- GBP/EUR falls below 1.17

- GBP/USD tests mid-July lows

- Global investor sentiment in the driving seat

- Investors fret over Fed stimulus withdrawal

- Asia's Delta wave another concern

- Market rates at publication: GBP/EUR: 1.1660 | GBP/USD: 1.3626

- Bank transfer rates: 1.1434 | 1.3344

- Specialist transfer rates: 1.1578 | 1.3530

- Get a bank-beating exchange rate quote, here

- Set an exchange rate alert, here

The British Pound will remain under pressure against the Euro and Dollar but advance against the Australian and New Zealand Dollars should this week's selloff on global equity markets extend into the final days of August.

The Pound was this week sold against the Euro, Dollar, Franc and Yen amidst a broad decline in investor sentiment that is linked to fears of a global growth slowdown owing to the spread of the Delta variant and expectations the Federal Reserve is preparing to withdraw stimulus.

But, the Pound was bought at the expense of major pro-cyclical currencies, particularly those with a strong exposure to Asia such as the Australian and New Zealand Dollars.

The foreign exchange market is therefore in the grip of a binary positive/negative investor sentiment play, which has meaningful implications for the near-term outlook of the British Pound.

Regular readers of this site will be aware that while the Bank of England and domestic economic developments are largely supportive of Sterling, trade in the UK currency is also underwritten by global investor sentiment.

"In a risk-off world, AUD, CAD, NZD are all weaker and AUD is the most vulnerable of the three. EUR is likely to outperform GBP, SEK, NOK and other risk-sensitive currencies in its time zone," says Kit Juckes, head of FX research at Société Générale.

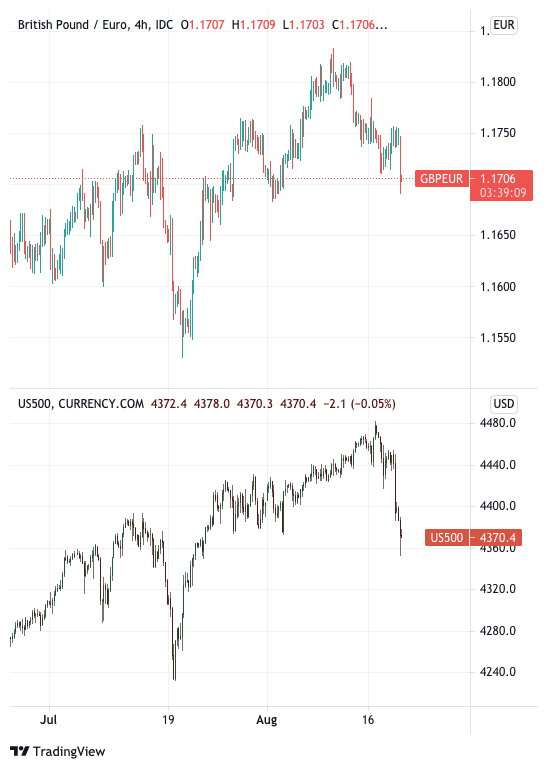

The above chart shows the U.S. S&P 500 index, considered the leading indication of universal investor sentiment; it also shows the Pound-to-Euro exchange rate (GBP/EUR). As can be seen, over recent months there has been a strong positive correlation between the two.

The declines in the S&P 500 of the past week have therefore been consistent with lower valuations in GBP/EUR and looking ahead a further extension lower, or a recovery, will depend on how investors are feeling.

But what is bothering markets, and crucially, can it last?

We can find two dynamics of concern regularly cited by the analyst community: 1) a looming withdrawal of cheap liquidity from the U.S. Federal Reserve, and 2) the spread of the Delta variant in Asia, particularly China.

"A sense of nervousness has returned to haunt financial markets. Investors are increasingly slashing their exposure to riskier assets amid concerns that the Delta outbreak will kneecap global growth, at a time when central banks are trying to take their foot off the accelerator," says Marios Hadjikyriacos, Senior Investment Analyst at XM.com.

The Euro has benefited from the increased nervousness amongst investors given that over the course of the past ten years or so it has increasingly benefitted when stock markets are selling off.

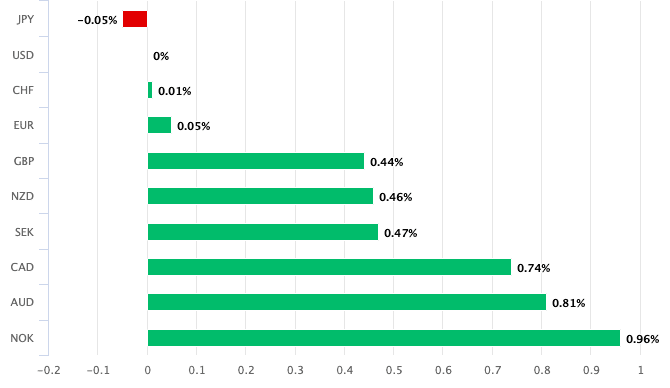

Above: The USD has outperformed all but the JPY, with smaller gains coming against other safe havens such as CHF and EUR.

The low interest rate environment in the Eurozone, courtesy of the European Central Bank's ultra 'easy' monetary policy, looks to be responsible: billions of cheap euros are borrowed to fund a cornucopia of investments by international institutional investors, individuals and corporations.

When those investments are sold they are repatriated into euros, creating a demand on the currency, establishing an impression that it is now a 'safe haven' asset during times of market stress.

"The EUR has traditionally been seen as a pro-cyclical currency, but these longer-term underlying shifts may suggest the EUR is starting to change its spots and may be in the process of moving from cyclical to risk off," says Paul Mackel, Head of FX Research at HSBC.

For a detailed account of how HSBC see the Euro "changing its spots" please see our coverage of this research here.

The Dollar is meanwhile the main currency beneficiary of the current market environment, testament to the expectation of diminishing support from the Federal Reserve over coming months.

The Fed is tipped to announce a 'taper' (reduction to its quantitative easing programme) at some point between next week's Jackson Hole Symposium and September, a move seen as the necessary first step towards an interest rate hike.

This rate hike could occur at some point between late-2022 and early-2023 according to money market pricing.

The entire dynamic has pushed up the yield on U.S. government bonds, which in turns attracts inflows of international funds, bidding the Dollar higher.

The Pound-to-Dollar exchange rate has fallen back to 1.3665, levels last seen on July 21.

The markets have known for some time now that the Fed will be ending its crisis-era support for the economy, but this message was unequivocally reinforced by the release of the minutes of the Fed's august meeting on August 18.

The release of these minutes comes alongside expectations for slowing global economic growth as China, other Asian economies and Pacific economies suffer headwinds owing to rising Covid cases.

The combination of the two is more relevant to investors than either in isolation, it appears.

"Markets are conditioned to be running on central bank support. Markets have become addicted to the sheer volume of money that has been available and this is clearly going to be a drawn-out process to reduce the liquidity it has become so accustomed to," says Hinesh Patel, portfolio manager at Quilter Investors.

"The Fed’s positioning may just be the straw that broke the market’s back given the fears around China’s growth potential, the persistence of the Delta variant and the possibility of global growth peaking," he adds.

The crucial question for those watching stock markets, commodities and the British Pound is whether the current bout of investor nerves represents a turn in a multi-month bull trend, or whether it is yet another patch of doubt that is inevitably bought into.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

The withdrawal of cheap funding from the Fed is still potentially some years away, with markets still more or less anticipating a first rate rise in 2023.

And the support offered by the European Central Bank and other major central banks is unlikely to disappear overnight either.

Fawad Razaqzada, Market Analyst at ThinkMarkets.com says the market's fears concerning the withdrawal of current generous support levels at the Fed is therefore unlikely to prove a game-changer for markets.

"Even if the Fed tapers bond purchases, it will still have a very loose policy compared to pre-Covid... the Fed has already prepared the market for tapering and so the FOMC’s meeting minutes revealed nothing we didn’t know already," says Razaqzada.

The experience of the past year has been that any weakness in stock markets is seen as an opportunities by investors to buy discounted assets.

Of course, history might not repeat but the fundamentals behind market dynamics remains constant: central banks are offering easy money and vaccines continue to blunt Covid's threat.

As such, the latest bout of sentiment-induced weakness in the Pound might prove temporary as has been the case through 2021.