- GBP forming base against EUR

- Too soon to say GBP/USD selloff over

- BoE cuts rates, expands quantitative easing

- Removes a negative dynamic for GBP

Image © Adobe Images

![]() - Spot GBP/EUR rate at time of writing: 1.0900

- Spot GBP/EUR rate at time of writing: 1.0900

- Bank transfer rates (indicative): 1.0620-1.0700

- FX specialist rates (indicative): 1.0750-1.0800 >> More information![]() - Spot GBP/USD rate at time of writing: 1.1739

- Spot GBP/USD rate at time of writing: 1.1739

- Bank transfer rates (indicative): 1.1430-1.1510

- FX specialist rates (indicative): 1.1600-1.1640 >> More information

The British Pound has recovered some ground against the Euro, Dollar and other 'safe haven' currencies over the course of the past 24 hours, thanks to stabilisation in global markets and a decision to slash interest rates and boost quantitative easing at the Bank of England.

Global stock markets remain a key factor in the Pound's performance as the currency tends to fall when markets are tanking, and recover when markets are bouncing.

Currently we are seeing some improvement in global stock market sentiment thanks to the significant measures aimed at minimising the negative economic impact of the coronavirus announced by both central banks and governments. The improvement in sentiment was highlighed by the positive close in the U.S. overnight and the positive day in Asia. Futures markets suggest European markets will open their final trading day of the week in positive territory.

As expected of such a backdrop, the Pound is looking better bid alongside some of the other 'risk on' currencies such as the Australian Dollar.

In the current febrile atmosphere of market instability we would however remain wary of a further deterioration in sentiment related to the coronavirus pandemic, which would put stock markets and Sterling at risk of further declines. Until we see a clear flattening in the number of cases in developed economies we remain open to negative surprises.

For now however it appears that the relentless February-March sell-off that afflicated the Pound has reached a pause with the Pound-to-Dollar exchange rate recovering 1.60% on Friday to reach 1.1648. GBP/USD is down 9.0% in March alone and there is a substantial way to go before we can say the bottom in the exchange rate is in.

"While the pace of decline appears to be slowing, there is still no sign that the recent weakness in GBP is about to stabilize. From here, GPB could drop below 1.1400 and weaken to 1.1330," says Quek Ser Leang, a market analyst with UOB.

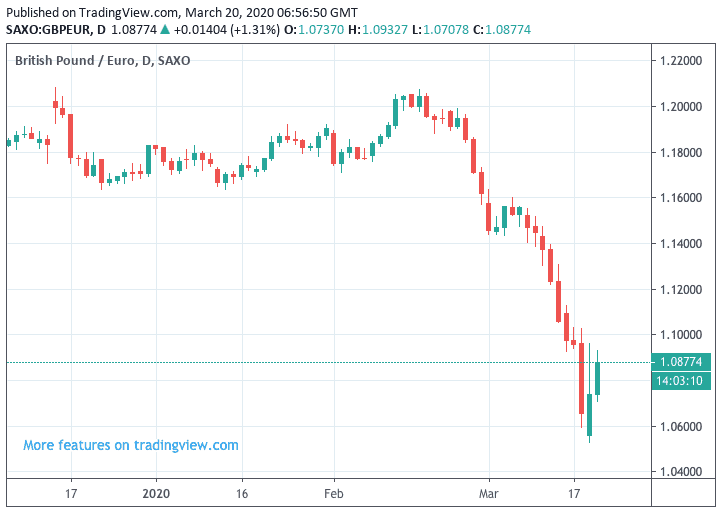

The Pound-to-Euro exchange rate does look to be a little more convincing however, the pair recovered 0.78% on Thursday and has added another 0.50% on Friday to reach 1.0838. At one point yesterday the bounce was as high as 3.0%, but the gains were ultimately pared back.

The Pound was fast heading towards parity against the Euro, but what was crucial for such a target to be realised was that the headline EUR/USD exchange rate kept appreciating. We have however witnessed a notable capitulation in EUR/USD - it suffered its largest one-day drop since June 2016 - and is now back below 1.08, a decline that leads us to expect that the Euro's tank has hit empty.

"Obviously, downward momentum is strong and this coupled with lack of support levels of note could lead to further sharp and rapid decline in EUR," says Leang. Such an outcome could ultimately lend further support to GBP/EUR.

Part of the Euro's recent impetus had been from the market repositioning its stance against the single currency: in February there were substantial 'short' positions on the Euro on global markets, the capitulation of these bets against the Euro has created significant demand.

However, when this technical phenomenon finally comes to an end the Euro might find itself lacking support. We wonder if these shorts have now been flushed from the system.

What has certainly been flushed from the system are expectations for further easing measures to come from the Bank of England. Over recent weeks a build up in expectations for an interest rate cut and the introduction of quantitative easing at Threadneedle Street has exerted significant downside pressure on Sterling.

Currencies tend to depreciate in expectation of interest rate cuts and quantitative easing measures and with markets building up expectations for such actions at the Bank of England over recent weeks the Pound has found itself under pressure.

These measures were finally delivered in an unscheduled announcement on March 19, and with it being unlikely that further cuts and quantitative easing measures are imminent we believe a negative dynamic working against Sterling has been removed.

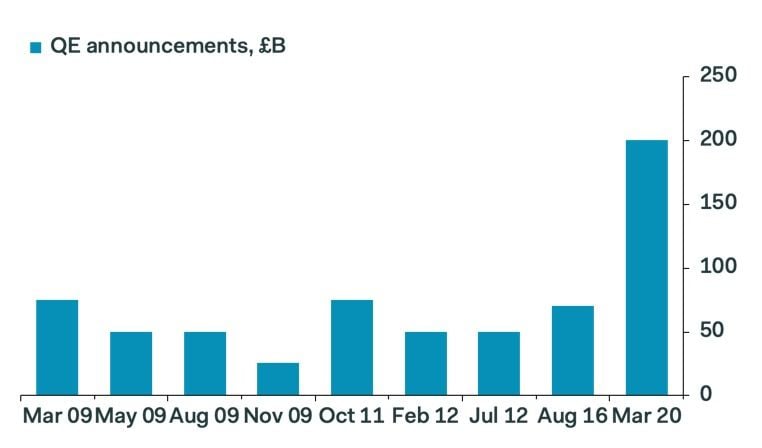

In an unscheduled policy announcement on Thursday, the Bank of England cut its Bank Rate by 15 basis points to 0.10% and increased holdings of government bonds and corporate bonds by £200BN to £645BN.

This is a significant intervention by the Bank as the largest package of support announced previous to this was at £75BN.

The BoE also announced it was increasing the size of its Term Funding Scheme, which aims to increase funding for smaller businesses.

The BoE said in a statement "the spread of COVID-19 and the measures being taken to contain the virus will result in an economic shock that could be sharp and large, but should be temporary".

"In light of actions to tackle the spread of the virus, and evidence relating to the global and domestic economy and financial markets, the Monetary Policy Committee (MPC) held an additional special meeting on 19 March. Over recent days, and in common with a number of other advanced economy bond markets, conditions in the UK gilt market have deteriorated as investors have sought shorter-dated instruments that are closer substitutes for highly liquid central bank reserves. As a consequence, UK and global financial conditions have tightened," added the Statement.

We have noted four potential reasons for the current short-term stability in Sterling:

1) The market has been expecting this move from the Bank of England. Often when an event is so well signposted the market's reaction is to 'sell the rumour, buy the fact'. Indeed, we wrote on Tuesday that it was rising expectations for Bank action that was contributing to Sterling's deep sell-off

2) The market judges the Bank's actions to have been credible. If the Bank and Treasury's combined efforts to dampen the downside effect of the coronavirus outbreak ultimately proves to be effective, then the UK economy could outperform its rivals going forward. Relative economic outperformance tends to underpin a currency.

Of course we need to keep an eye on the coronavirus curve in the UK as a surge in new cases could fast make the actions of the Bank of England and Treasury look inadequate.

3) The Bank has run out of ammunition. Because interest rates are at 0.1% further cuts are now highly unlikely simply because they will achieve very little. The same could be said for further quantitative easing measures. Therefore, it could be reckoned that the Bank has spent its ammunition, thereby denying a driver of further GBP downside.

"Go big or go home from Bank of England. 15bps cut & £200bn QE (mainly govt bonds). Big purchases. BoE previously saw QE as a credit-easing measure too at times of market stress. So makes sense. BoE have now laid their cards on the table. Not a lot left in the monetary tank," says Viraj Patel, FX and Macro Strategist at Arkera.

4) The market's response to the coronavirus episode is shifting. If we look at the markets we can see the AUD and NZD are bouncing, these two currencies have lost significant ground since the coronavirus outbreak and it appears that the deluge of money offered by global central banks could now be providing a backstop to 'risk on' currencies. Crucially the Pound fits this bracket, therefore it could be that the broader market place is moving in Sterling's favour.

David Bloom, Head of Global FX Strategy at HSBC says we are currently in a binary 'Risk on Risk Off' market and a currency's position in that spectrum determines its performance.

"So the most Risk On currencies are currently NOK, AUD, GBP and NZD in that order," says Bloom.

That all these currencies are moving higher confirms markets are turning more 'risk on', indeed a look at the major indices at the time of writing shows a rebound in global stock markets is underway.