The Euro is already undervalued against the US Dollar - this is just one reason why the EUR/USD exchange rate won't fall to 1.0.

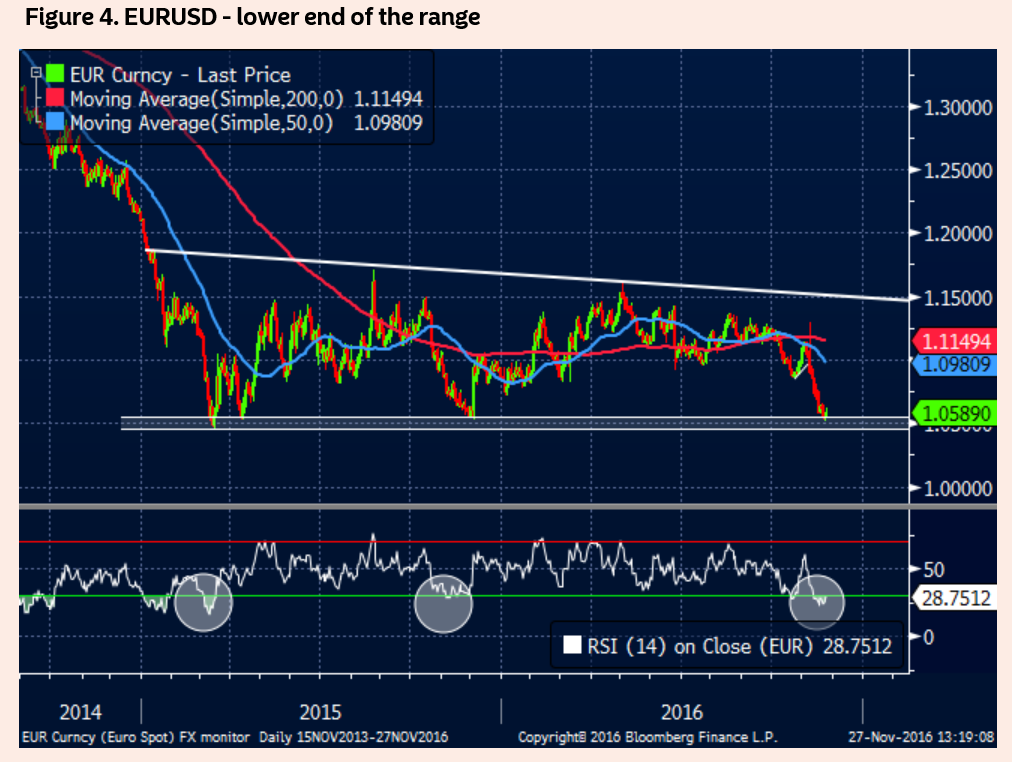

The Euro remains near multi-year lows in the vicinity of $1.05 having slid from a high near $1.11 at the start of November.

The velocity of November's decline has inevitably raised questions over whether the exchange rate will now sink to 1:1.

Such a move is likely argue analysts at Deutsche Bank who have been long-time bears on the EUR/USD.

They are joined by other big names including Barclays, Societe Generale and Bank of Tokyo, to name but a few.

Yet, the majority of analysts continue to argue against such weakness.

“'The EURUSD to parity' is a popular call again," notes Nordea Markets' Aurelija Augulyte. “But if we haven’t seen the EUR collapse on multiple downgrades, bailouts, Greek default, Cyprus bail-in, amidst rising unemployment across the Euro area it is really hard to see something like a well-known-in-advance Italian constitutional referendum, where most expect a 'No' vote anyway, becoming THE reason to sell the EUR”.

Technically EUR/USD should hold at the lower boundary of a long-term range it is currently revisiting if previous cycle lows are anything to go by.

The RSI indicator (circled in chart below) is also indicating the pair is heavily oversold at its current level and thereby at risk of a recovery – particularly if we go by previous oversold lows.

Augulyte also highlights a subtle difference between US and Eurozone yields.

International capital chases higher yields increasing the value of denominated currency so they are a major factor in a currency analysis.

Yes, whilst yields in the US are rising strongly, so are inflation expectations, thus the ‘real’ yield outlook, which is the difference in what an investor gets in return after taking away inflation erosion is actually pretty poor.

In the Eurozone, however, where yields have remained low, missing out on the Trump reflationary after-party, inflation expectations are also low, thus from a real yield perspective the two are not so different.

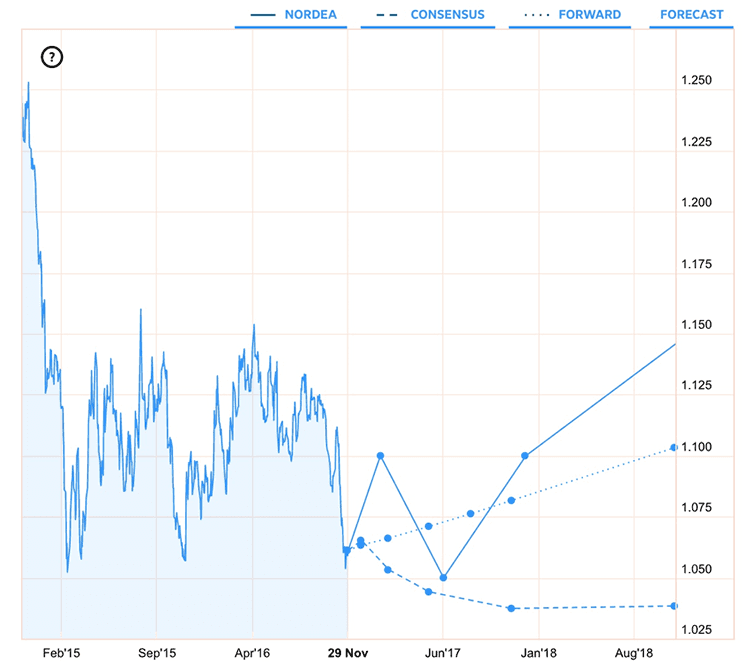

“While the nominal rate spread has pushed the EUR/USD down after the US election, it is still the real rates that guide the currencies over time. With the US inflation and inflation expectations higher than in the Eurozone, the long term 'fair value' of the EUR/USD is also trending higher, north of 1.20,” said the Nordea analyst.

Consensus forecasts for the EUR/USD see the EUR/USD bottoming towards 1.03 in November 2017 ahead of a shallow recovery.

Image courtesy of Nordea Markets

Dollar Strength to Fade say Rabobank

Also arguing against the EUR/USD @ parity camp are Rabobank who envisage an uninspiring recovery in the exchange rate going forward.

The reflationary theme which helped stimulate the rise in US bond yields and therefore the Dollar which is currently extremely closely correlated to yields may be reaching an end argue analysts at the Dutch-based bank.

“It may not be clear for some months whether the market has correctly anticipated a sea-change in the inflationary prospects of the US economy, or whether this month’s move has been overdone," says foreign exchange analyst Jane Foley in a note to clients. “While it is reasonable to expect a loosening in fiscal policy in the US, there are downside risks to inflation potentially from the same set of factors that have been pressuring inflation in recent years,” argues Foley.

These downside risks can be summarised as a lack of ‘pass-through’ of relaxed conditions to increased consumer demand and the real economy.

“Income inequality, low productivity and wage growth may continue to limit the pass through of expansionary policies to demand and inflation,” says Foley.

A downwards revision in the inflation outlook will weigh on US yields and therefore the Dollar.

This forms the basis of Rabobank’s forecast for a rebound in EUR/USD.

“While we are continuing to expect a recovery to EUR/USD 1.08 on a 3 mth view, we are now forecasting only a moderate recovery to 1.10 on a 12 mth view based on our expectations that US yields will soften in that time-frame,” says the Rabobank strategist.

The rebound is lower than Rabobank previously forecast, however, due to political risk keeping the Euro down.

Foley notes:

“While we expect EUR/USD to trend higher on a 3 to 12 mth view, it is becoming clear that investors are positioning themselves for a bumpy ride in European politics.

"Even if Italian PM Renzi remains in situ after the December 4 referendum, Italy faces elections in 2018 and this could be another conduit for protest votes and anti-EMU sentiment.

“In the spring both the Dutch and French elections could provide grandstands for nationalism.”

Whilst it is not the strategist’s view that these elections will lead to a disintegration of the Euro, Foley expects them to weigh on the currency in 2017 and therefore keep the potential for rebound limited, at best.