The Euro to Dollar exchange rate (EUR/USD) should be supported above parity in 2017 say Bank of America Merrill Lynch Global Research.

The call comes amidst heightened expectation in the institutional analyst community for a 1:1 exchange rate to be attained in 2017, largely owing to the apparently unstoppable advance of the Dollar.

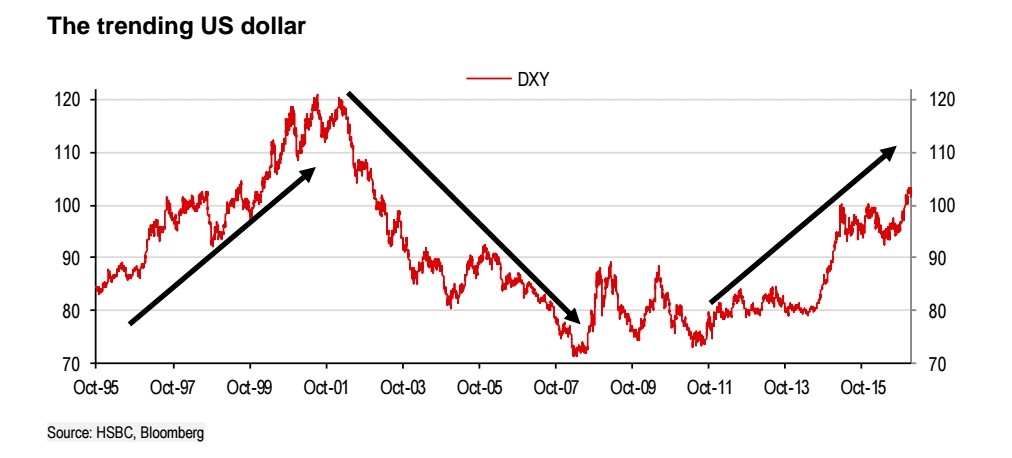

Indeed, the foreign exchange theme of 2017 that most institutional analysts are in agreement with is that the US Dollar is likely to strengthen further.

In real effective terms, the USD is about 8% above its 20-year average, but still 8% below its high of 2002.

The current cycle of appreciation is therefore possibly only 50% done if we are to look at past action as a guide.

Athanasios Vamvakidis at Bank of America Merrill Lynch Global Research in London has meanwhile told clients he too believes the Dollar will continue to strengthen in 2017.

However, Dollar strength may have to come from other sources as the EUR/USD is not a slam-dunk bet for parity.

Although hedge funds are long the USD, Bank of America notes real money remains short, relatively to positioning in the last 12 months which tells.

In short, there are other currencies that will have to absorb the bulk of the Dollar's advance.

Always be Wary of the Surprise

Looking at the evidence on recent thematic calls made by Bank of America, we note they have done well over the course of the past 12 months.

A year ago investors were in panic about deflation.

Back then, BofA took a contrarian view and argued that inflation was what could really surprise markets.

Indeed, as the year progressed, a good case inflation scenario unfolded.

Before the US elections, we argued that the good reflation scenario would continue, despite substantial risks (The rest of the year ahead and a preview of the year to follow). The market reaction following the US elections was even faster than we had expected.

“Having been right too early, we are now wondering what could surprise markets this year,” cautions Vamvakidis.

2017's Risks to Consensus

Vamvakidis warns that he does see substantial uncertainties this year.

In particular, the analyst is cautious of entering a headlong chase of a higher USD, particularly towards the start of the year.

A number of reasons to be cautious on the ability of the US Dollar to trend higher are:

- “In the short term, we are concerned about US data in Q1, given negative seasonality in recent years.

- “Negotiations for the US fiscal stimulus could be long and more difficult than markets currently expect.

- “Trade protection remains a concern.

- "Later in the year, Yellen's replacement will become a key market theme.

- “Beyond the US, Europe is facing political tail risks, with elections in France, the Netherlands, Germany and possibly Italy.

- “We have also argued that markets are not fully appreciating the ECB constraints and the challenges ahead (The end of the Draghi cycle).

- “Geopolitical risks depending on the policies of the new US administration could be another blind spot, with hard to predict market implications. Historically high equity prices and still low volatility suggest market complacency.

Bullish USD Long-Term, Wary Near Term

Put together, Bank of America argue for a stronger Dollar in 2017 but there are near-term trials.

“We remain bullish on the USD for the year, but see short-term risks. Following the strong USD rally, we closed our short EURUSD trade with a profit and remain long USD against JPY, AUD and NZD,” says Vamvakidis.

As such Bank of America forecast USD/JPY at 120 and EUR/USD at 1.02 in 2017, but the risks are for an even higher USD in a positive scenario.