215bps, which would leave the BoE lagging by 10bps the RBA, RBNZ and Norges bank and by 85bps the Fed and the BoC. It would certainly prompt some further GBP/USD selling toward the 1.1000 level," says Derek Halpenny, Head of Research for Global Markets EMEA at MUFG.

The Bank of England did however opt to start selling gilts as it looks to unwind its quantitative easing programme.

At its August meeting the MPC had communicated that it was provisionally minded to commence gilt sales shortly after its September meeting, subject to economic and market conditions being appropriate.

The commencement of gilt sales was less certain following news of increased debt issuance requirements by the UK government to fund its energy price cap; the Bank selling bonds just as the government increases issuance would risk pressuring yields higher.

"At this meeting, the Committee agreed that the conditions were appropriate, and voted to begin the sale of UK government bonds held in the Asset Purchase Facility shortly after this meeting," said the Bank in a statement.

"This is significant, both because it is another form of monetary tightening, and because there had been some speculation that the Bank would delay the start of 'quantitative tightening' to help the government to finance additional borrowing. That would have sent a terrible signal," says independent economist Julian Jessop.

The decision could provide some upside support to UK gilt yields, which could in turn offer some marginal support for Sterling.

But the consensus amongst currency analysts is the Bank of England is not a central bank that is proving supportive of its currency.

"The Bank of England is already experiencing what other central banks are fearing: in view of record inflation levels and comparatively hesitant rate hikes confidence in the central bank is being eroded and inflation expectations are rising," says Esther Reichelt, FX and EM Analyst at Commerzbank.

In addition to the lack of support from the Bank of England Reichelt says "the dire growth outlook, rising government debt and high current account deficit point towards depreciation pressure on Sterling continuing for now."

"A weak currency only fans the flames of inflation, given the UK’s reliance on imports," says Charlie Huggins, Head of Equities, at Wealth Club.

"The Bank of England is stuck between a rock and a hard place. A gentler approach to rate rises risks sending sterling into a tailspin, and seeing inflation get even further out of control. But too much tightening could easily choke the life out of the economy, without significantly easing the cost-of-living crisis," he adds.