Image © Adobe Images

The euro can regain some of its May losses into the month-end period, but the recovery should be shallow.

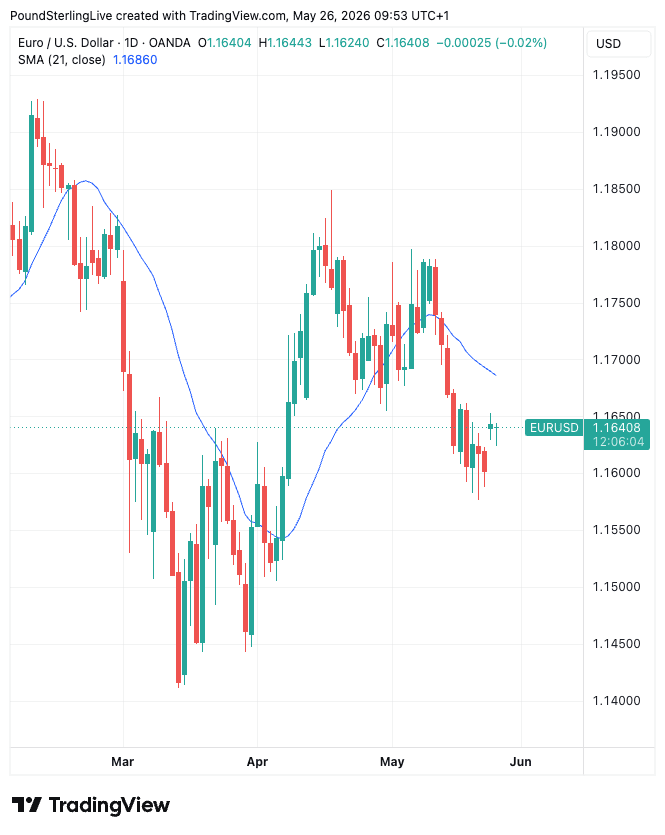

The euro to dollar exchange rate rose as high as 1.1653 on Monday thanks to a 7% fall in crude oil prices, but hasn't carried any of that momentum into Tuesday, easing to 1.1630 at the time of writing.

The charts are telling us that a recent selloff that characterised euro-dollar trade through the middle part of May has ended, and a tactical rebound, helped by potentially supportive month-end flows, is possible.

Month-end signals show money managers are likely to be net USD sellers against EUR this month-end period, owing to relative equity market movements over the course of May.

A big drop of 1.75% through mid-month was quite significant, and the mean-reverting tendencies of this exchange rate mean we could expect a further paring of recent losses.

The euro-dollar can therefore approach its 21-day moving average at 1.1683 this week. However, this Week Ahead Forecast doesn't expect much progress beyond this signal line unless there's a notable and convincing shift against USD.

As mentioned, Monday's move higher in EUR/USD looks linked to a drop in oil prices, while Tuesday's softness is a response to another rise in oil.

So some yo-yoing on geopolitical headlines out of the Middle East can be expected.

The direction of travel nevertheless remains in favour of a breakthrough in peace negotiations that would be typically expected to undermine the USD.

However, the reopening of the Strait of Hormuz won't be simple and could take months to achieve, even in the event of the U.S. and Iran striking a deal.

That should prevent a reversion in oil and gas prices to pre-war lows, which would be expected to add pressure to the Eurozone economy, whereas the U.S. economy would benefit on a terms-of-trade basis as U.S. exports of oil and gas draw in handsome revenues.

Last week's Eurozone PMI data showed the economy came under notable pressure in May as the effects of the war worked through European households and businesses, limiting the ability of the ECB to raise interest rates in the face of rising price pressures.

To be sure, the Eurozone outlook is less constructive than it was at the start of the year when euro-dollar was trending towards 1.20.

Turning to the calendar, we should receive a reminder as to why the dollar has perked up: the U.S. economy is humming along nicely, is relatively insulated to the Iran war while inflation is printing on the wrong side of 3.0%.

The U.S. will release April PCE inflation figures on Thursday, where we should get further evidence of building inflationary pressures.

A core PCE rate of around 3.3% y/y will reinforce the notion that there's limited scope for the U.S. Federal Reserve to lower interest rates this year.

That's important for the dollar which weakened through the first quarter of the year as investors saw the Fed cutting interest rates as the ECB kept rates unchanged.

With Fed rate cuts now out of the picture, the dollar is firmer and euro-dollar 'bulls' can't rely on supportive developments in interest rate policy differentials to drive a rally.

That should ensure that any gains by the euro-dollar witnessed in the near-term should be relatively contained.