Analysts at Deutsche Bank have conceded they might have previously been a little to negative on the Euro’s prospects against the US Dollar.

Writing to clients on Wednesday, March 15, strategist George Saravelos says his team are turning tactically neutral on the pair and see risks of a squeeze to 1.10 over the next couple of months.

Deutsche Bank had previously been of the opinion that the EUR/USD would suffer further notable falls following Donald Trump’s victory which heralded a future of increased Government spending and tax cuts.

The Euro to Dollar exchange rate has however since shown a resilience that has ensured the pair has failed to go below 1.05 in 2017.

At the time of writing the exchange rate is quoted at 1.0732.

Why Deutsche Bank are More Positive on the Euro

“On the US side, it is hard to price much more Fed tightening in the near-term,” says Saravelos.

The call comes on the day the US Federal Reserve opts to raise interest rates but shows little appetite for enacting three further rate rises in 2017.

The market is already expecting five hikes over the next two years and the terminal Fed funds rate is approaching 2.5%.

Both measures are a little below the peaks reached in 2014.

“While they remain low on the Fed’s medium-term forecasts, further repricing will require greater evidence of an improvement in US trend productivity growth or material acceleration in inflation pressure,” says Saravelos.

On the Trump front, Deutsche Bank are disappointed that more aggressive measures on taxation and spending have not been delivered.

“There is sufficient evidence on post-election US politics to conclude that meaningful progress on dollar-positive tax reform will be unlikely in Q2,” says Saravelos.

On the European side of the equation, Deutsche Bank observe the French polling numbers have been remarkably stable.

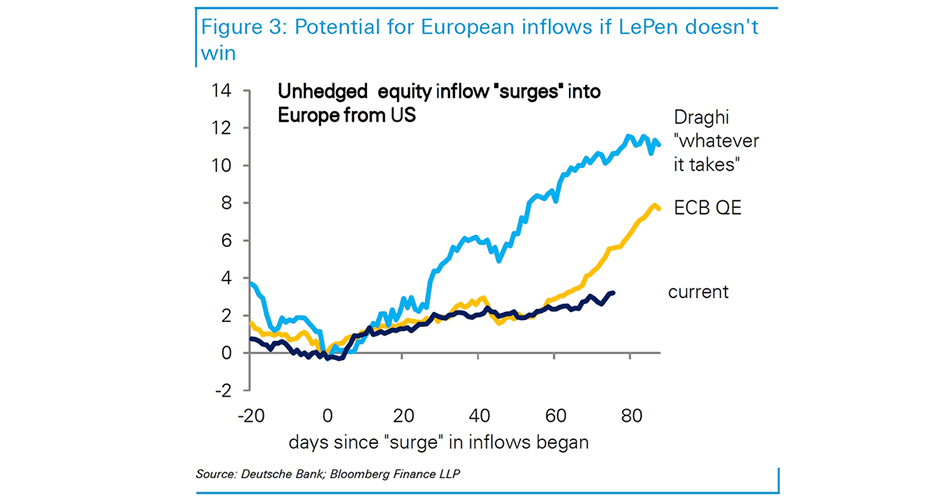

While the market is already pricing a very low probability of a LePen win, there is likely pent-up demand for European growth sensitive assets after the election.

“Unhedged European equity inflows from the US are running well below previous

cycles suggesting the flow picture may improve after the French election,” says Sarvelos.

Focus on the German election could help attract further inflows after.

“The possibility of a Schulz win would be perceived as lowering re-denomination risk as well as increasing the prospects of easier fiscal policy,” says Saravelos.

And then there is the European Central Bank.

Mario Draghi, in the March policy meeting, signalled a willingness to incrementally turn more hawkish.

"We have long argued an ECB taper is not particularly bullish for the Euro - the Dollar weakened around the Fed taper tantrum experience because FX is not driven by long-end yields. But an ECB willingness to potentially discuss a one-off hike in the depo rate combined with upside risks to Eurozone core inflation in coming months makes the near-term case for ignoring ECB exit weaker," says Saravelos.

Forecast Changes

Deutsche Bank tell clients they are tactically turning neutral on EURUSD and revising their Q2 and Q3 forecasts up to 1.08 and 1.03 respectively.

They are not however changing our year-end bearish forecast of 0.95 cents. The