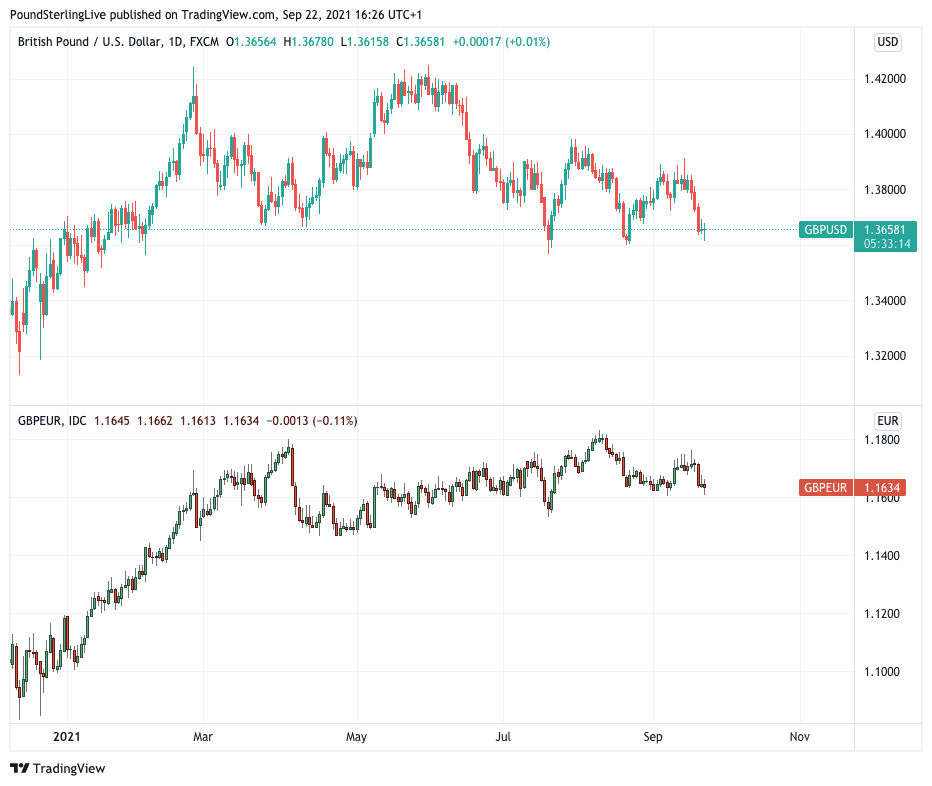

- GBP has fallen steadily this week

- Bank of England policy decision at 12:00 BST

- Comes amidst surging UK gas prices

- Bank might opt to ignore surging inflation

Image © Adobe Stock

- Market rates at publication:

GBP/EUR: 1.1650 | GBP/USD: 1.3647 - Bank transfer rates:

1.1420 | 1.3365 - Specialist transfer rates:

1.1589 | 1.3580 - Get a bank-beating exchange rate quote, here

- Set an exchange rate alert, here

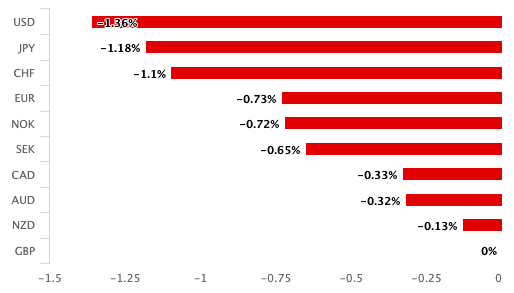

The British Pound is the biggest loser amongst the major currencies of the past week and those hoping for a stronger exchange rate will look to the Bank of England to provide some support.

The steady decline suggests investors have adopted a view the Bank will express concerns over recent economic developments and signal the Bank Rate will stay at 0.10% deep into 2022, disappointing against expectations for an early 2022 rate rise.

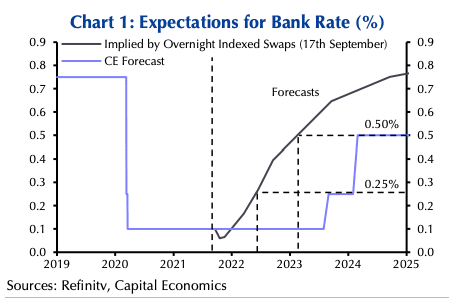

Heading into this week money market pricing suggested investors expected a rise in the Bank Rate from 0.10% to 0.25% in the first quarter of 2022 and to 0.50% at the start of 2023.

How this positioning shifts over coming days in response to the Bank of England's update will likely move the Pound, with any attempts to push back the timing resulting in weakness.

Above: The Pound has fallen against all majors over the course of the past week.

An initial signal of intent lies with how the Bank's Monetary Policy Committee (MPC) votes on 1) immediately ending quantitative easing, and 2) raising interest rates.

There is a chance more than one member votes to end quantitive easing, but given the programme is scheduled to end in December greater market emphasis will fall on the vote to raise rates.

The MPC has been unanimous in voting to keep rates unchanged since lowering them to crisis lows in 2020, therefore any votes to raise rates would be a first clear signal a 'hawkish' shift is underway.

"We expect Michael Saunders, who already at the last meeting voted in favour of reducing the target stock of gilts, to maintain his stance. The rest of the Committee, however, we think is likely to vote for no change against the backdrop of slower activity at the start of Q3," says Anna Titareva, Economist at UBS.

Unanimous votes to keep rates unchanged and a lone dissenter to end quantitative easing early could serve as an initial bearish signal for the Pound.

Image courtesy of Capital Economics.

The Bank's assessment of recent economic developments and the tone they strike will potentially offer currency markets an additional signal that impacts Sterling exchange rates.

"What the market will be watching out for will be any noticeable change in the tone of the MPC that would suggest policy tightening is going to be imminent in the coming months. If that’s the case, we may see a sharp rally in the pound, after the currency spent much of the summer trading in a sideways range," says Fawad Razaqzada, analyst with ThinkMarkets.

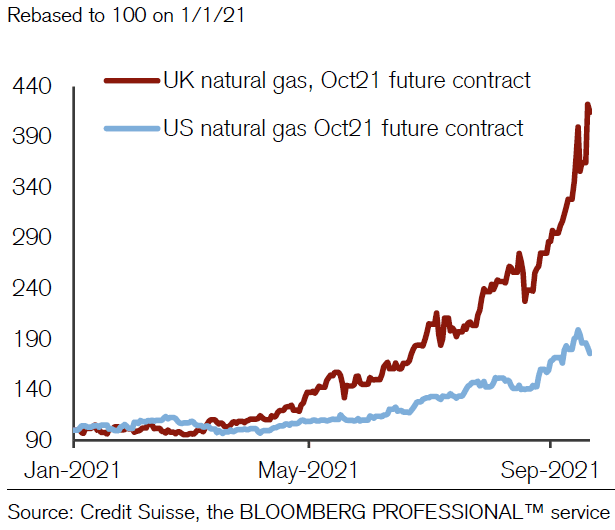

The key risk to any upside narrative for the Pound is that the Bank of England signals caution over a recent hike in UK gas prices, warning further rises in household and business utility tariffs will slow the recovery.

Economists and industry experts are of the view a third consecutive rise in the Ofgem price cap is likely to be announced in February as a result of surging wholesale gas prices.

"Growth has slowed down markedly, with consumption likely to see another drag from the spike in energy tariffs over autumn and next winter. This could leave the Bank's August projections of a closed output gap by year end in serious doubt," says Sanjay Raja, Senior Economist at Deutsche Bank.

Above: "UK natural gas prices have massively outperformed US equivalent in 2021" - Credit Suisse.

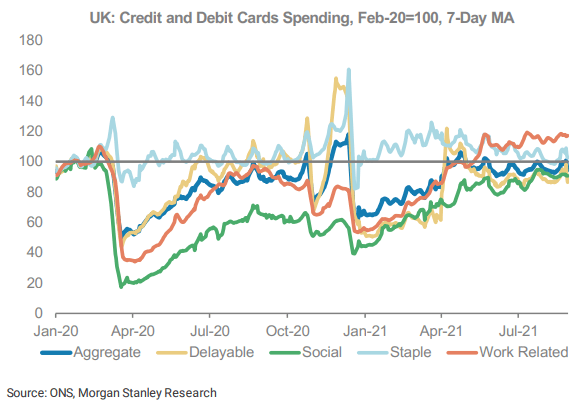

The UK economic rebound slowed during the summer and has generally underwhelmed against economist expectations, even before the latest gas price shock.

"The BoE's projection of 2021 real GDP growth north of 7.0% is looking less realistic based on Q3 data available to-date," says Stephen Gallo, Head of European FX Strategy at BMO Capital Markets.

Economists at HSBC have flagged the run of economic activity disappointments from the UK with HSBC’s economic activity surprise index turning sharply lower lately.

"Growth momentum is not simply faltering, it is slowing more acutely than expected," says Daragh Maher, Head of FX Strategy, US, at HSBC.

Above: UK credit card spending data peaked in early June, image courtesy of Morgan Stanley.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

But a sombre assessment from the Bank of England already appears to be reflected in current Sterling exchange rates:

The Pound-to-Euro exchange rate has fallen from a September 16 high at 1.1763 to 1.1609, the Pound-to-Dollar exchange rate has fallen from a September 14 high at 1.3913 to 1.3616.

The Pound's weakness in advance of the Bank of England event comes amidst benign market positioning opening the door to a 'sell the rumour, buy the fact' market reaction.

"We believe the BoE wants to leave behind the very lowest crisis interest rate and give itself the flexibility to start downsizing its debt portfolio," says a note from Nordic lender and investment bank SEB.

Adopting a 'hawkish' stance on the Pound, SEB anticipate the Bank of England will end its quantitative easing programme "prematurely" in November.

They see a rate rise of 0.15 basis points in May 2022 and another of 0.25 basis points in early 2023 and again in late 2023, bringing the Bank Rate back to its pre-pandemic level of 0.75%.

"As the market in 2021 has been rewarding currencies backed by central banks about to step away from their very loose monetary stimuli, we expect EUR/GBP to resume its trend lower in anticipation of the BOE hikes," says SEB.

Above: The Pound's 2021 rally ended in April.

SEB finds that one reason for a recent rise in the value of the Euro relative to the Pound was a larger increase in Eurozone money market interest rates versus UK rates ahead of September's European Central Bank decision.

But, this "turned out to be a bit of a disappointment for markets after which the EUR/GBP rate spread has resumed a grind lower as well," says SEB.

EUR/GBP is forecast by SEB to end 2021 at 0.84, which gives a GBP/EUR rate of 1.19.

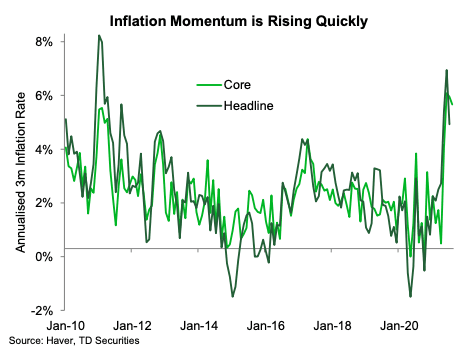

Arguments for the Bank to stick to a timetable that sees the ending of quantitative easing and the commencement of a rate hike cycle in early 2022 lies with the UK's hot inflation levels.

"The overwhelming public narrative on inflation is turning more hawkish, as inflation expectations remain set to move in one direction over the near-term: up," says Sanjay Raja, an economist at Deutsche Bank.

He says navigating the trade-off between slowing growth and surging headline inflation will need careful choreography – "and the Bank of England may be running out of time to clearly set out how it intends to navigate the next few quarters of above 3% y-o-y inflation".

Image courtesy of TD Securities.

Deutsche Bank find that a 20% rise to the Ofgem cap in April - when the cap is due to be reassessed - will add about 60 basis points to headline inflation rates.

Capital Economics are only anticipating a first rate rise in 2023 - which if correct would deliver a significant blow to Sterling bulls - but say the rise in inflation and wholesale gas and electricity prices increases the risk that inflation expectations become unanchored.

Inflation 'unanchoring' would occur if inflation expectations were raised: in short, expectations for higher inflation begets higher inflation as business and consumer's shift behaviour.

"Even so, a rate rise anytime soon would probably prove counterproductive," says Ruth Gregory, Senior UK Economist at Capital Economics.

They say that raising interest rates would weaken demand and jeopardise the recovery and deepen longer-term economic scarring effects.

"We expect a moderately 'hawkish' statement and account of the September MPC meeting on Thursday — but only in a general sense, and not a significantly more 'hawkish' outcome than at the time of the August MPR," says BMO Capital's Gallo.

BMO Capital anticipate see a very low chance of the MPC ditching its description of above-target inflation as 'transient' or 'transitory'; terms used to signal that inflation will come down again and hence why interest rates don't need to be hiked.

The Bank will look to avoid any major communication shifts in their Thursday update and any changes in tone are not expected by BMO Capital to shock foreign exchange and interest rate markets.

Gallo notes that the market is broadly positioned for EUR/GBP downside and has already absorbed expectations for higher interest rates in 2022.

"As such, we think the risk of a 'hawkish shock' for investors from the BoE this week is low," says Gallo.