Image © Adobe Stock

- Market rates at publication:

GBP/EUR: 1.1650 | GBP/USD: 1.3647 - Bank transfer rates:

1.1420 | 1.3365 - Specialist transfer rates:

1.1589 | 1.3580 - Get a bank-beating exchange rate quote, here

- Set an exchange rate alert, here

The Bank of England remains on track to raise interest rates in the first half of 2022 having delivered what was on balance a 'hawkish' policy update, with one analyst saying the tone was necessary to ensure the Pound remains supportive of the Bank's inflation objectives.

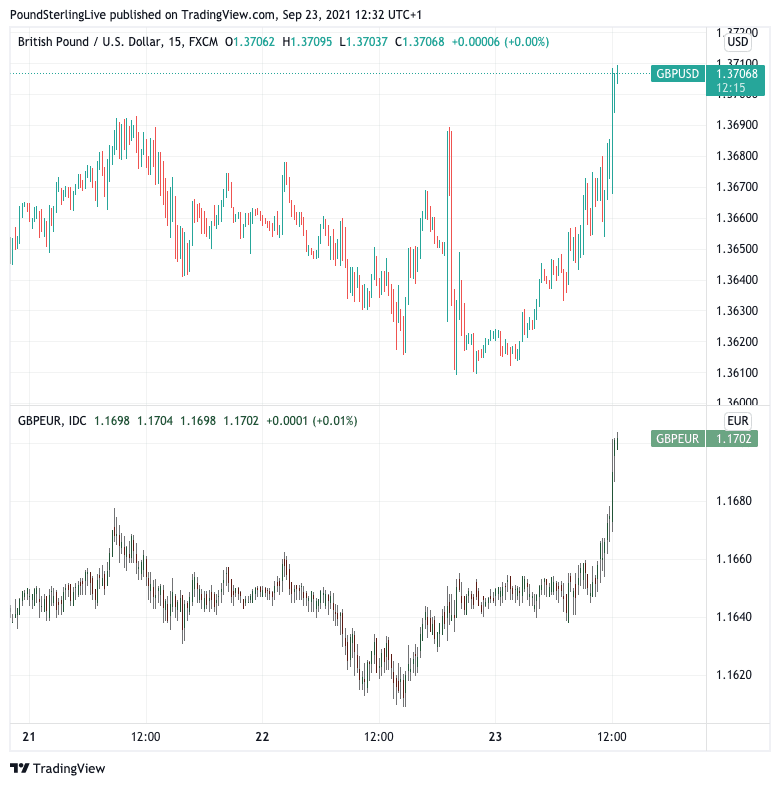

The British Pound rallied against the Euro and Dollar after the Bank opted to maintain interest rates and quantitative easing levels at existing settings but warned of the prospect of inflationary levels remaining elevated for a longer-than-expected period.

The UK currency had fallen in the days leading up to the event, suggesting investors were wary the Bank's Monetary Policy Committee (MPC) would sound a more cautious tone in light of slowing economic growth and the eruption of a full blown energy crisis since their August meeting.

Pound Sterling Live said in a preview article that there was a high likely hood that a 'sell the rumour, buy the fact' trade was underway in currency markets as investor caution rose.

But by going higher in the aftermath the Pound is signalling that the market assesses the September update to still be consistent with higher rates in 2022.

Indeed, following the event money market pricing showed the probability of a 15 basis point rise in the Bank Rate in February 2022 had in fact risen to 87%.

Given the outlook for UK interest rates have not been fundamentally altered following the Bank's update this view on recent and ongoing foreign exchange price action appears vindicated.

The Pound-to-Euro exchange rate is trading back to 1.17, the Pound-to-Dollar exchange rate is back to 1.370.

"We had expected the Bank of England’s MPC to sound hawkish today, and that’s what we got," says Daniel Vernazza, Chief International Economist at UniCredit Bank.

"If unemployment does not rise materially then the MPC will likely tee-up a small (15bp) rate hike as soon as February next year," he adds.

The MPC voted unanimously to maintain Bank Rate at 0.1% and by a majority of 7-2 for the quantitative easing programme to be maintained at existing levels.

Dave Ramsden joined Michael Saunders in voting to prematurely end quantitive easing ahead of its December expiry.

In a statement the Bank said "some modest tightening of monetary policy over the forecast period was likely to be necessary to be consistent with meeting the inflation target sustainably in the medium term."

The statement largely rubber-stamps existing market pricing for rate lift-off to take place in the first half of 2022.

"Some developments during the intervening period appear to have strengthened that case," said the Statement.

But, the Statement was by no means a 'hawkish' surprise as the MPC said considerable uncertainties regarding the global economy and domestic labour markets remain.

Therefore the Pound is likely to recapture recently lost ground as opposed to blaze a path into new 2021 highs.

Economists at the Bank revised down their expectations for the level of UK GDP in the third quarter of 2021 by around 1% since the August Report, leaving the expected level of Q3 GDP around 2½% below its pre-Covid level.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

This downward revision was blamed on supply constraints: this is important given some economists out there have recently said it demand restraints were to blame for the recent slowdown in growth.

The MPC is more likely to go ahead and meet markets' expectation and raise rates if they feel demand remains robust and supply restraints transitory.

The MPC nevertheless said it would monitor closely the incoming evidence regarding developments in the labour market, and particularly unemployment, wider measures of slack and underlying pay pressures; the extent to which businesses pass on wage and other cost increases, as well as medium-term inflation expectations.

The MPC reflected global growth had shown since August and inflation remained elevated amidst a backdrop of robust goods demand and continuing supply constraints.

The Bank also warned that inflation might remain elevated above their 2.0% target on a "more persistent" basis.

Economists at the Bank note that underlying pay growth has picked up to above its pre-pandemic rate, another 'hawkish' takeaway.

They estimate CPI inflation will rise further in the near term and breach their existing 4.0% forecast for the fourth quarter of 2021 but say this is largely down to developments in energy and goods prices.

They touched on the evolving energy crisis saying a material rise in spot and forward wholesale gas prices since the August Report represents an upside risk to the MPC’s inflation projection from April 2022.

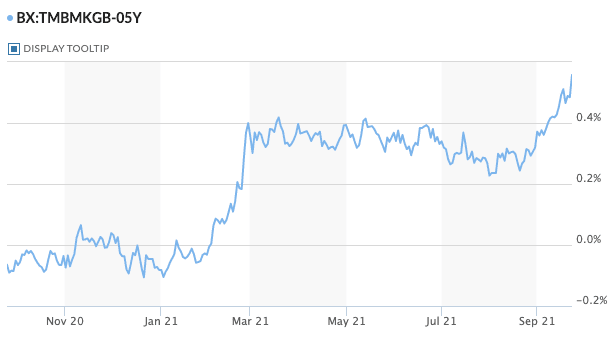

Above: The yield on 5 year UK gilts is on the march higher. GBP has tracked it steadily in 2021 suggesting some catch-up is due.

But the Committee’s central expectation continues to be that current elevated global cost pressures will prove transitory.

“The Bank of England, in its policy decision today, clearly expects the inflation rate to be higher than previously feared," says Hinesh Patel, portfolio manager at Quilter Investors. "While they reiterate it will be transitory, it will no doubt be of major concern."

Patel says because for now inflation is largely being driven by external factors raising interest rates might have little impact on overall inflation levels.

But he makes an important point: the Bank of England does not exist in isolation and therefore what the U.S. Federal Reserve and European Central Bank also do matters.

"With the ECB and Federal Reserve both announcing that they intend to begin the tapering and unwind their financial support, there is a risk that not acting in the same timeline will force UK sterling down even further – exacerbating the inflationary shock further with even higher import prices," says Patel.

Indeed, the Bank cannot afford a significant devaluation of the Pound as it would only risk exacerbating externally driven inflation, therefore holding the line on a 2022 rate hike might be very necessary.

The UK is a net importer of goods and therefore a rising Pound pushes down the cost of imports and is therefore a deflationary force.

While the Bank does not officially target the Pound the MPC will be aware that now could be the worst possible moment to trigger a devaluation.